- LIVE QUOTES

- LEARN

- HELP

EN

A Look At Ecolab’s Valuation As Earnings Strength And Raised 2026 Guidance Support Investor Confidence

What Ecolab’s latest earnings signal for investors

Ecolab (ECL) moved into focus after its latest earnings report showed 15% adjusted EPS growth in 2025 and 3% organic sales growth in Q4, alongside updated 2026 guidance and a reaffirmed quarterly dividend.

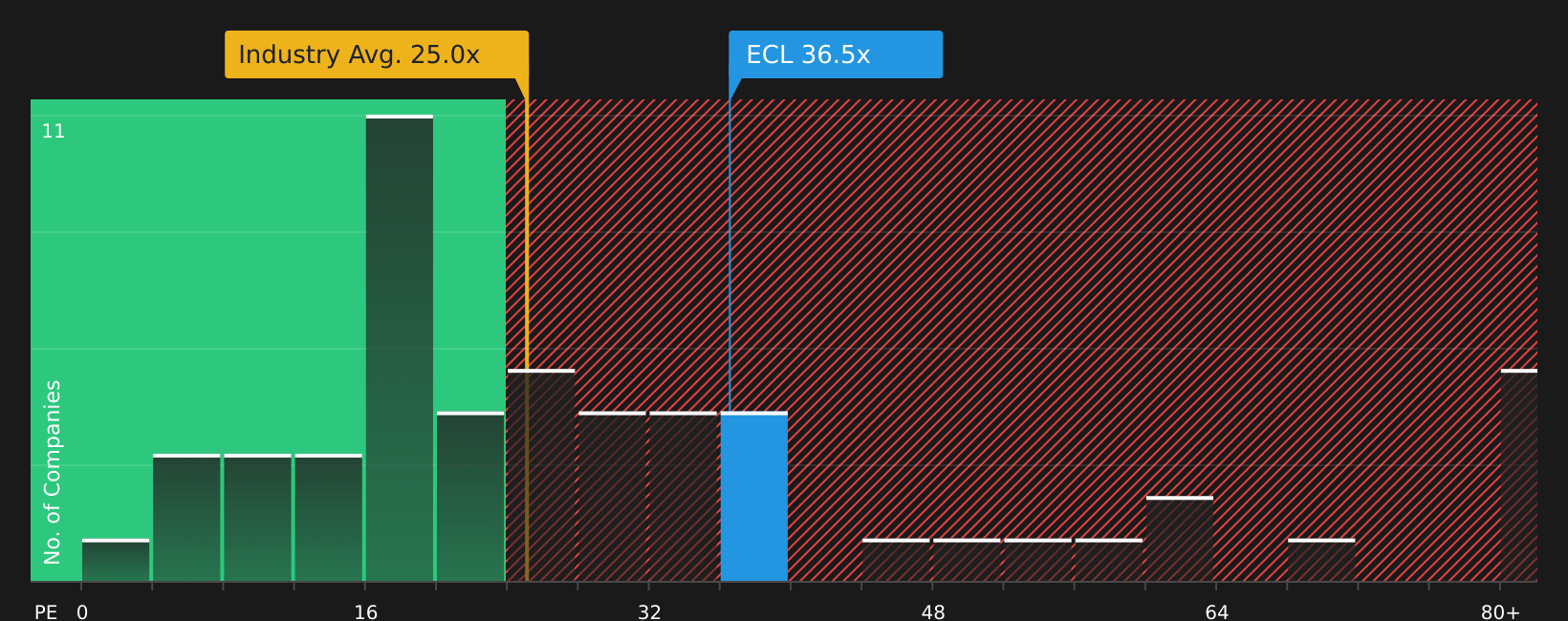

See our latest analysis for Ecolab.

The latest earnings update and raised guidance have come after a mixed share price run, with a 1-day share price return of 1.04% and a 7-day return of 1.73%, against a 30-day share price decline of 5.54%. Even so, long term momentum looks stronger, with a 1-year total shareholder return of 17.14% and a 3-year total shareholder return of 66.04%, indicating that patient holders have seen materially better outcomes than recent monthly moves suggest.

If this kind of earnings driven story has your attention, it can be useful to see which other companies are also gaining interest from capital markets and institutions via our 20 top founder-led companies

With Ecolab shares up 17.14% over 1 year and 66.04% over 3 years, and analysts’ average price target sitting above the recent US$267.03 close, you have to ask: is there still a buying opportunity here, or is future growth already priced in?

Most Popular Narrative: 17% Undervalued

With Ecolab’s fair value in the most followed narrative at $320.43 against a last close of $267.03, the story hinges on pricing power and margin expansion.

Ecolab is focusing on expanding its One Ecolab growth initiative, aiming to capitalize on market share gains and increased value pricing. This initiative is expected to drive revenue growth and improve net margins by delivering exceptional value to customers.

Curious what has to happen for that higher value to make sense? The narrative leans on faster revenue growth, higher margins, and a rich earnings multiple. The exact mix matters.

Result: Fair Value of $320.43 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, softer demand in heavy industrial markets and higher input costs from tariffs and local suppliers could pressure margins and challenge the company’s ability to maintain pricing power.

Find out about the key risks to this Ecolab narrative.

Another View: What Earnings Multiples Are Signalling

The popular narrative leans on a fair value of $320.43, yet Ecolab currently trades on a P/E of 36.3x. That is richer than the US Chemicals industry at 29.2x, the peer average at 29x, and the fair ratio of 25.7x, which points to valuation risk if expectations slip.

For a closer look at what this pricing gap could mean for your own thesis, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment split between upside potential and valuation risk, it makes sense to move fast and review the facts yourself, then weigh the 1 key reward and 1 important warning sign.

Looking for more investment ideas?

If Ecolab has sharpened your focus, do not stop here. Use the screener to quickly surface fresh opportunities that fit the kind of portfolio you want to build.

- Target quality at a discount by scanning 62 high quality undervalued stocks that pair solid fundamentals with attractive pricing.

- Lock in reliable income potential by reviewing 13 dividend fortresses built around higher yielding payers.

- Dial down portfolio stress by checking 68 resilient stocks with low risk scores that score well on resilience and financial strength.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com