- LIVE QUOTES

- LEARN

- HELP

EN

PVH (PVH) Is Up 21.4% After Beating Adjusted EPS And Mapping Tariff Strategy Plans – Has The Bull Case Changed?

- PVH Corp. recently reported its fourth-quarter and full-year 2025 results, with quarterly sales rising to US$2,505.1 million but swinging from net income of US$157.2 million to a net loss of US$158.3 million, while full-year net income fell sharply despite higher annual sales of US$8,950.2 million versus US$8,652.9 million previously.

- Behind the headline loss, PVH delivered adjusted earnings per share well above expectations, driven by Calvin Klein and Tommy Hilfiger, and outlined plans to counter higher tariffs while leaning into cultural partnerships and direct-to-consumer growth to support its PVH+ transformation plan.

- Next, we’ll examine how PVH’s stronger-than-expected adjusted earnings and tariff mitigation plans may influence its broader investment narrative.

AI is about to change healthcare. These 37 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

PVH Investment Narrative Recap

To own PVH, you need to believe the PVH+ plan can turn iconic brands Calvin Klein and Tommy Hilfiger into stronger earnings, even as tariffs and consumer uncertainty weigh on results. The latest quarter shows that while reported earnings were hit by a large one off loss, the core business still produced adjusted EPS ahead of expectations. That supports the near term catalyst around execution on brand momentum, but tariff risk remains the most immediate swing factor for margins.

One of the most relevant developments is PVH’s detailed tariff outlook, including an expected 15% rate on goods entering the US from February 2026 and an estimated significant EBIT hit. Management is already talking about mitigation actions, which ties directly into the catalyst around margin efficiency under PVH+. How effectively those actions offset higher import costs will matter at least as much as the recent earnings beat for the near term story.

Yet despite the upbeat headlines, the tariff overhang is something investors should be aware of, especially if...

Read the full narrative on PVH (it's free!)

PVH's narrative projects $9.4 billion revenue and $707.7 million earnings by 2028. This requires 2.3% yearly revenue growth and about a $239 million earnings increase from $468.5 million today.

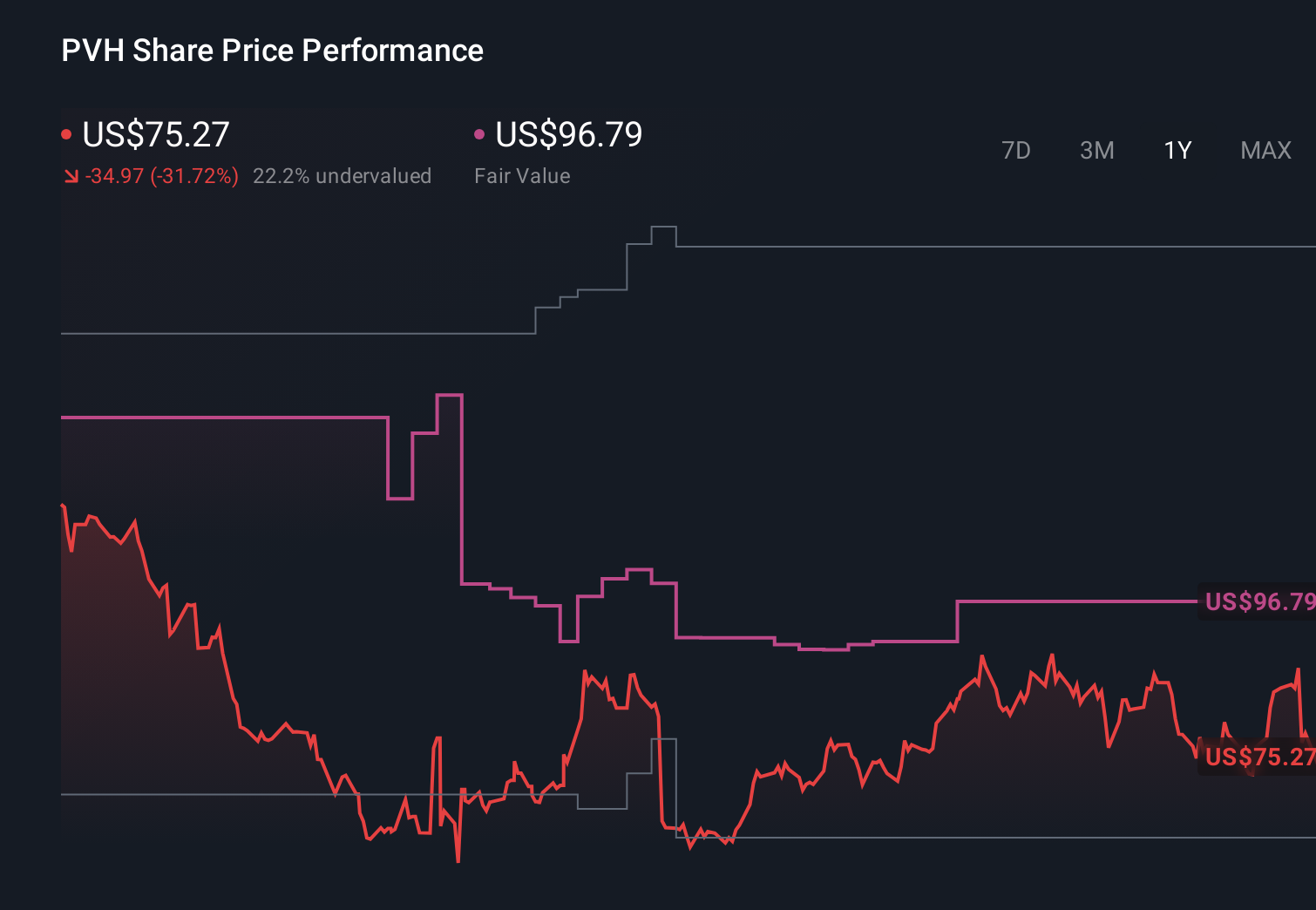

Uncover how PVH's forecasts yield a $96.79 fair value, a 20% upside to its current price.

Exploring Other Perspectives

Some of the most cautious analysts were already assuming only about 3.4% annual revenue growth and US$791.2 million of earnings by 2029, so this latest tariff hit and margin uncertainty could push their more pessimistic view even further, while others may see the Q4 beat as evidence that PVH can out-execute those lower expectations.

Explore 4 other fair value estimates on PVH - why the stock might be worth over 2x more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your PVH research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free PVH research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate PVH's overall financial health at a glance.

Contemplating Other Strategies?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com