- LIVE QUOTES

- LEARN

- HELP

EN

Why lululemon athletica (LULU) Is Up 7.1% After Insider Share Purchase Amid Mixed Outlook

- Recently, lululemon athletica reported fiscal Q4 and full-year results that led to reassessments of its outlook by several Wall Street firms, alongside ongoing discussions around tariffs and North American demand pressures.

- A key development was Interim Co-CEO Andre Maestrini’s purchase of 3,275 company shares, which many investors interpret as a strong signal of internal confidence amid mixed external views.

- We’ll now explore how this insider buying, set against concerns about demand and margins, reshapes lululemon’s existing investment narrative.

Find 62 companies with promising cash flow potential yet trading below their fair value.

lululemon athletica Investment Narrative Recap

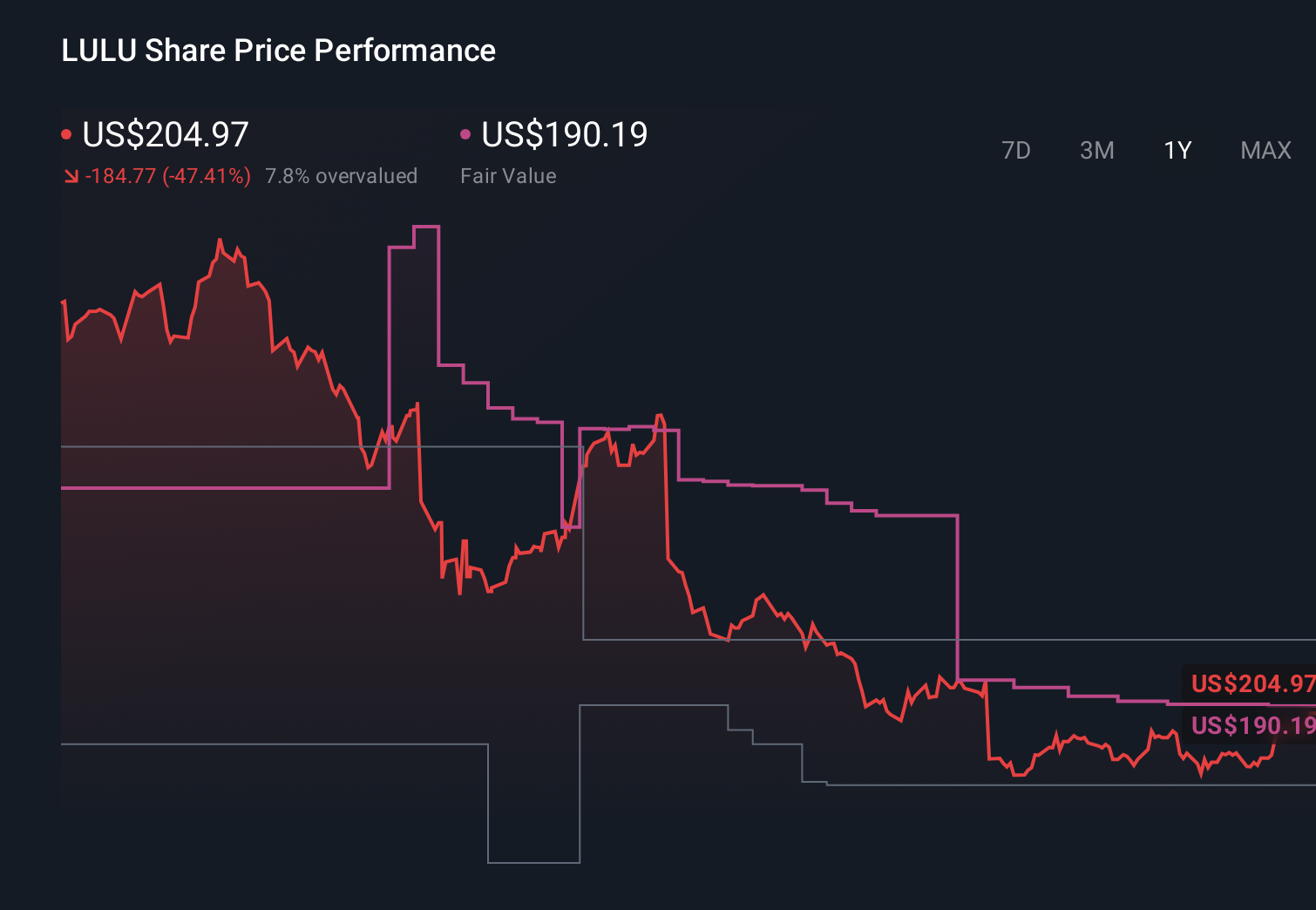

To own lululemon today, you have to believe the brand can reignite demand in North America while protecting margins from higher tariffs and promotional pressure. The latest Q4 and full year results, along with softer Q1 guidance, keep near term demand in focus as the main catalyst, while tariff driven margin compression remains the most pressing risk. Andre Maestrini’s insider share purchase does not materially change those fundamentals, but it does add an interesting datapoint to sentiment.

Against this backdrop, lululemon’s recent guidance for 2026 revenue of US$11.35 billion to US$11.50 billion and EPS of US$12.10 to US$12.30 stands out as the most relevant reference point. It frames how much room the company has to absorb tariff headwinds and a slower U.S. business while it pushes product innovation and international growth as key levers for any future reacceleration.

Yet even with insider buying, investors should be aware of the risk that North American demand softness and tariff costs could...

Read the full narrative on lululemon athletica (it's free!)

lululemon athletica's narrative projects $12.6 billion revenue and $1.6 billion earnings by 2029.

Uncover how lululemon athletica's forecasts yield a $183.80 fair value, a 18% upside to its current price.

Exploring Other Perspectives

Some analysts see much steeper risks than consensus, with bearish forecasts around US$11.8 billion in 2028 revenue and US$1.5 billion in earnings, reminding you that views on lululemon’s recovery and tariff impact can differ widely and may shift again after this latest insider buying and guidance update.

Explore 40 other fair value estimates on lululemon athletica - why the stock might be worth over 2x more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your lululemon athletica research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free lululemon athletica research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate lululemon athletica's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our top stock finds are flying under the radar-for now. Get in early:

- Uncover the next big thing with 32 elite penny stocks that balance risk and reward.

- Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 26 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com