- LIVE QUOTES

- LEARN

- HELP

EN

Why Li Auto (LI) Is Up 5.2% After March Delivery Rebound And New Autonomous Tech Unveiling

- In March 2026, Li Auto Inc. reported deliveries of 41,053 vehicles, lifting its cumulative total to 1.64 million and reflecting a rebound after earlier production bottlenecks, particularly as the Li i6 surpassed 24,000 monthly units.

- At the same time, Li Auto unveiled its MindVLA autonomous driving foundation model at NVIDIA GTC 2026 and prepared to launch a new Li L9 in the second quarter, underscoring a push to pair higher volumes with in-house advanced driving technology.

- We’ll now examine how March’s delivery rebound, led by the Li i6, may influence Li Auto’s pre-existing investment narrative and expectations.

Find 58 companies with promising cash flow potential yet trading below their fair value.

Li Auto Investment Narrative Recap

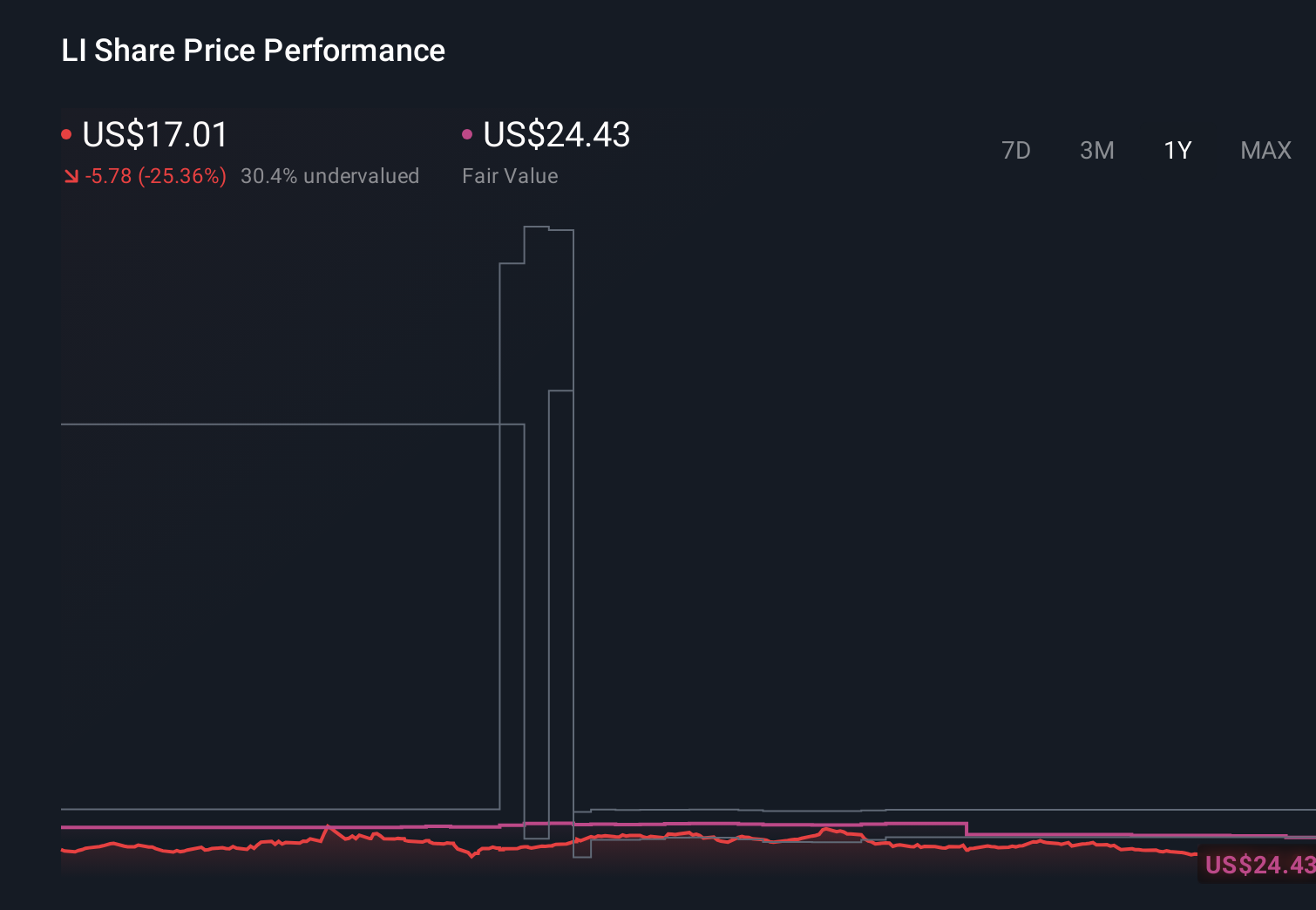

To own Li Auto today, I think you need to believe the company can turn strong BEV launches and software-heavy cars into improving margins, despite rising spending and fierce EV competition in China. March’s 41,053 deliveries, helped by the Li i6 passing 24,000 units, ease near term concerns about execution on its BEV pivot, but they do not remove the key risk around profitability pressure from high AI and capital investment.

Among the recent announcements, the US$1,000,000,000 share repurchase authorization stands out next to March’s rebound. It sits alongside RMB 112,312.51 million in 2025 revenue and modest net income, and may matter for investors weighing liquidity and capital allocation against an expensive valuation, especially with Li Auto’s P E multiple well above both peers and its own estimated fair multiple while it continues to invest heavily in technology and product expansion.

Yet investors should also be aware that intensifying global trade tensions and possible new tariffs on Chinese EV exports could...

Read the full narrative on Li Auto (it's free!)

Li Auto's narrative projects CN¥167.9 billion revenue and CN¥8.1 billion earnings by 2029.

Uncover how Li Auto's forecasts yield a $22.16 fair value, a 20% upside to its current price.

Exploring Other Perspectives

Before this delivery jump, the most bearish analysts were assuming roughly flat revenue at about CN¥139.1 billion by 2028 and still saw earnings rising to CN¥9.3 billion, a far more cautious view than the consensus that could shift again once these stronger March numbers and Li Auto’s tech spending path are fully reflected.

Explore 5 other fair value estimates on Li Auto - why the stock might be worth 20% less than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Li Auto research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

- Our free Li Auto research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Li Auto's overall financial health at a glance.

No Opportunity In Li Auto?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com