- LIVE QUOTES

- LEARN

- HELP

EN

US Market's Hidden Gems: 3 Promising Small Caps

The United States market has experienced a robust performance, rising 3.5% over the last week and climbing 31% over the past year, with earnings projected to grow by 16% annually. In this thriving environment, identifying promising small-cap stocks can be key to unlocking potential opportunities that may not yet be fully recognized by the broader market.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| First Bancorp | 68.18% | 1.28% | -2.88% | ★★★★★★ |

| Cashmere Valley Bank | 31.17% | 5.25% | 1.74% | ★★★★★★ |

| Oakworth Capital | 26.12% | 15.98% | 13.01% | ★★★★★★ |

| ASA Gold and Precious Metals | NA | 12.65% | 41.20% | ★★★★★★ |

| Winchester Bancorp | 121.44% | 49.13% | 3283.33% | ★★★★★★ |

| Union Bankshares | 374.44% | 1.11% | -7.71% | ★★★★★☆ |

| Seneca Foods | 38.64% | 2.39% | -18.65% | ★★★★★☆ |

| NameSilo Technologies | 12.63% | 14.48% | 3.12% | ★★★★★☆ |

| Pure Cycle | 5.42% | 9.36% | -2.03% | ★★★★★☆ |

| Oxford Bank | 12.42% | 14.34% | 4.14% | ★★★★☆☆ |

Let's uncover some gems from our specialized screener.

Anterix (ATEX)

Simply Wall St Value Rating: ★★★★★☆

Overview: Anterix Inc. specializes in commercializing spectrum assets to support utility and critical infrastructure customers with private broadband networks, with a market capitalization of $756.62 million.

Operations: Anterix generates revenue primarily from wireless communications services, amounting to $5.93 million.

Anterix, a notable player in the telecom space, is making waves with its strategic initiatives and financial performance. Recently, it inked a 900 MHz spectrum sale agreement with Texas-New Mexico Power to bolster grid reliability. Despite reporting a net loss of US$6.6 million for Q3 2025, Anterix's nine-month net income was US$72.12 million, showcasing its potential turnaround capabilities. The company has repurchased shares worth US$23.26 million as part of its buyback strategy announced in 2023. With no debt and trading at nearly 75% below estimated fair value, Anterix presents intriguing prospects for investors looking at utility-focused connectivity solutions.

- Dive into the specifics of Anterix here with our thorough health report.

Understand Anterix's track record by examining our Past report.

Willdan Group (WLDN)

Simply Wall St Value Rating: ★★★★★★

Overview: Willdan Group, Inc. offers professional, technical, and consulting services such as engineering, program management, policy advisory, and software and data analytics mainly in the United States with a market cap of approximately $1.19 billion.

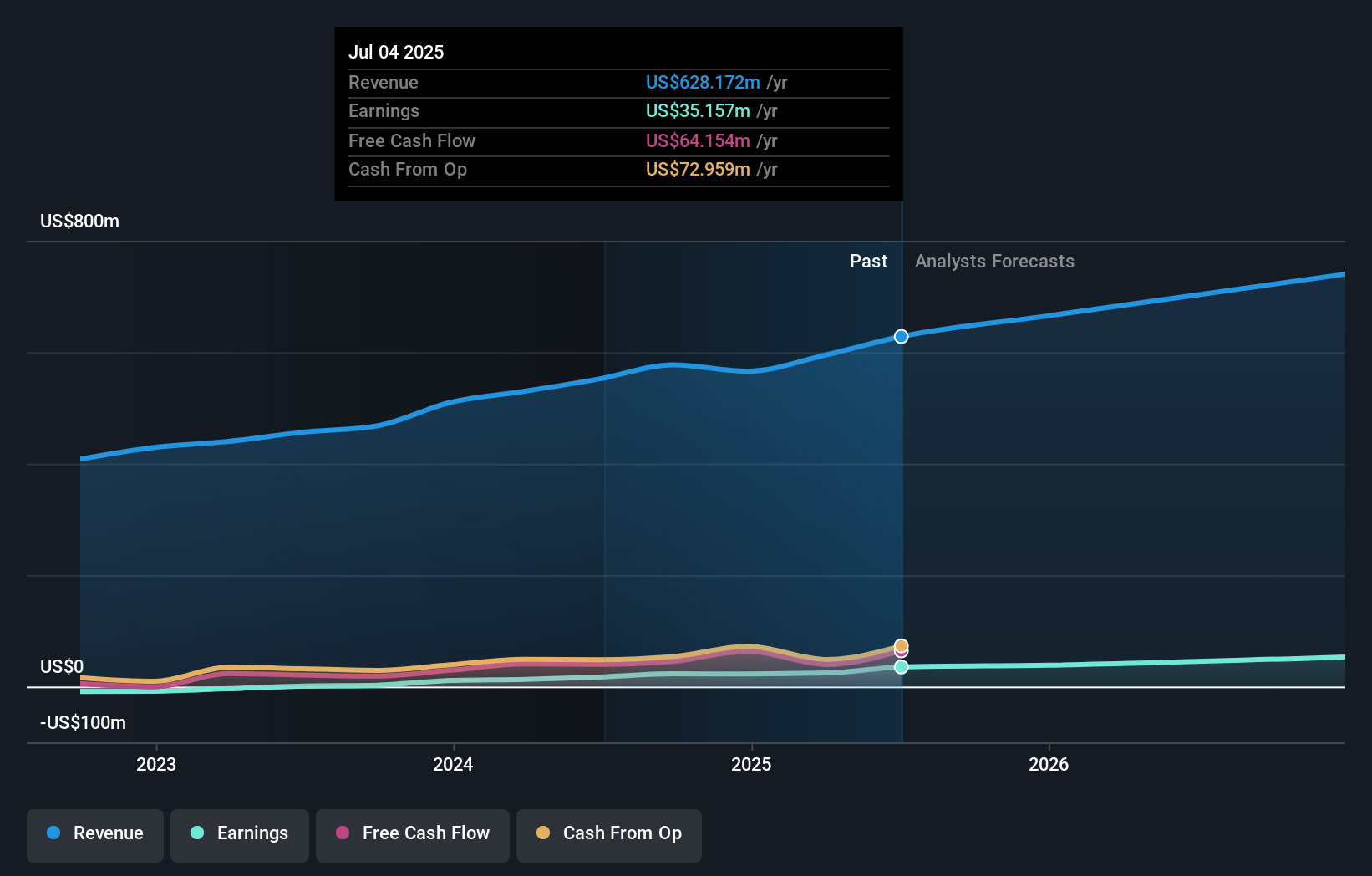

Operations: The company generates revenue primarily from its Energy segment, contributing $576.05 million, and its Engineering & Consulting segment, which adds $105.50 million.

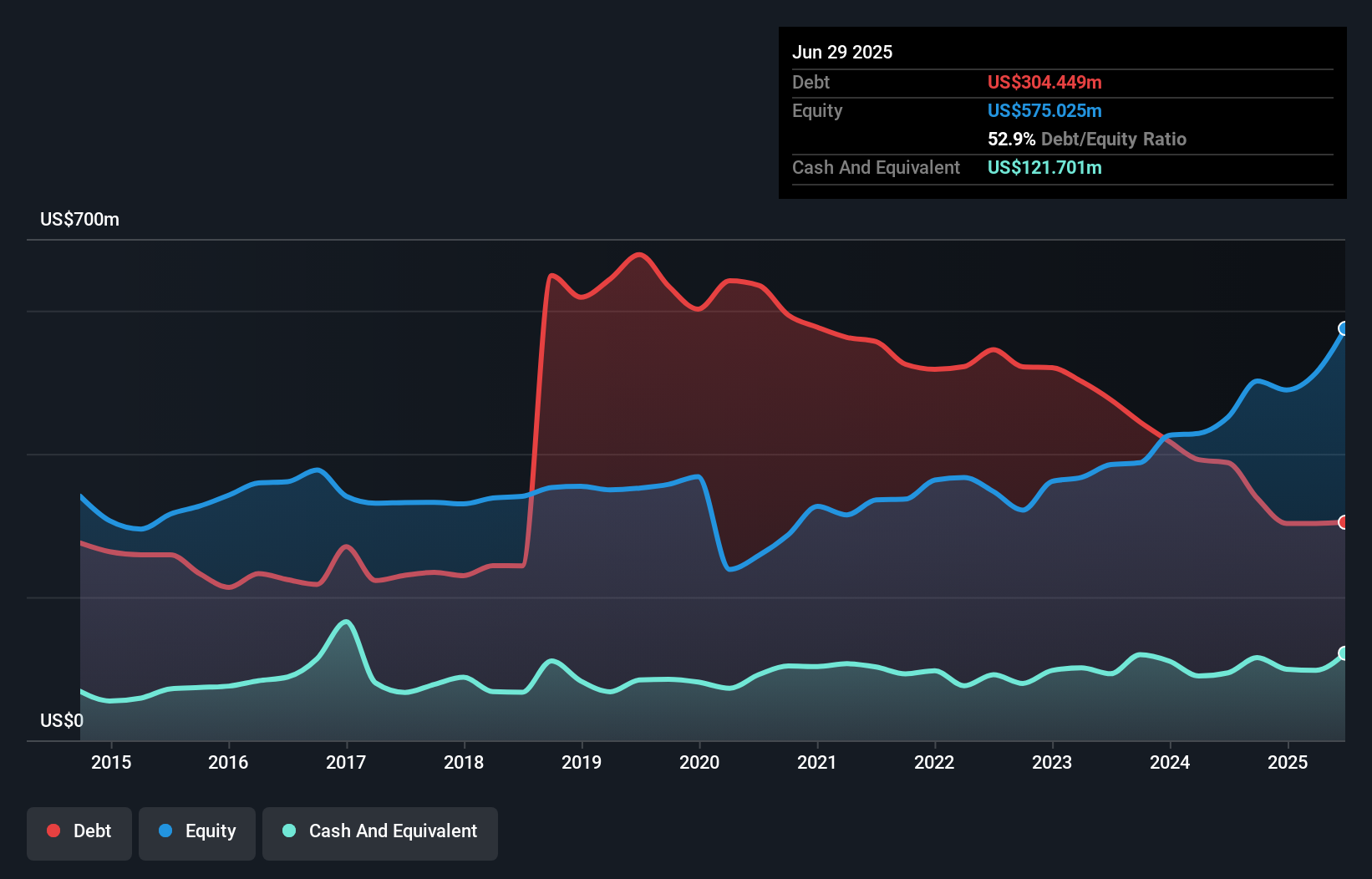

Willdan Group, a notable player in the professional services sector, has demonstrated impressive financial performance with earnings growing by 131.8% over the past year, significantly outpacing industry growth of 3.8%. The firm is currently trading at 41.7% below its estimated fair value and boasts high-quality earnings with free cash flow positivity. Its debt management appears robust, as evidenced by a reduction in the debt-to-equity ratio from 67.3% to 15.9% over five years and more cash than total debt on hand. Recent initiatives include a $49 million energy contract with Mt. San Antonio College and expansion into telecommunications programs for Puget Sound Energy, highlighting strategic growth through diversification and infrastructure projects that leverage its proprietary technology solutions for long-term revenue stability.

Interface (TILE)

Simply Wall St Value Rating: ★★★★★★

Overview: Interface, Inc. is a company that designs, produces, and sells modular carpet products across various regions including the United States, Canada, Latin America, Europe, Africa, Asia, and Australia with a market capitalization of $1.49 billion.

Operations: The company's revenue primarily comes from the Americas segment, contributing $843.89 million, and the Europe, Africa, Asia, and Australia (EAAA) segment with $542.97 million.

Interface stands out in the flooring industry with its focus on sustainable products, such as the newly launched noravant™, a PVC-free resilient flooring solution. The company reported strong financial performance for 2025, with net income rising to US$116.1 million from US$86.95 million in 2024 and basic earnings per share increasing to US$1.99 from US$1.49. Interface's strategic initiatives, including potential M&A activities and the One Interface Strategy, aim to bolster market penetration and operational efficiency while maintaining a satisfactory net debt to equity ratio of 17.2%. Recent share repurchases totaling 3.63% reflect confidence in future prospects.

Next Steps

- Click here to access our complete index of 329 US Undiscovered Gems With Strong Fundamentals.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com