- LIVE QUOTES

- LEARN

- HELP

EN

Did Piper Sandler's Upgrade Just Shift FB Financial's (FBK) Investment Narrative?

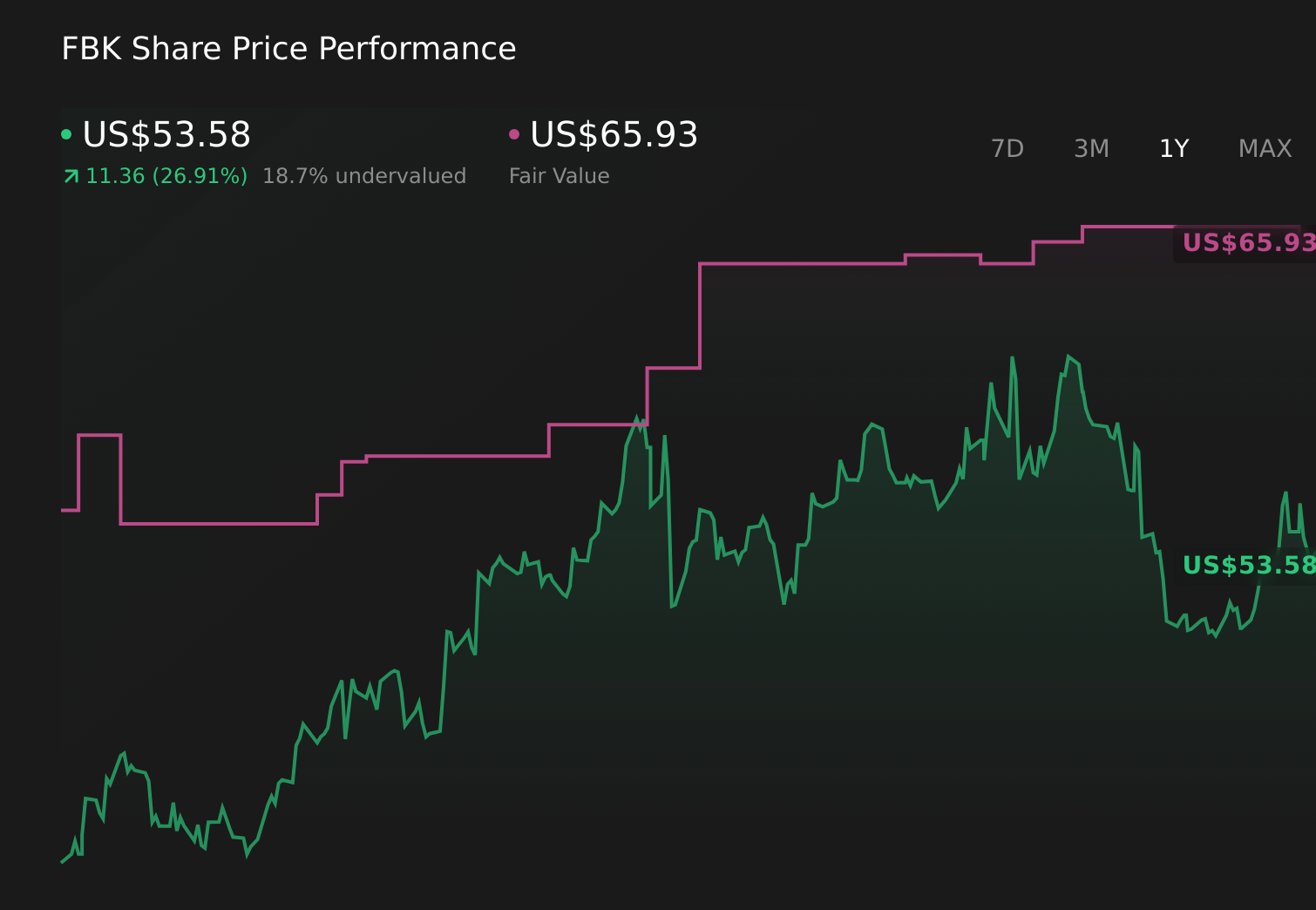

- Piper Sandler analyst Stephen Scouten recently upgraded FB Financial to a buy rating, while keeping his existing US$65 price target unchanged.

- The upgrade comes from an analyst with a year-long track record of relatively strong success and average returns, which may carry weight with investors assessing FB Financial’s outlook.

- We’ll now examine how this vote of confidence from a well-regarded analyst interacts with FB Financial’s existing investment narrative and assumptions.

Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

FB Financial Investment Narrative Recap

To own FB Financial, you need to be comfortable with a regional bank that is leaning into growth through the Southern States merger, active capital return and revenue-producing hires, while managing integration, credit and funding risks. Piper Sandler’s upgrade does not fundamentally change the near term focus on executing the merger and controlling credit costs, but it may reinforce confidence around those existing catalysts rather than introduce a new one.

The recent completion of the Southern States merger in July 2025 looks most relevant here, as it directly ties into the scale and earnings potential many analysts, including Scouten, are assessing. Investors now have to weigh the promised benefits of a larger footprint and loan book against the operational and credit integration challenges that could influence both returns and the pace of any future capital deployment.

Yet investors should be aware that the integration of Southern States could still...

Read the full narrative on FB Financial (it's free!)

FB Financial’s narrative projects $940.8 million revenue and $358.1 million earnings by 2029.

Uncover how FB Financial's forecasts yield a $66.58 fair value, a 25% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community span a wide range, from about US$66.58 up to roughly US$112.03 per share. When you set these against the merger integration and credit quality risks discussed above, it becomes clear that opinions can differ sharply, and it is worth exploring several viewpoints before forming your own.

Explore 2 other fair value estimates on FB Financial - why the stock might be worth just $66.58!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your FB Financial research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free FB Financial research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate FB Financial's overall financial health at a glance.

Interested In Other Possibilities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- AI is about to change healthcare. These 36 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com