- LIVE QUOTES

- LEARN

- HELP

EN

A Look At FLEX LNG (NYSE:FLNG) Valuation As New Flex Aurora Charter Extends Earnings Visibility

FLEX LNG (NYSE:FLNG) has secured a new time charter for its Flex Aurora vessel with a global Supermajor. The agreement is a two-year firm deal with options that could extend employment through 2034.

See our latest analysis for FLEX LNG.

The new charter lands at a time when FLEX LNG’s share price has a 90-day share price return of 23.31% and a 1-year total shareholder return of 67.73%. This suggests momentum has been building around the stock’s income and contract visibility story.

If this time charter has you thinking about other energy infrastructure ideas, it may be worth scanning opportunities in liquefied gas, tankers, and related plays via the 28 power grid technology and infrastructure stocks

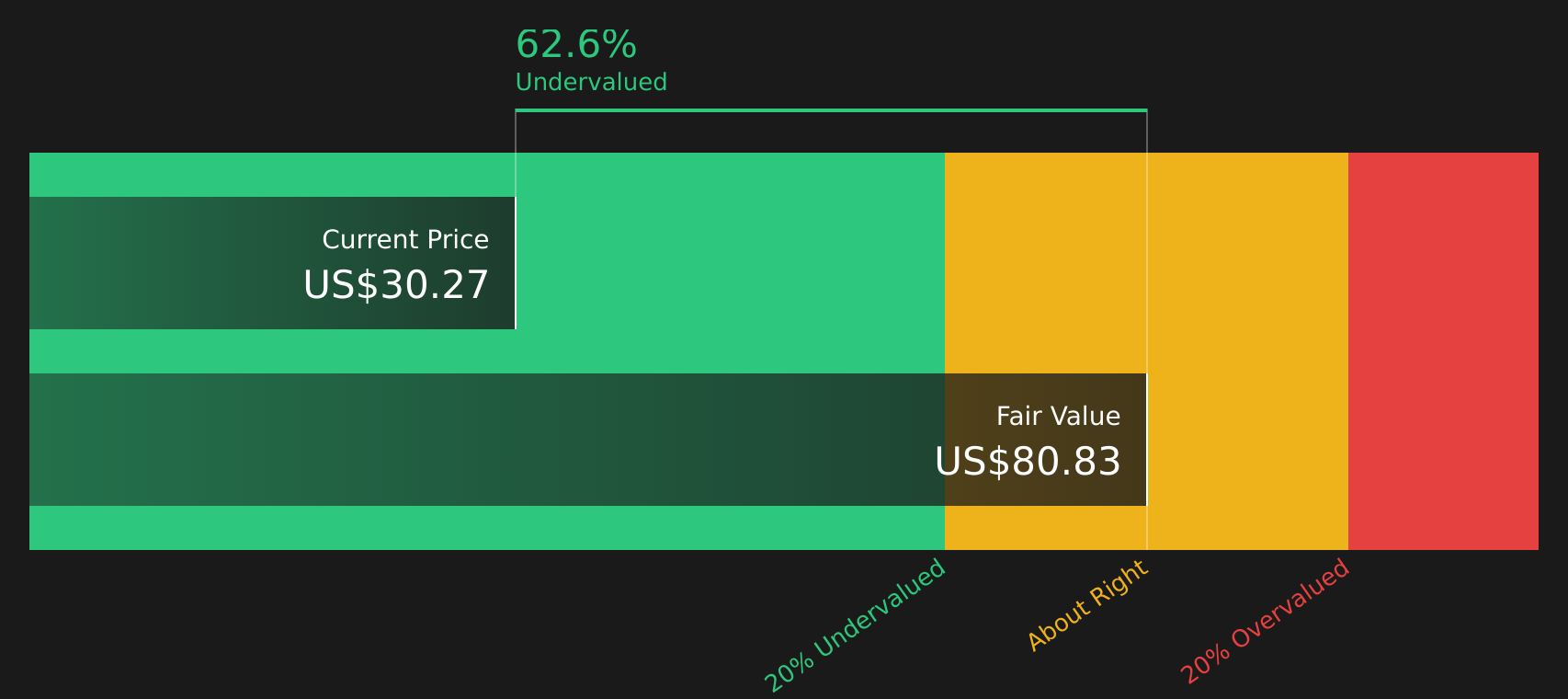

With FLNG up 67.73% over the past year and trading above the average analyst price target, yet flagged with an intrinsic discount of 73.21%, investors have to ask whether there is still a buying opportunity here or whether the market is already pricing in future growth.

Most Popular Narrative: 16.6% Overvalued

With FLEX LNG last closing at $30.47 against a narrative fair value of $26.13, the prevailing view is that expectations already sit ahead of the modelled outlook.

The analysts have a consensus price target of $26.12 for FLEX LNG based on their expectations of its future earnings growth, profit margins and other risk factors. In order for you to agree with the analysts, you would need to believe that by 2029, revenues will be $366.6 million, earnings will come to $137.3 million, and it would be trading on a PE ratio of 12.9x, assuming you use a discount rate of 7.8%.

Want to see what kind of revenue path and margin rebuild need to line up to back that fair value, and how the future earnings multiple fits into it? The full narrative sets out the earnings runway, profitability shift, and valuation bridge that sit behind this overvaluation call.

Result: Fair Value of $26.13 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you still need to weigh the risk that around 300 new LNG vessels could pressure charter rates, while high payouts may limit flexibility for fleet renewal and debt reduction.

Find out about the key risks to this FLEX LNG narrative.

Another View: Cash Flows Tell a Very Different Story

The narrative fair value of $26.13 suggests FLNG is 16.6% overvalued, while the SWS DCF model points to a future cash flow value of $113.73 per share. That is a wide gap for the same company, so which set of assumptions do you trust more?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out FLEX LNG for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 58 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With such a wide spread between sentiment, cash flow models, and contract news, this is the moment to look through the numbers yourself and move quickly to shape your own view using the 2 key rewards and 3 important warning signs.

Looking for more investment ideas?

Do not stop at a single stock story. Use focused stock lists to quickly spot opportunities that match your income needs, risk appetite, and quality filters.

- Zero in on resilient compounders by scanning the 58 high quality undervalued stocks that pair quality with pricing that still looks reasonable.

- Strengthen your income stream by reviewing the 13 dividend fortresses that combine higher yields with supporting fundamentals.

- Prioritise capital protection by filtering for the 68 resilient stocks with low risk scores that score well on financial health and business stability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com