- LIVE QUOTES

- LEARN

- HELP

EN

Is Strong Q4 Execution And New UK P&A Contract Altering The Investment Case For Helix (HLX)?

- In recent days, Helix Energy Solutions Group reported fourth-quarter results with revenue slightly lower year on year but materially ahead of analyst expectations on EPS and EBITDA, while also securing a multi-year well plug and abandonment program in the UK North Sea.

- At the same time, rising crude prices amid heightened U.S.–Iran tensions have drawn attention to how geopolitical risk can influence demand for Helix’s offshore services and earnings potential.

- We’ll now examine how Helix’s strong quarter and new UK North Sea decommissioning contract may influence its existing investment narrative.

Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

Helix Energy Solutions Group Investment Narrative Recap

To own Helix today, you generally need to believe that long term demand for offshore well intervention and decommissioning will offset short term contract timing and margin pressure. The recent earnings beat and new UK North Sea plug and abandonment contract support that thesis near term, while the key risks remain project deferrals, spot market exposure, and cost inflation. Geopolitically driven oil price moves may influence sentiment, but they do not materially change Helix’s core risk profile right now.

The multi year UK North Sea plug and abandonment award for up to 34 subsea wells looks especially relevant, because it directly addresses one of Helix’s main catalysts: building a more visible backlog in decommissioning to smooth earnings volatility. Coming on the heels of a quarter where EBITDA outpaced expectations despite softer revenue, this contract underpins near term asset utilization and offers a counterweight to concerns about delayed awards elsewhere.

Yet, against this positive contract momentum, investors should still watch the risk that stricter environmental regulations and policy uncertainty in the UK North Sea could materially delay projects and pressure returns...

Read the full narrative on Helix Energy Solutions Group (it's free!)

Helix Energy Solutions Group's narrative projects $1.4 billion revenue and $103.0 million earnings by 2028. This requires 2.9% yearly revenue growth and about a $52.9 million earnings increase from $50.1 million today.

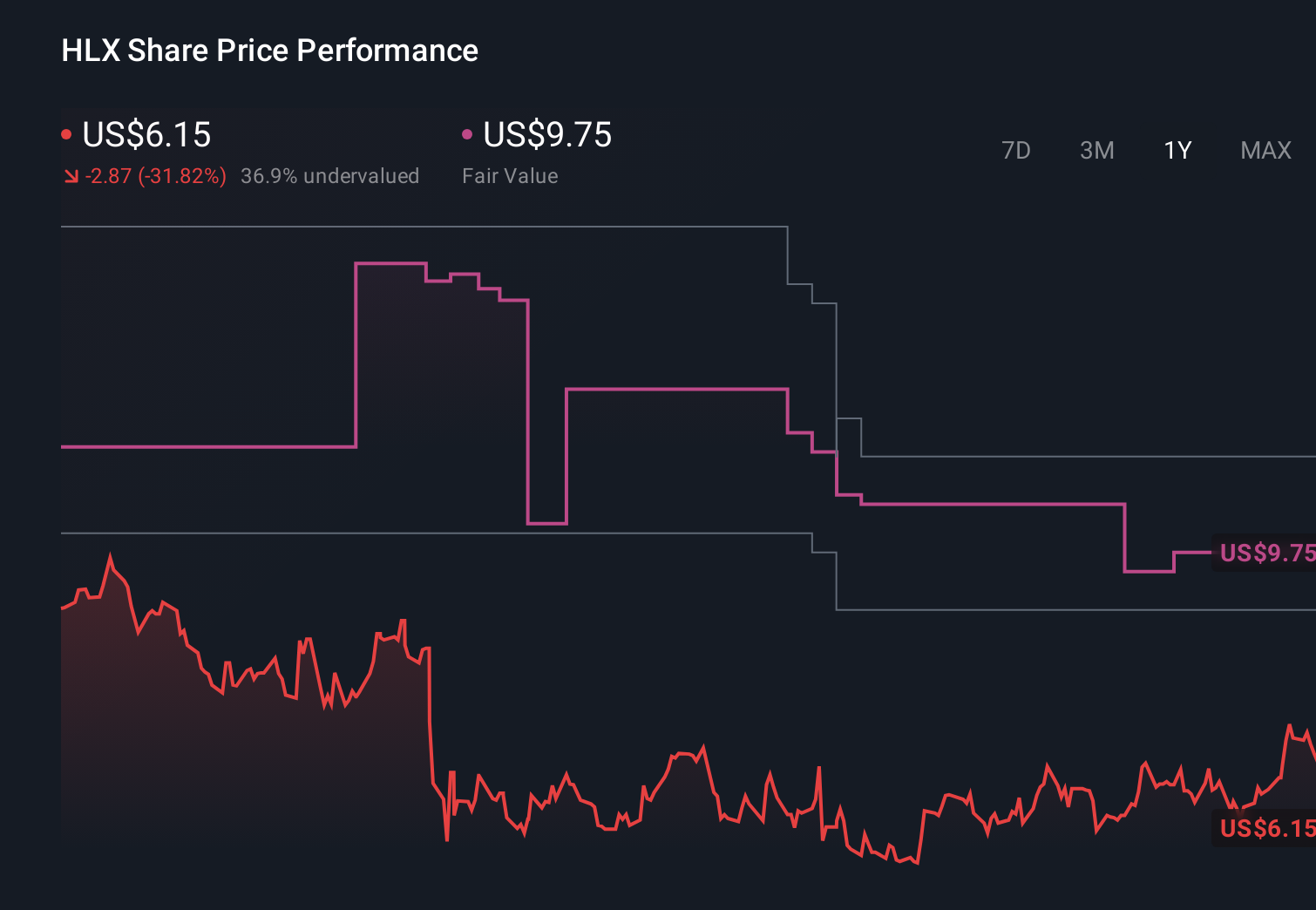

Uncover how Helix Energy Solutions Group's forecasts yield a $9.75 fair value, in line with its current price.

Exploring Other Perspectives

By contrast, the most optimistic analysts were already modeling revenue around US$1.4 billion and earnings near US$114 million by 2028, so you should recognize that some forecasts assume regulatory driven decommissioning demand and robotics growth far outpacing today’s consensus and that both bullish and cautious views may need updating as this latest contract win and geopolitical backdrop feed into new expectations.

Explore 4 other fair value estimates on Helix Energy Solutions Group - why the stock might be worth 27% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Helix Energy Solutions Group research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Helix Energy Solutions Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Helix Energy Solutions Group's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Find 58 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com