- LIVE QUOTES

- LEARN

- HELP

EN

A Look At Stellar Bancorp (STEL) Valuation After Early Redemption Of Subordinated Notes

Stellar Bancorp (STEL) recently redeemed the remaining $30.0 million of its 4.70% fixed to floating rate subordinated notes due 2029, simplifying its capital structure and removing this interest bearing obligation earlier than scheduled.

See our latest analysis for Stellar Bancorp.

The share price is at $36.62, and while the 1 day share price return is slightly negative, the 90 day share price return of 19.05% and 1 year total shareholder return of 49.82% point to momentum that has been building over time.

If this kind of rerating catches your attention, it could be a good moment to widen your watchlist with 20 top founder-led companies

With the shares at $36.62 and only a small discount to the $38.00 analyst target, plus a recent 1 year total return near 50%, you have to ask: is there still value here, or is the market already pricing in future growth?

Most Popular Narrative: 3.6% Undervalued

With Stellar Bancorp at $36.62 versus a narrative fair value of $38.00, the gap is small but it still reflects a modest upside case built on specific operating assumptions.

Investors seem to discount the challenge of rising compliance, technology, and ESG-related costs, as increased regulatory and stakeholder requirements may outpace operational leverage improvements, resulting in longer-term net margin compression.

Curious what justifies a higher fair value despite these cost pressures? Revenue expectations, margin assumptions and the future earnings multiple all pull in different directions, and the full narrative shows how they are reconciled.

Result: Fair Value of $38 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this fair value story still leans on smooth merger execution and branch relevance, both of which could be tested by digital competitors and regional shocks.

Find out about the key risks to this Stellar Bancorp narrative.

Another View: Multiples Point to a Richer Price

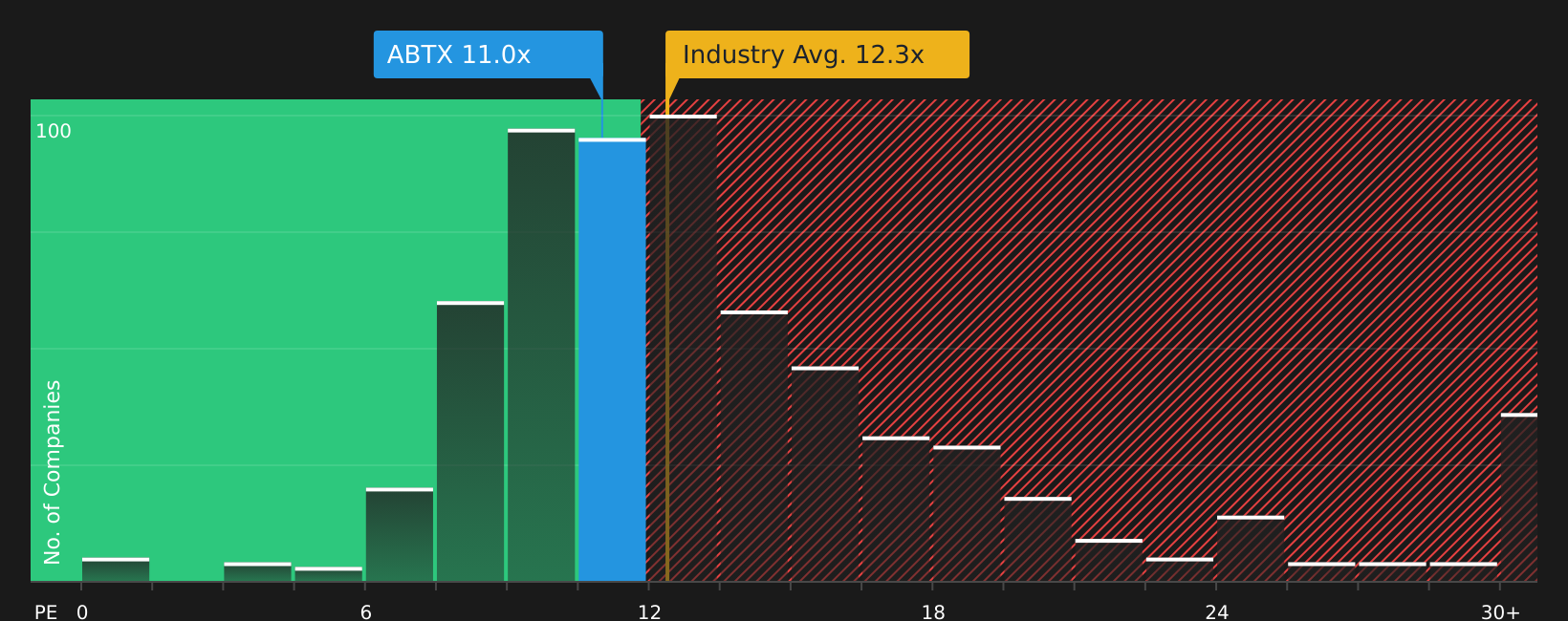

While the narrative fair value suggests 3.6% upside to $38.00, the current P/E of 18.1x tells a tougher story. It sits above the US Banks average of 11.4x and a fair ratio of 11.1x, which implies less cushion if sentiment or earnings expectations cool.

To see what the numbers say about this valuation gap and how much room there might be for the P/E to move toward the fair ratio, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment clearly mixed between opportunity and concern, it helps to move fast and test the numbers yourself so you are not relying on headlines alone. To see how the current story balances potential upside with the risks on investors' minds, review the 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If you stop here, you only see part of the opportunity set, so take a few minutes to scan other ideas and keep your watchlist working harder.

- Target potential value upside by reviewing 59 high quality undervalued stocks that combine quality fundamentals with prices that may not fully reflect them.

- Boost your income focus by checking out 13 dividend fortresses that pair 5%+ yields with an emphasis on resilience.

- Protect your downside by scanning 68 resilient stocks with low risk scores built around stronger balance sheets and lower overall risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com