- LIVE QUOTES

- LEARN

- HELP

EN

Does Alignment Healthcare's (ALHC) Mixed Quarter Clarify or Cloud Its Medicare Advantage Scale Ambitions?

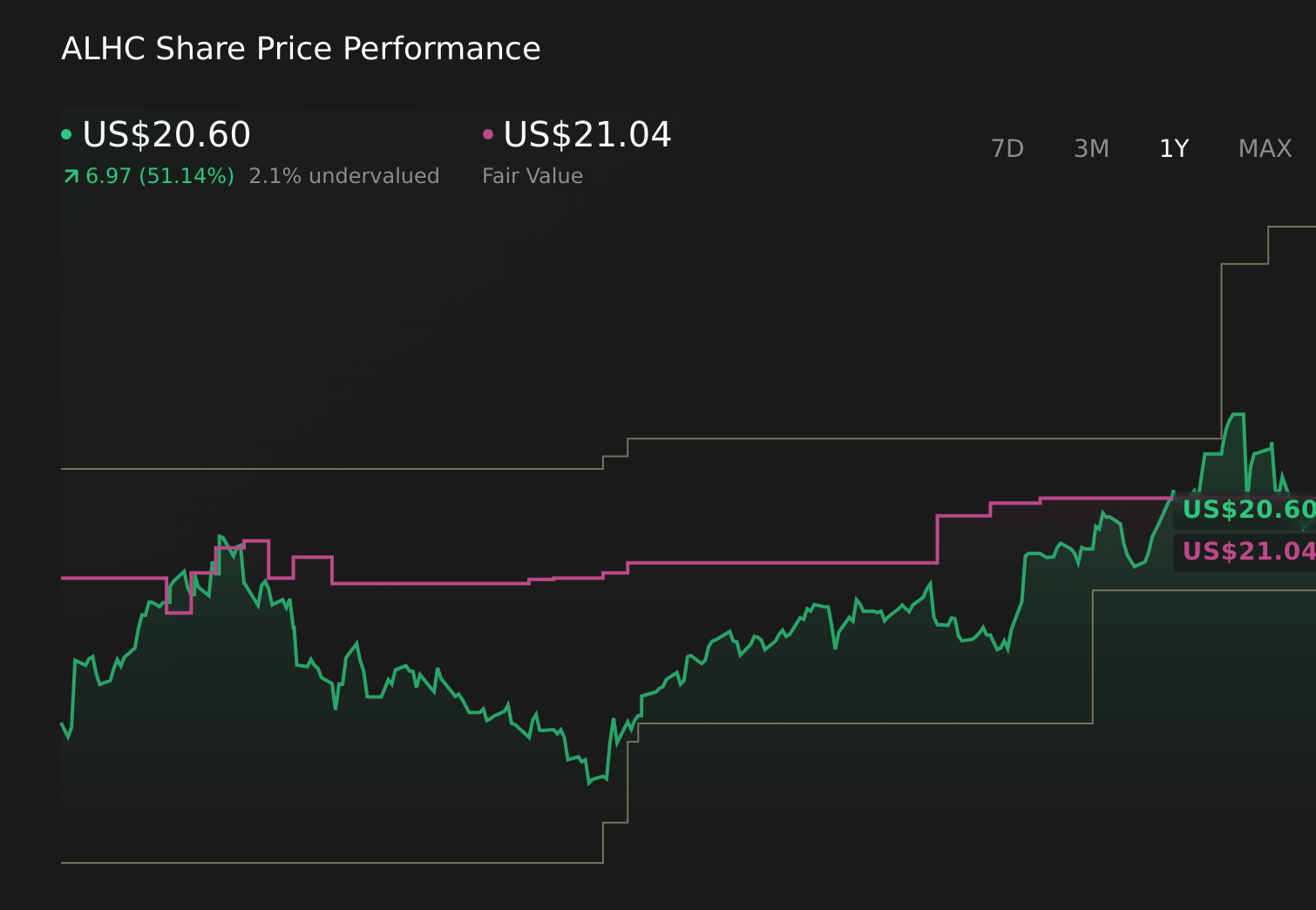

- Alignment Healthcare recently reported quarterly results showing revenue up 44.4% year on year and earnings per share above analyst estimates, while also updating guidance that implied weaker-than-expected revenue for the next quarter.

- Alongside this mixed earnings picture, the company highlighted ongoing expansion of its Medicare Advantage offerings and national footprint, underscoring a continued push to scale its coordinated, technology-enabled care model.

- Next, we’ll explore how this combination of strong recent revenue growth and softer forward guidance may reshape Alignment Healthcare’s investment narrative.

Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

Alignment Healthcare Investment Narrative Recap

To own Alignment Healthcare, you have to believe its technology-driven Medicare Advantage model can turn rapid revenue growth into durable profitability while withstanding reimbursement and regulatory pressure. The latest quarter’s strong 44.4% revenue increase and EPS beat support the growth side of that story, but the softer revenue guidance and 8.5% share price pullback keep execution risk front and center, especially around scaling efficiently and managing medical costs in the near term.

Among recent announcements, the completed US$256.2 million follow-on equity offering stands out. For a business still posting small net losses, this extra capital can help fund market expansion, technology investment, and cushion near term volatility, which matters more now that guidance has come in below expectations and investors are watching how growth and margin improvement are funded.

But while the growth story is appealing, investors should be aware that tighter Medicare Advantage reimbursement, rising competition, and the risk that heavy tech spending does not translate into...

Read the full narrative on Alignment Healthcare (it's free!)

Alignment Healthcare’s narrative projects $8.0 billion revenue and $151.5 million earnings by 2029. This requires 26.5% yearly revenue growth and an earnings increase of about $152 million from -$724.0 thousand today.

Uncover how Alignment Healthcare's forecasts yield a $25.50 fair value, a 36% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were looking for revenue of about US$8.2 billion and earnings of roughly US$252.7 million by 2028, which paints a far rosier picture than the more cautious consensus. If you are intrigued by that upside, the latest guidance miss and stock reaction could either challenge those bullish assumptions or simply mark a bump in the road, so it is worth comparing how different viewpoints weigh membership growth, margin expansion, and regulatory risk before deciding which story you find more convincing.

Explore 2 other fair value estimates on Alignment Healthcare - why the stock might be worth over 2x more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Alignment Healthcare research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Alignment Healthcare research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Alignment Healthcare's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- This technology could replace computers: discover 25 stocks that are working to make quantum computing a reality.

- AI is about to change healthcare. These 37 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com