- LIVE QUOTES

- LEARN

- HELP

EN

Coterra Energy (CTRA) Valuation Check After Q4 Earnings And Oil Price Volatility

Recent Q4 earnings and fresh moves in oil prices after U.S. Iran tensions eased have pushed Coterra Energy (CTRA) into focus, giving you a live case study in how geopolitics and fundamentals interact.

See our latest analysis for Coterra Energy.

Coterra’s share price has been volatile around these oil headlines and Q4 results, with a 1 month share price return of 11.84% and a year to date gain of 29.92%. The 5 year total shareholder return of 151.27% points to momentum that has built over a longer stretch.

If the recent move in energy stocks has you thinking more broadly about commodity producers, it could be a good time to scan 28 elite gold producer stocks

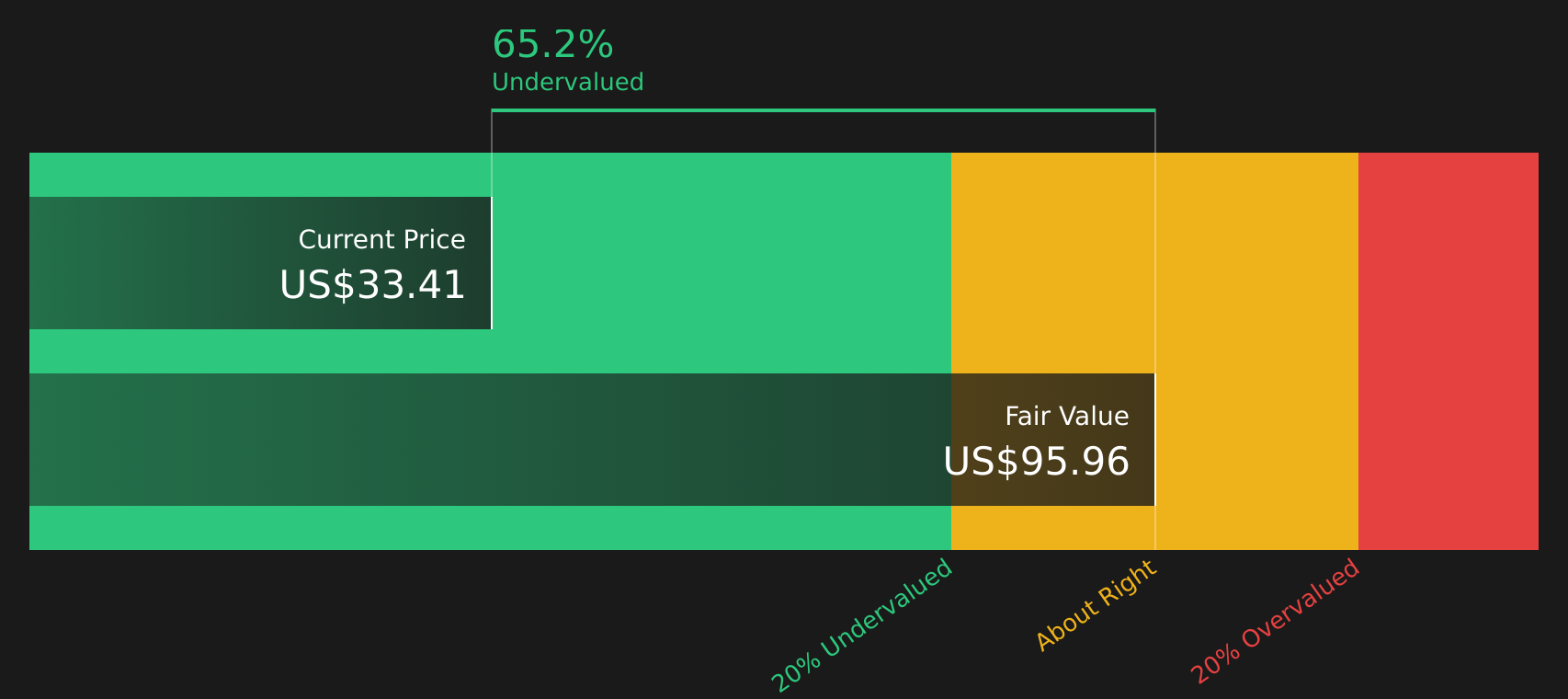

Coterra now trades at $34.56, with a reported intrinsic value gap of about 68% and a modest discount of roughly 8% to consensus price targets. This raises the question of whether this reflects genuine undervaluation or whether the market is already accounting for future growth.

Most Popular Narrative: 35.3% Overvalued

According to Bejgal, the narrative fair value for Coterra Energy of $25.55 sits well below the current $34.56 share price, which frames the current enthusiasm very differently to the market.

In 3 years, Coterra is likely to solidify its position as a leading energy producer with enhanced capital efficiency and diversified revenue streams. By 5 years, the company could see robust earnings growth driven by the LNG market and efficient oil production. Over 10 years, its extensive inventory and focus on innovation position it for sustainable long-term growth.

Curious what kind of LNG driven revenue path justifies a fair value well below today’s price? The narrative leans heavily on margin rich barrels and disciplined capital use.

Result: Fair Value of $25.55 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, LNG market disruptions or tighter environmental rules in key regions could quickly challenge the earnings story and call that 35.3% overvaluation view into question.

Find out about the key risks to this Coterra Energy narrative.

Another View: Cash Flows Point the Other Way

Bejgal’s narrative flags Coterra as 35.3% overvalued at a fair value of $25.55, yet our DCF model points in the opposite direction, with a fair value estimate of $106.57. That gap suggests the market could be heavily discounting future cash flows. Which story do you trust more?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

Mixed signals so far, right? If you want to move beyond headlines and models, it makes sense to review the 3 key rewards and 1 important warning sign.

Looking for more investment ideas?

If you only stop at Coterra, you risk missing other opportunities that may better match your goals, risk comfort, and income needs across the market.

- Target potential value opportunities by scanning 62 high quality undervalued stocks that combine quality fundamentals with pricing that may not fully reflect their underlying strength.

- Strengthen your focus on capital preservation by reviewing 67 resilient stocks with low risk scores that score well on financial resilience and lower historical risk indicators.

- Broaden your opportunity set by checking screener containing 25 high quality undiscovered gems that have solid fundamentals but receive relatively limited market attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com