- LIVE QUOTES

- LEARN

- HELP

EN

A Look At DuPont De Nemours (DD) Valuation After Recent Share Price Volatility

Why DuPont de Nemours (DD) is on investors’ radar today

Recent share performance has put DuPont de Nemours (DD) back in focus. The stock has shown a 5.8% decline over the past month and an 11.3% gain in the past 3 months.

See our latest analysis for DuPont de Nemours.

At a share price of US$45.48, DuPont de Nemours has seen short term share price pressure with a 30 day share price return of a 5.8% decline, while longer term momentum is reflected in an 11.3% year to date share price return and a 63.7% 1 year total shareholder return.

If this kind of rebound story interests you, it can be useful to look at other companies with strong themes behind them, including 28 power grid technology and infrastructure stocks

With DuPont de Nemours trading at US$45.48 and sitting at around a 25% discount to one intrinsic value estimate along with a similar gap to analyst targets, investors may ask whether this represents a value opportunity or whether the market is already pricing in future growth.

Most Popular Narrative: 19% Undervalued

At a last close of $45.48 against a narrative fair value of $56.13, DuPont de Nemours is framed as undervalued, with the story leaning heavily on future cash generation supported by higher margins and steadier growth.

The company's renewed portfolio focus post Qnity spin and recent divestitures in non core segments enables greater resource allocation to high growth specialty businesses, contributing to improved operating margin and increased earnings stability. DuPont's robust innovation pipeline, including content and share gains in advanced nodes and the water tech portfolio, underpins premium pricing opportunities and sustainably enhances gross margins over the medium to long term.

Want to see what this means in hard numbers? The narrative hinges on measured revenue expansion, a sharp margin reset, and a richer earnings multiple anchored by a specific discount rate. The full breakdown shows exactly how those ingredients stack up into that fair value.

Result: Fair Value of $56.13 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this story can be knocked off course if PFAS related legal actions escalate, or if Qnity and other portfolio moves leave earnings more volatile.

Find out about the key risks to this DuPont de Nemours narrative.

Another Angle on DuPont de Nemours’ Valuation

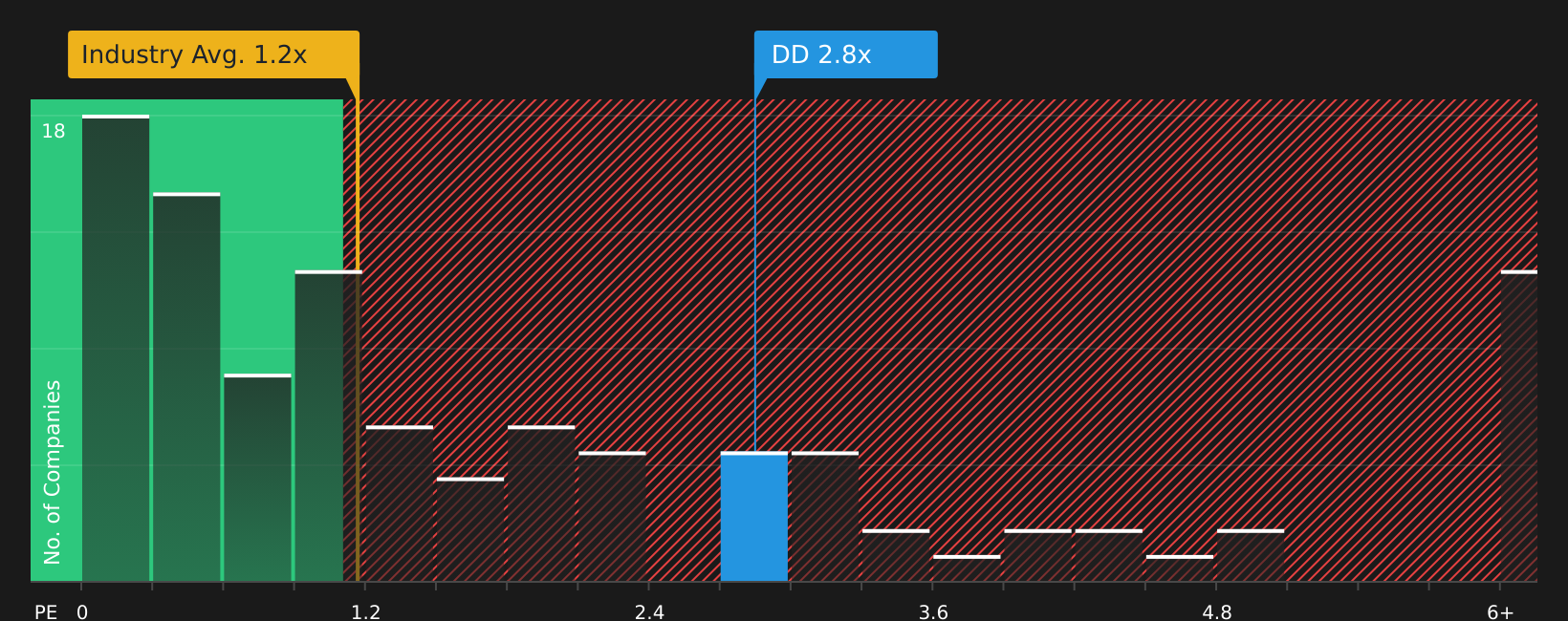

While the narrative fair value points to DuPont de Nemours looking undervalued, the P/S ratio tells a more cautious story. At 2.7x, it sits above both peers at 2.2x and the US Chemicals industry at 1.1x, even though the fair ratio is 3x. This raises the question of whether the market is pricing in extra risk or leaving some room on the table for patient investors.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Mixed signals or a clear opportunity: the only opinion that really counts is yours, so take a closer look at the data behind the 4 key rewards and 2 important warning signs

Looking for more investment ideas?

If you stop with just one stock, you could miss out on other opportunities that fit your style. Widen your search using focused sets of potential ideas.

- Spot potential bargains early by scanning a curated group of quality names that currently look mispriced with the 62 high quality undervalued stocks.

- Strengthen your income plan by reviewing companies that pair higher yields with resilience through the 12 dividend fortresses.

- Limit unwanted surprises by focusing on businesses with sturdier finances using the solid balance sheet and fundamentals stocks screener (39 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com