- LIVE QUOTES

- LEARN

- HELP

EN

Is Devon’s Extended, Cheaper Credit Line Quietly Reframing Its Capital Allocation Playbook (DVN)?

- On March 24, 2026, Devon Energy amended its syndicated credit facility, extending the maturity to March 24, 2031 and removing the 10 basis point SOFR credit spread adjustment while renewing options for three additional one-year extensions, subject to lender approval.

- This refinancing slightly lowers Devon’s borrowing costs and lengthens liquidity visibility, which can support capital allocation flexibility across commodity cycles.

- With this extended, lower-cost credit line in place, we’ll now assess how it interacts with Devon Energy’s existing investment narrative and risk profile.

We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Devon Energy Investment Narrative Recap

To own Devon Energy, you need to believe that its U.S. shale portfolio and free cash flow can support ongoing shareholder returns despite commodity and regulatory uncertainty. The new credit facility modestly improves financial flexibility and liquidity visibility, but it does not materially change the near term earnings catalyst or core risk around Devon’s dependence on hydrocarbon prices and high decline rate shale assets.

The most relevant recent development here is Devon’s continued use of its repurchase program, with about 15% of shares bought back since late 2021. Pairing a long dated, lower cost credit line with active buybacks can matter for near term sentiment, as investors weigh balance sheet capacity against the ongoing need to reinvest heavily just to sustain production.

Yet, while this new credit support looks helpful on the surface, investors should still be alert to the risk that...

Read the full narrative on Devon Energy (it's free!)

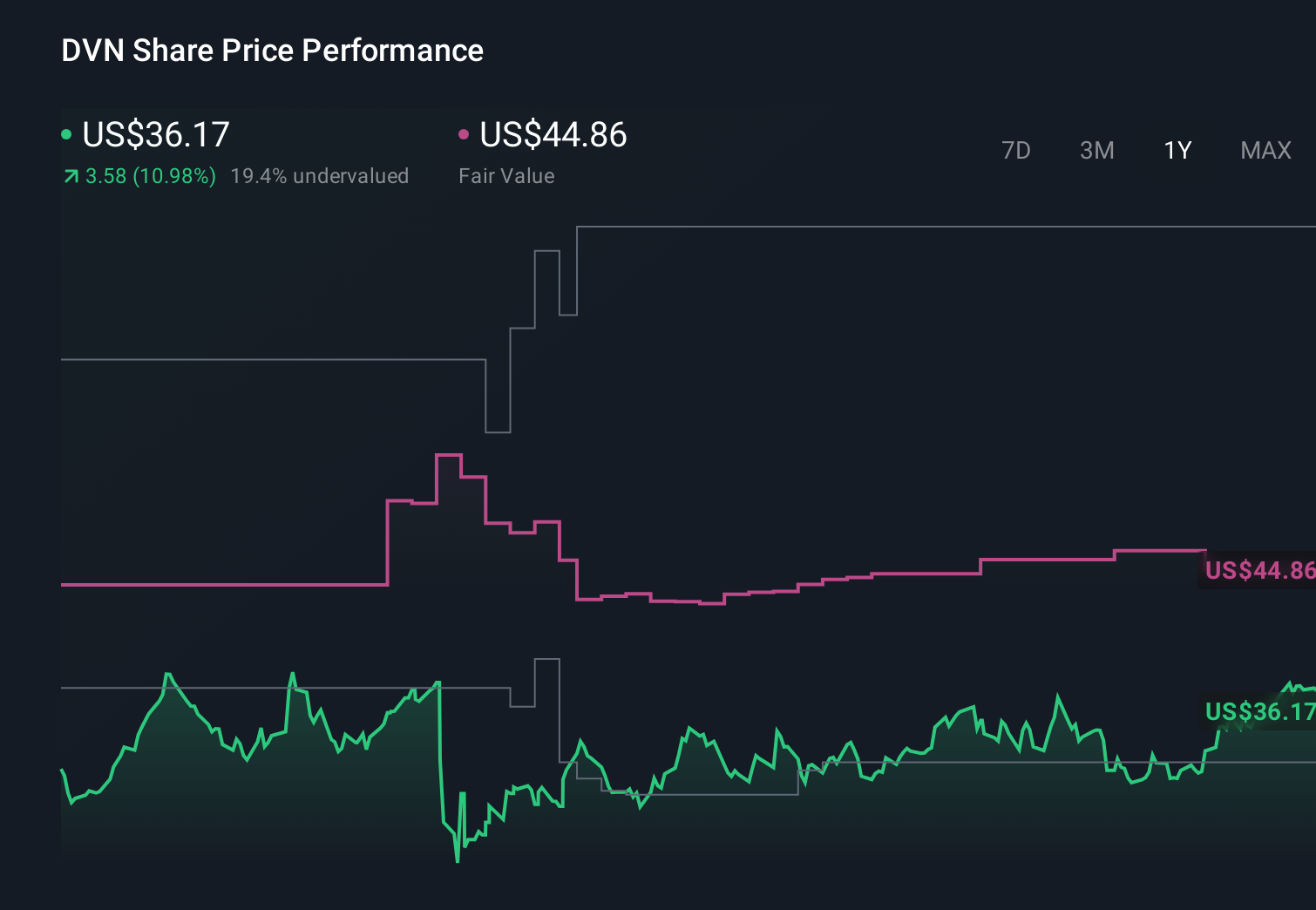

Devon Energy's narrative projects $19.3 billion revenue and $3.0 billion earnings by 2028. This requires 6.3% yearly revenue growth and a roughly $0.2 billion earnings increase from $2.8 billion today.

Uncover how Devon Energy's forecasts yield a $44.34 fair value, a 10% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts paint a far more cautious picture than the consensus, even before this credit amendment, assuming Devon’s revenue only reaches about US$20.3 billion and earnings about US$3.2 billion by 2029, which could still be revisited once the impact of cheaper, longer dated bank funding and the risk of stranded shale assets are fully weighed.

Explore 6 other fair value estimates on Devon Energy - why the stock might be worth over 4x more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Devon Energy research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Devon Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Devon Energy's overall financial health at a glance.

No Opportunity In Devon Energy?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com