- LIVE QUOTES

- LEARN

- HELP

EN

Discovering US Undiscovered Gems in April 2026

Over the last 7 days, the United States market has remained flat, yet it boasts an impressive 16% growth over the past year, with earnings expected to increase by 15% annually in the coming years. In this promising environment, identifying stocks that are not only resilient but also poised for growth can uncover hidden opportunities within a dynamic and evolving landscape.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| First Bancorp | 68.18% | 1.28% | -2.88% | ★★★★★★ |

| Southern Michigan Bancorp | 110.47% | 7.93% | 2.26% | ★★★★★★ |

| Oakworth Capital | 26.12% | 15.98% | 13.01% | ★★★★★★ |

| Sound Financial Bancorp | 16.27% | 0.75% | -13.28% | ★★★★★★ |

| TON Strategy | NA | -43.33% | 47.02% | ★★★★★★ |

| First Northern Community Bancorp | NA | 7.53% | 11.34% | ★★★★★★ |

| Winchester Bancorp | 121.44% | 49.13% | 3283.33% | ★★★★★★ |

| Union Bankshares | 374.44% | 1.11% | -7.71% | ★★★★★☆ |

| NameSilo Technologies | 12.63% | 14.48% | 3.12% | ★★★★★☆ |

| Pure Cycle | 5.42% | 9.36% | -2.03% | ★★★★★☆ |

Underneath we present a selection of stocks filtered out by our screen.

Bank First (BFC)

Simply Wall St Value Rating: ★★★★★★

Overview: Bank First Corporation functions as a holding company for Bank First, N.A., with a market capitalization of approximately $1.51 billion.

Operations: The primary revenue stream for Bank First Corporation is its banking operations, generating $172.63 million.

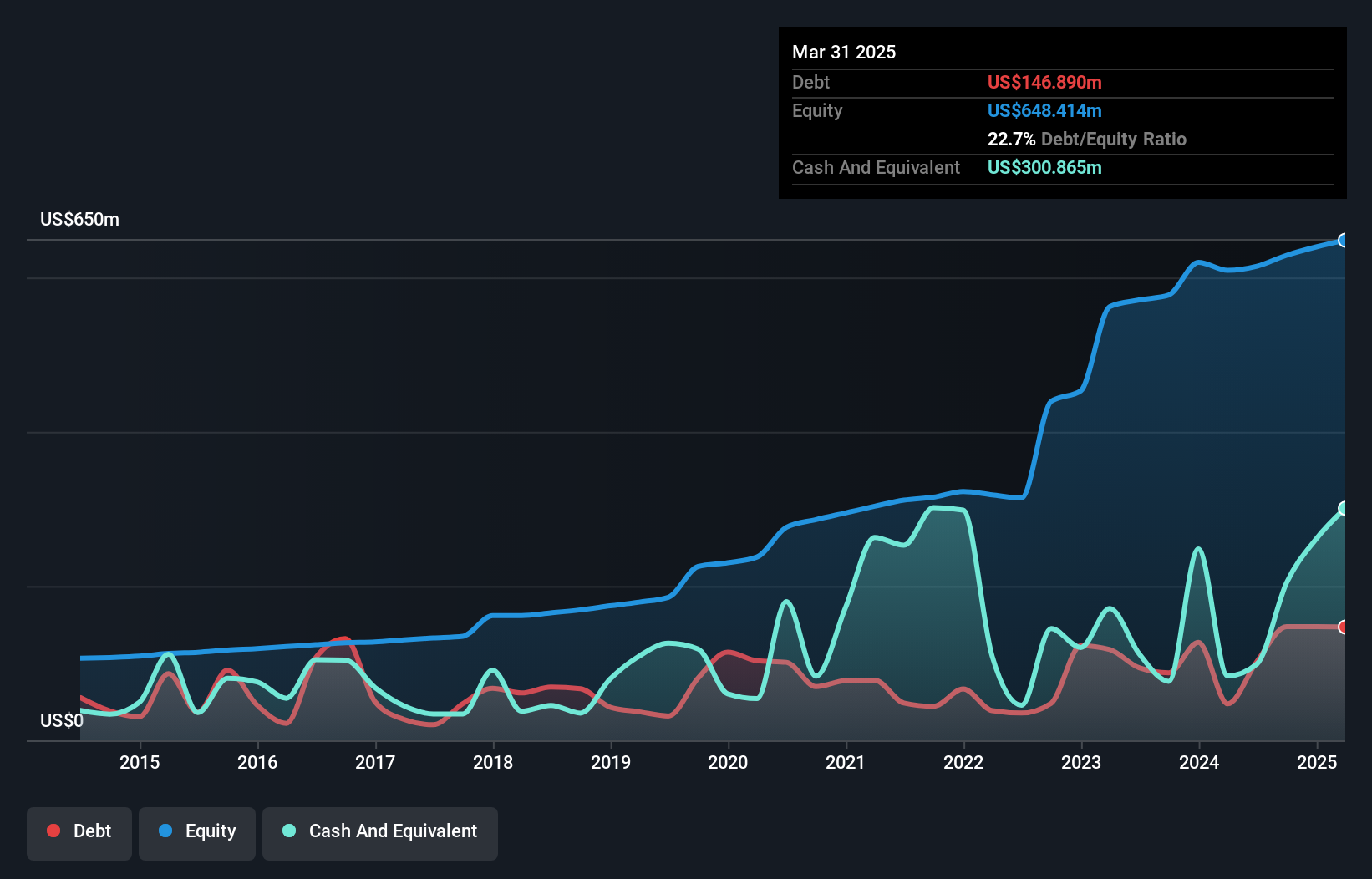

Bank First, with assets totaling US$4.5 billion and equity of US$643.8 million, stands out with its robust financial health. Its total deposits are US$3.7 billion against loans of US$3.6 billion, showcasing a balanced approach to lending and borrowing. The bank's net interest margin is 3.8%, supported by a sufficient allowance for bad loans at 0.3% of total loans, indicating prudent risk management practices in place. Over the past five years, earnings have grown at an impressive rate of 14% annually despite not outperforming the industry last year; it trades attractively below estimated fair value by nearly 25%.

- Take a closer look at Bank First's potential here in our health report.

Evaluate Bank First's historical performance by accessing our past performance report.

CRA International (CRAI)

Simply Wall St Value Rating: ★★★★☆☆

Overview: CRA International, Inc. offers economic, financial, and management consulting services globally and has a market cap of approximately $1.06 billion.

Operations: CRA International generates revenue primarily from professional and consulting services, amounting to $751.58 million.

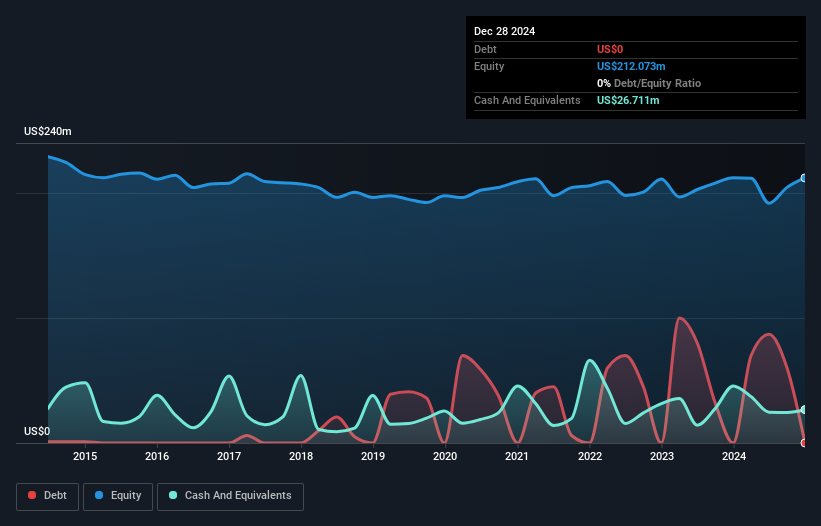

CRA International, a nimble player in the professional services arena, showcases impressive earnings growth of 16.8% over the past year, outpacing its industry peers' 2.8%. The company's net debt to equity ratio stands at a satisfactory 7.4%, indicating robust financial health despite an increase from 0.2% five years ago to 15.9%. With EBIT covering interest payments by a substantial margin of 15.5 times, CRA's strong financial footing is evident. Recent insider selling may raise eyebrows; however, trading at approximately half its estimated fair value suggests potential for significant upside as it navigates complex regulatory landscapes and M&A activity demands.

Republic Bancorp (RBCA.A)

Simply Wall St Value Rating: ★★★★★★

Overview: Republic Bancorp, Inc. is a bank holding company for Republic Bank & Trust Company, offering a range of banking products and services in the United States, with a market capitalization of approximately $1.38 billion.

Operations: Republic Bancorp generates revenue primarily from its Core Banking segment, with Traditional Banking contributing $268.16 million and Warehouse Lending adding $14.20 million. The Republic Processing Group (RPG) further diversifies income through Tax Refund Solutions at $38.97 million, Republic Credit Solutions at $47.67 million, and Republic Payment Solutions at $16.91 million.

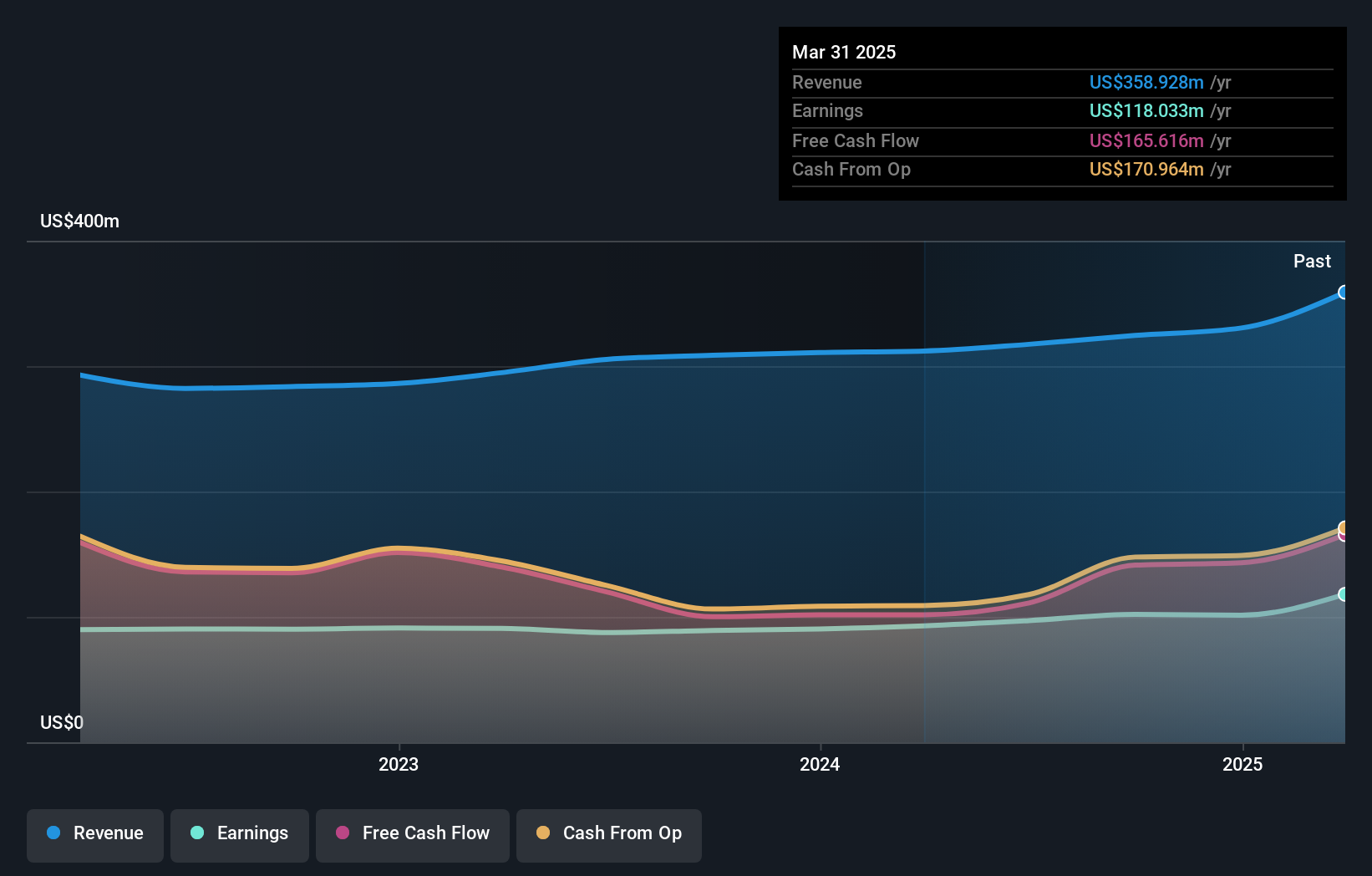

Republic Bancorp, with assets totaling $7 billion and equity of $1.1 billion, showcases a robust financial profile. The bank's total deposits stand at $5.2 billion against loans of $5.4 billion, highlighting its lending focus. Its allowance for bad loans is an impressive 356%, with non-performing loans at just 0.4%. Despite a forecasted earnings dip averaging 3.8% annually over the next three years, last year's earnings surged by 29.5%, outpacing the industry average of 20.2%. Recently added to the S&P Regional Banks Select Industry Index, it also increased dividends by 10%, reflecting confidence in its future prospects.

- Dive into the specifics of Republic Bancorp here with our thorough health report.

Explore historical data to track Republic Bancorp's performance over time in our Past section.

Make It Happen

- Get an in-depth perspective on all 330 US Undiscovered Gems With Strong Fundamentals by using our screener here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com