- LIVE QUOTES

- LEARN

- HELP

EN

Did Middle East-Linked Sales Weakness and Insider Buying Just Shift Coty's (COTY) Investment Narrative?

- In late March 2026, BofA reduced its outlook on Coty, citing weaker sales tied to the Middle East conflict, while Coty’s Interim CEO Markus Strobel publicly acknowledged that recent performance has fallen short of expectations despite the company’s strong brands and innovation pipeline.

- On March 6, 2026, Coty’s President of Consumer Beauty Von Bretten bought 83,000 Coty shares, signaling internal confidence even as external analysts raised concerns about sales trends and execution.

- We’ll now look at how Coty’s weaker sales linked to the Middle East conflict could reshape its existing investment narrative.

Explore 25 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Coty Investment Narrative Recap

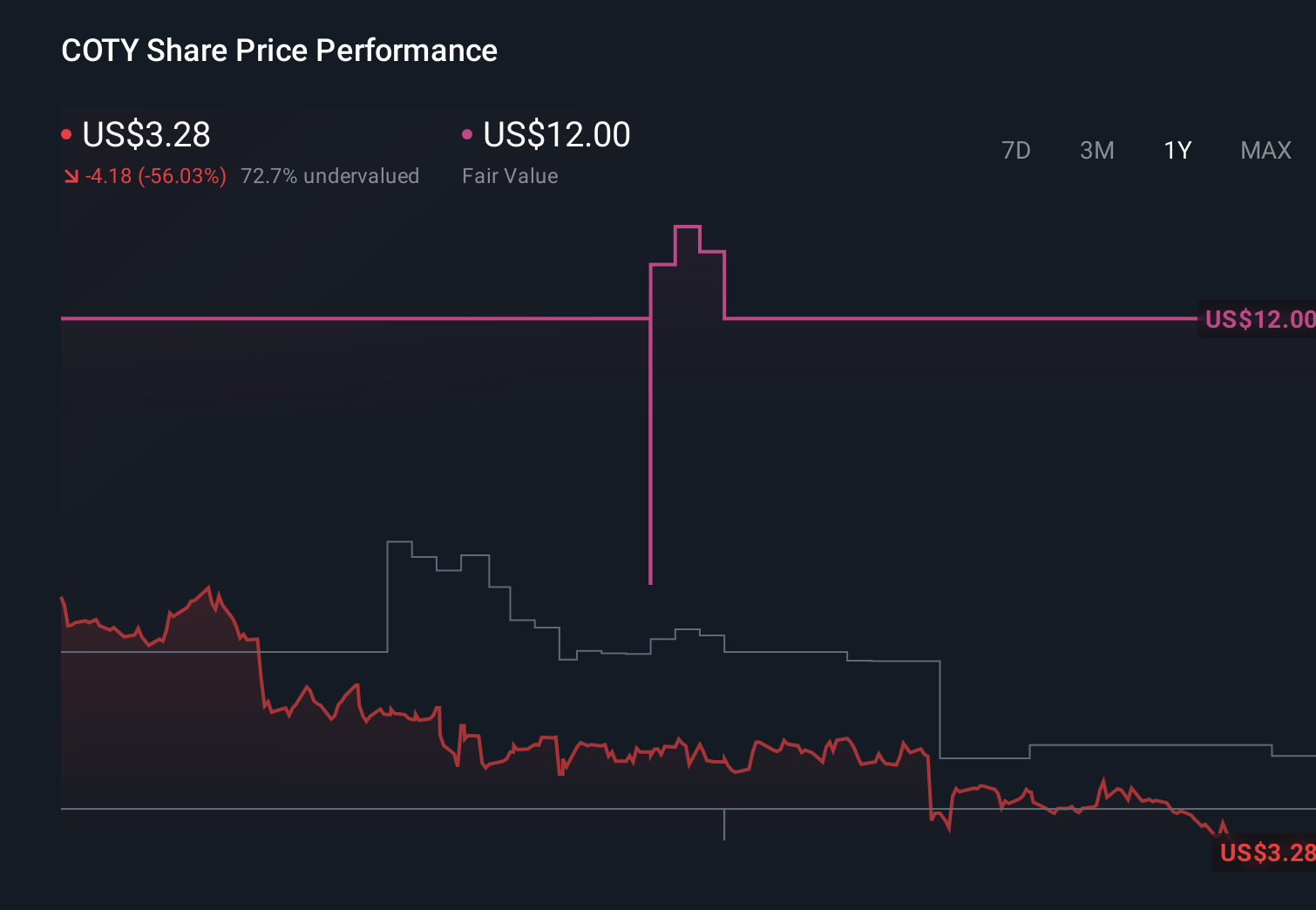

To own Coty today, you need to believe its portfolio of established beauty brands and licensing deals can translate into improving profitability once temporary pressures ease. The recent BofA downgrade highlights how Middle East related sales weakness adds to existing concerns about execution and near term sales trends. In my view, the most important short term catalyst remains evidence that like for like revenues can stabilize, while the key risk is that ongoing demand softness and regional disruptions further delay that turn.

Against this backdrop, Von Bretten’s purchase of 83,000 Coty shares in early March stands out as especially relevant. It arrives just weeks after Coty guided to a mid single digit like for like revenue decline for Q3 FY2026 and as the Interim CEO acknowledged disappointing performance. For investors, that combination of internal share buying and cautious guidance creates a clear focal point: upcoming results will need to show whether sales weakness linked to the Middle East conflict is temporary or more entrenched.

Yet investors should also be aware that the biggest emerging risk may be how prolonged regional disruptions interact with already fragile margins and high leverage...

Read the full narrative on Coty (it's free!)

Coty's narrative projects $6.1 billion revenue and $302.1 million earnings by 2028. This requires 1.3% yearly revenue growth and a $683.2 million earnings increase from $-381.1 million today.

Uncover how Coty's forecasts yield a $4.56 fair value, a 123% upside to its current price.

Exploring Other Perspectives

Before this setback, the most optimistic analysts were assuming Coty could lift annual revenue to about US$6.4 billion and earnings to roughly US$372.4 million, but the new Middle East driven weakness raises fresh questions about whether those more aggressive growth and margin expectations still hold, especially if prestige fragrance dependence and regional volatility remain pressure points.

Explore 6 other fair value estimates on Coty - why the stock might be worth just $3.27!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Coty research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Coty research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Coty's overall financial health at a glance.

Seeking Other Investments?

Our top stock finds are flying under the radar-for now. Get in early:

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 22 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com