- LIVE QUOTES

- LEARN

- HELP

EN

Is WTW’s New WELL Facility Reframing Its AI-Enabled Growth Narrative in Complex Risk Markets?

- Recently, Willis Towers Watson launched the Willis Excess Liability Lineslip (WELL) facility, offering up to $50 million in combined lead umbrella and first excess liability capacity via a single London-market policy for large and complex U.S. casualty risks.

- This move, alongside organizational changes to sharpen specialization and accelerate AI-driven innovation, highlights how WTW is using product design and operating model changes to tackle capacity constraints and evolving client needs in complex risk markets.

- We’ll now examine how the WELL facility’s expanded umbrella capacity could influence WTW’s existing investment narrative around AI-enabled growth.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 22 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Willis Towers Watson Investment Narrative Recap

To own Willis Towers Watson, you need to believe it can keep deepening its role as a specialist risk and advisory partner while using technology to stay differentiated from global peers. The WELL facility supports this story by showcasing product innovation and London-market syndication strength, but it does not materially change the near term focus on AI-enabled productivity as a key catalyst or the risk of fee pressure if core services become more commoditized.

Among recent developments, WTW’s appointment of Tammy Richardson to lead its global AI transformation stands out as particularly relevant to WELL, since both underline a push to embed analytics and technology into specialty solutions. Together, these moves sit squarely within the existing catalyst of growing demand for advanced risk management and consulting, while still leaving investors to weigh ongoing competitive pressure from Marsh McLennan and Aon, and the potential for pricing compression in highly contested segments.

Yet investors also need to be aware that rising automation in broking and consulting could compress fees faster than Willis Towers Watson can offset with...

Read the full narrative on Willis Towers Watson (it's free!)

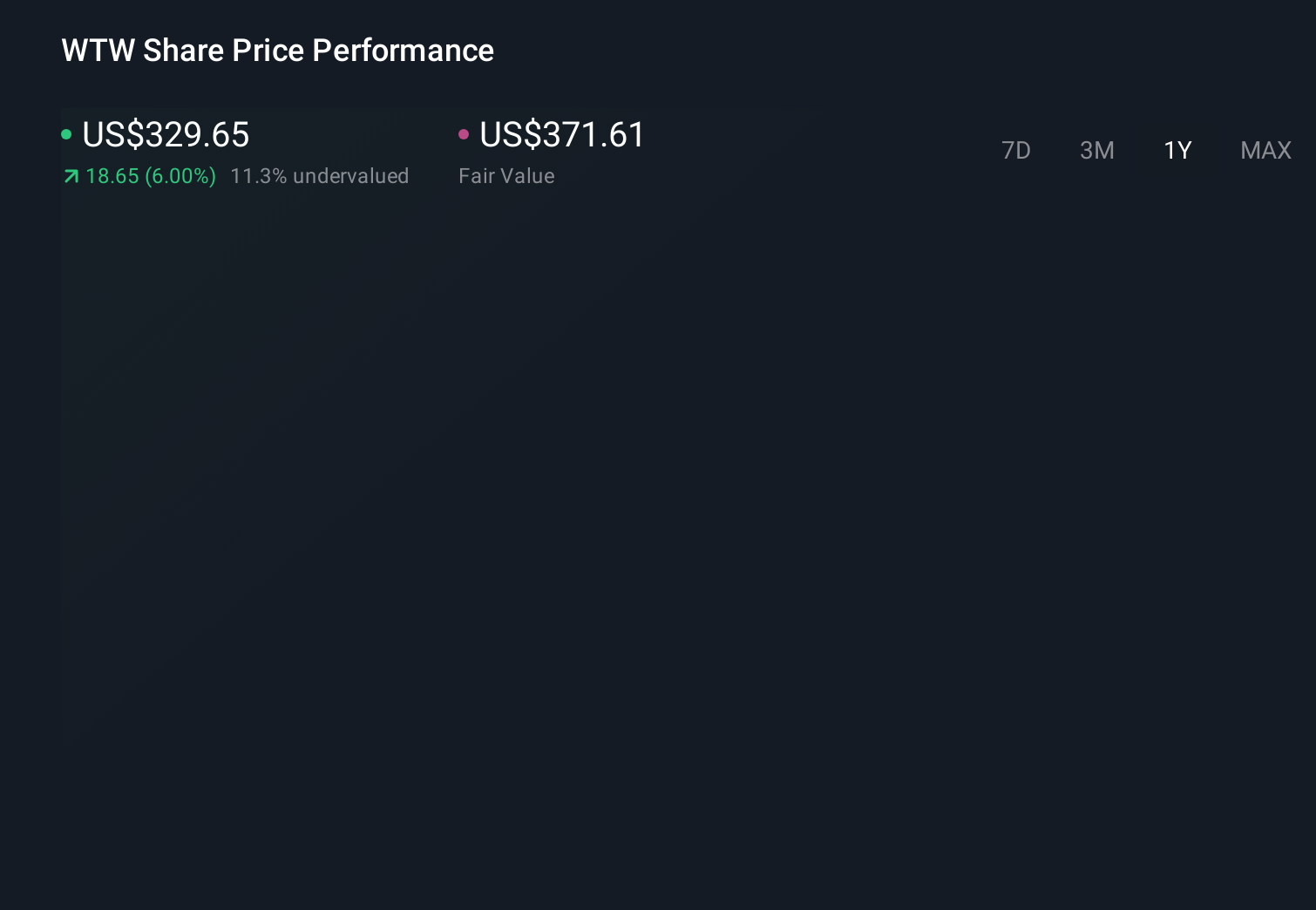

Willis Towers Watson's narrative projects $11.9 billion revenue and $1.8 billion earnings by 2029.

Uncover how Willis Towers Watson's forecasts yield a $370.63 fair value, a 29% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community span a wide range, from about US$187 to roughly US$371 per share, showing how far apart individual views can be. You should weigh those opinions against the catalyst that WTW is leaning on AI enabled solutions like WELL to reinforce its differentiation in complex risk markets, which could be critical if competition intensifies and pricing pressure builds.

Explore 2 other fair value estimates on Willis Towers Watson - why the stock might be worth as much as 29% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Willis Towers Watson research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Willis Towers Watson research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Willis Towers Watson's overall financial health at a glance.

Want Some Alternatives?

Our top stock finds are flying under the radar-for now. Get in early:

- Find 63 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com