- LIVE QUOTES

- LEARN

- HELP

EN

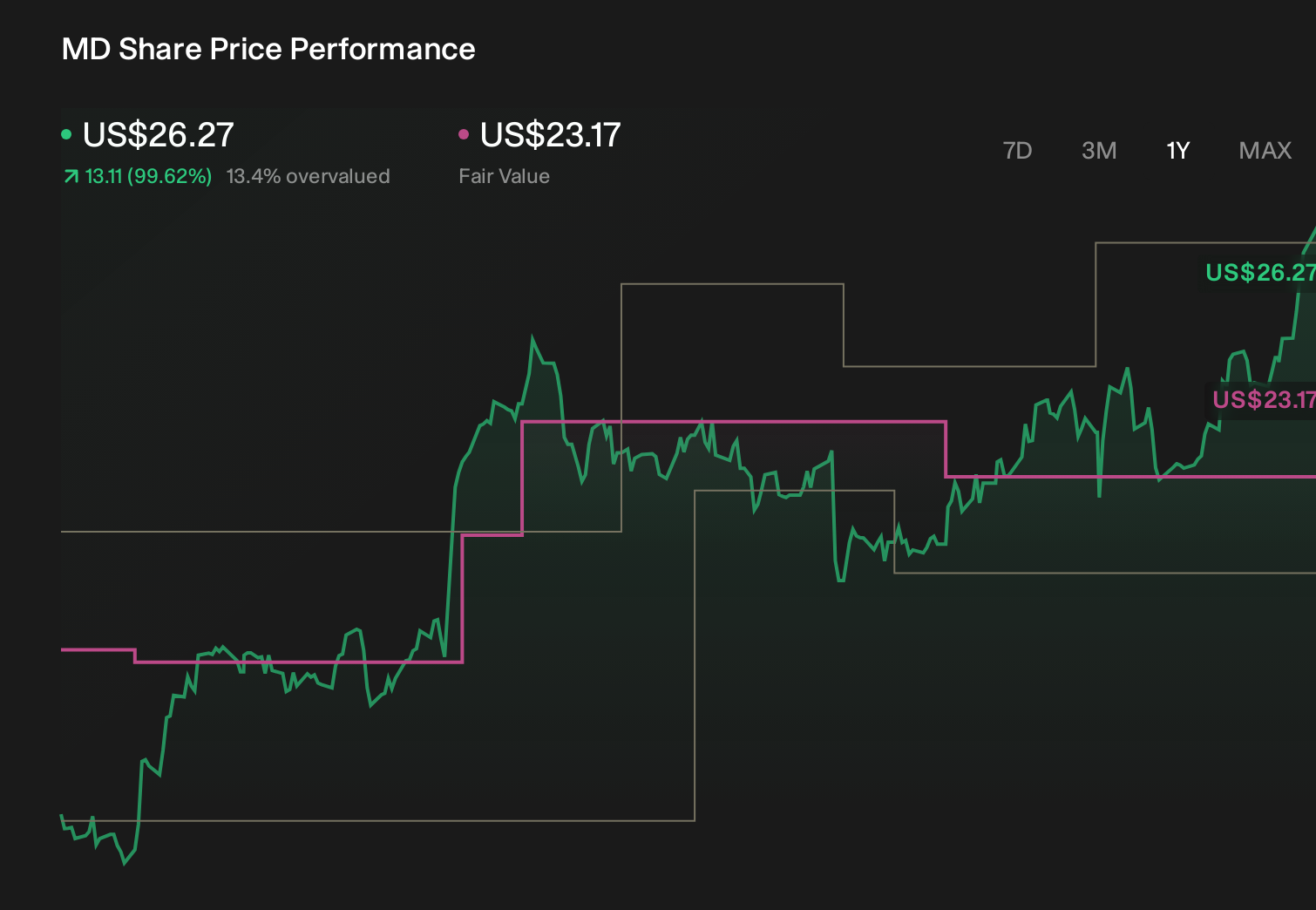

Did Pediatrix’s Earnings-Accretive Tennessee MFM Deal Just Shift Pediatrix Medical Group’s (MD) Investment Narrative?

- In late March 2026, Pediatrix Medical Group, Inc. expanded its presence in Middle Tennessee by acquiring Tennessee Maternal-Fetal Medicine in a cash deal, integrating five Greater Nashville locations and a ten-provider team under the Maternal-Fetal Medicine Specialists of Tennessee banner, with the transaction expected to be immediately accretive to earnings.

- This move reinforces Pediatrix’s focus on high-acuity maternal-fetal care and broader regional coverage, potentially enhancing its capacity-driven growth profile and perceived resilience in specialized women’s and neonatal health services.

- Next, we will examine how this earnings-accretive maternal-fetal partnership could reshape Pediatrix Medical Group’s investment narrative and future expectations.

Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

Pediatrix Medical Group Investment Narrative Recap

To own Pediatrix Medical Group, you have to believe its focus on high-acuity neonatal and maternal-fetal care can offset revenue pressure from portfolio restructuring, payer dynamics, and rising labor costs. The Tennessee Maternal-Fetal Medicine acquisition looks helpful for near term earnings, but does not remove the core risk around hospital and payer pushback on fees and reimbursement, which remains central to the story.

The recent hiring of James Barry, M.D., as Chief Clinical Quality & Transformation Officer and Jochen Profit, M.D., as Chief Quality Advisor ties directly into this earnings-accretive expansion. If these leaders can translate quality, AI, and outcomes-focused initiatives into better reimbursement terms and hospital partnerships, they could reinforce the key catalyst of more efficient operations and resilient margins, complementing acquisitions like the Middle Tennessee deal.

Yet, beneath these positive headlines, there is a structural risk around payer and hospital fee pressure that investors should be aware of...

Read the full narrative on Pediatrix Medical Group (it's free!)

Pediatrix Medical Group's narrative projects $2.1 billion revenue and $171.4 million earnings by 2029. This requires 2.6% yearly revenue growth and a modest $6.0 million earnings increase from $165.4 million today.

Uncover how Pediatrix Medical Group's forecasts yield a $21.33 fair value, in line with its current price.

Exploring Other Perspectives

Before this news, the most optimistic analysts were expecting Pediatrix to reach about US$2.2 billion of revenue and US$159 million of earnings by 2028, but they were also more concerned about long term birth rate pressure and payment model shifts, so their story around this acquisition could end up looking very different from the more cautious consensus view.

Explore 4 other fair value estimates on Pediatrix Medical Group - why the stock might be worth less than half the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Pediatrix Medical Group research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Pediatrix Medical Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Pediatrix Medical Group's overall financial health at a glance.

Looking For Alternative Opportunities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

- Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 21 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com