- LIVE QUOTES

- LEARN

- HELP

EN

US Undiscovered Gems To Watch In March 2026

Over the last 7 days, the United States market has dropped 3.5%, yet it remains up by 14% over the past year, with earnings anticipated to grow by 15% annually in the coming years. In this dynamic environment, identifying stocks that are not only resilient but also poised for growth can be a rewarding strategy for investors seeking potential opportunities.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| First Bancorp | 68.18% | 1.28% | -2.88% | ★★★★★★ |

| Morris State Bancshares | 1.94% | 4.43% | 2.90% | ★★★★★★ |

| Cashmere Valley Bank | 31.17% | 5.25% | 1.74% | ★★★★★★ |

| Oakworth Capital | 26.12% | 15.98% | 13.01% | ★★★★★★ |

| Sound Financial Bancorp | 16.27% | 0.75% | -13.28% | ★★★★★★ |

| Affinity Bancshares | 42.51% | 1.82% | 1.11% | ★★★★★★ |

| First Northern Community Bancorp | NA | 7.53% | 11.34% | ★★★★★★ |

| Seneca Foods | 38.64% | 2.39% | -18.65% | ★★★★★☆ |

| NameSilo Technologies | 12.63% | 14.48% | 3.12% | ★★★★★☆ |

| Pure Cycle | 5.42% | 9.36% | -2.03% | ★★★★★☆ |

We're going to check out a few of the best picks from our screener tool.

Northeast Bank (NBN)

Simply Wall St Value Rating: ★★★★★★

Overview: Northeast Bank offers a range of banking services to individual and corporate clients in Maine, with a market capitalization of $930.82 million.

Operations: Revenue from banking services amounts to $213.09 million.

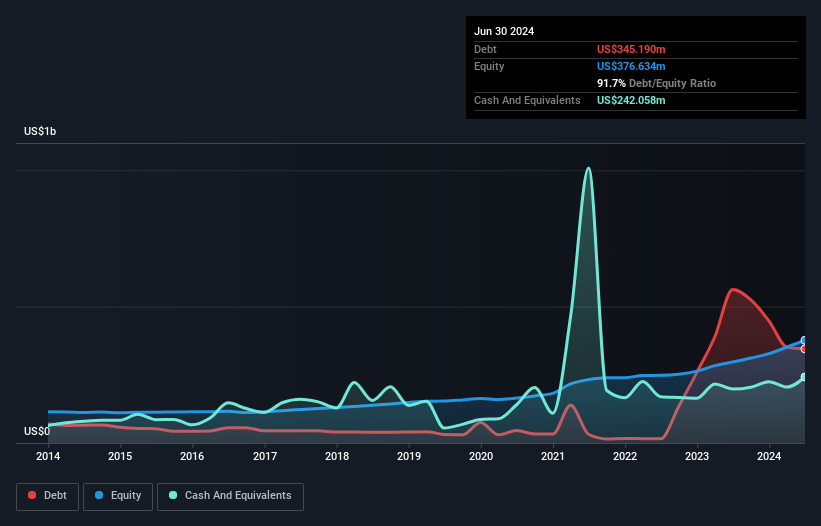

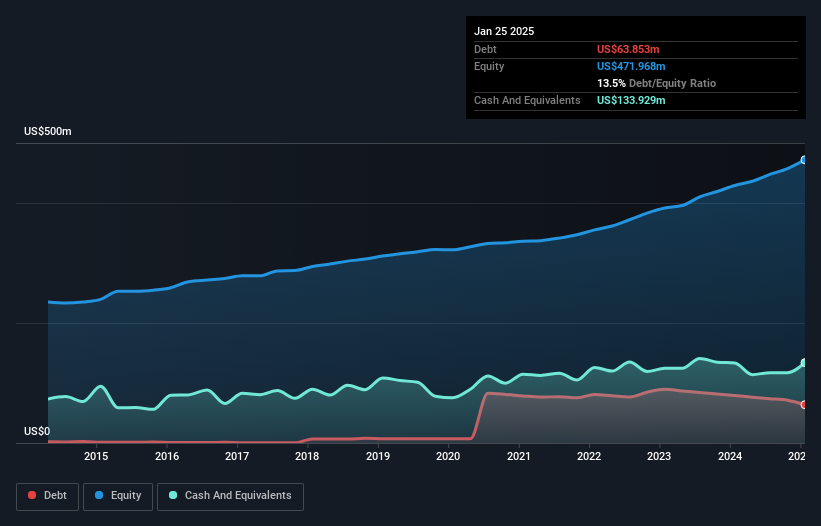

Northeast Bank, with total assets of US$4.9 billion and equity of US$536 million, offers an intriguing opportunity in the financial sector. Its net interest margin stands at 4.9%, supported by a sufficient allowance for bad loans at 0.8% of total loans, showcasing prudent risk management. The bank's earnings growth outpaced the industry at 27.2% versus 19.9%, reflecting strong performance relative to peers while trading at a significant discount to its estimated fair value by 57%. Despite challenges like rising competition and regulatory shifts, strategic moves in digital transformation could bolster future growth prospects significantly.

Village Super Market (VLGE.A)

Simply Wall St Value Rating: ★★★★★☆

Overview: Village Super Market, Inc. operates a chain of supermarkets in the United States and has a market cap of $616.78 million.

Operations: The company generates revenue primarily from the retail sale of food and nonfood products, totaling $2.39 billion.

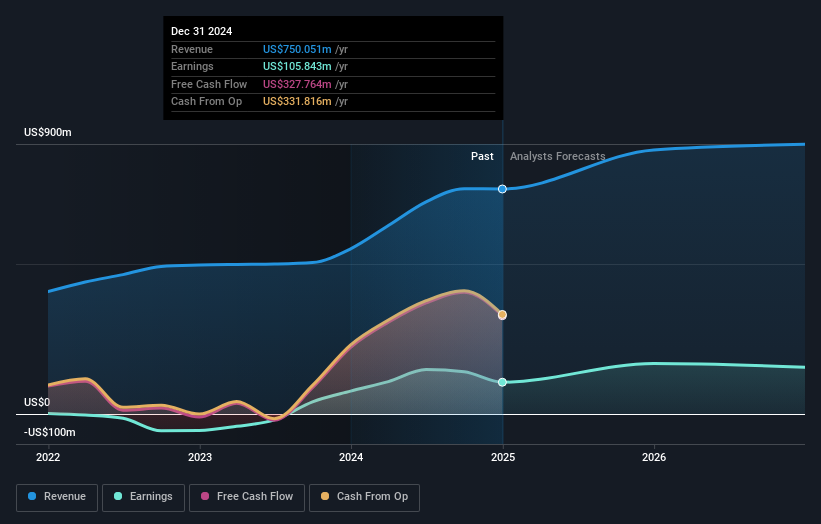

Village Super Market has been making strides in the retail sector, with earnings growing at an impressive 20.2% annually over the past five years. The company seems to be a bargain, trading at 50.8% below its estimated fair value, and it remains free cash flow positive. Despite facing industry challenges, Village's debt-to-equity ratio improved significantly from 23.3% to 11.6%, reflecting better financial health over time. Recent earnings reports show sales reaching US$640 million for Q2 and net income of US$17 million, indicating steady growth compared to last year’s figures of US$599 million in sales and US$16 million in net income.

- Click here to discover the nuances of Village Super Market with our detailed analytical health report.

Evaluate Village Super Market's historical performance by accessing our past performance report.

HCI Group (HCI)

Simply Wall St Value Rating: ★★★★★★

Overview: HCI Group, Inc. operates in the property and casualty insurance sector within the United States and has a market capitalization of approximately $1.96 billion.

Operations: The primary revenue stream for HCI Group comes from its insurance operations, generating approximately $834.43 million. Additional contributions include Exzeo at $221.28 million and reciprocal exchange operations at $65.55 million, while real estate contributes $14.82 million.

HCI Group, a tech-focused insurer, has made strides with its proprietary technology and disciplined underwriting. Over the past year, earnings surged by 171%, far outpacing the insurance industry’s 25.8% growth. The debt-to-equity ratio improved significantly from 89.6% to 6.1% over five years, indicating better financial health. Trading at about 78.7% below estimated fair value suggests potential upside for investors despite recent shareholder dilution and anticipated annual revenue growth of just under 9%. A share repurchase program worth $80 million could bolster stock value as HCI navigates risks like reinsurance costs and market dependencies.

Turning Ideas Into Actions

- Explore the 333 names from our US Undiscovered Gems With Strong Fundamentals screener here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com