- LIVE QUOTES

- LEARN

- HELP

EN

3 Undervalued Small Caps With Insider Action To Watch

Over the last 7 days, the United States market has experienced a 3.5% drop, yet it remains up by 14% over the past year with earnings forecasted to grow by 15% annually. In this fluctuating environment, identifying stocks that are potentially undervalued and have notable insider activity can be key to uncovering promising opportunities in the small-cap sector.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| PCB Bancorp | 8.7x | 2.9x | 27.24% | ★★★★★☆ |

| Financial Institutions | 8.3x | 2.6x | 45.79% | ★★★★★☆ |

| AVITA Medical | NA | 1.6x | 39.36% | ★★★★★☆ |

| Franklin Financial Services | 10.9x | 2.7x | 0.31% | ★★★★☆☆ |

| 1st Source | 10.6x | 4.0x | 49.57% | ★★★★☆☆ |

| New Peoples Bankshares | 9.4x | 2.2x | 41.37% | ★★★☆☆☆ |

| Union Bankshares | 10.1x | 2.1x | 20.85% | ★★★☆☆☆ |

| Bank of the James Financial Group | 10.4x | 1.9x | 47.94% | ★★★☆☆☆ |

| CEVA | NA | 4.4x | -2.33% | ★★★☆☆☆ |

| Douglas Emmett | 105.8x | 1.6x | 43.80% | ★★★☆☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

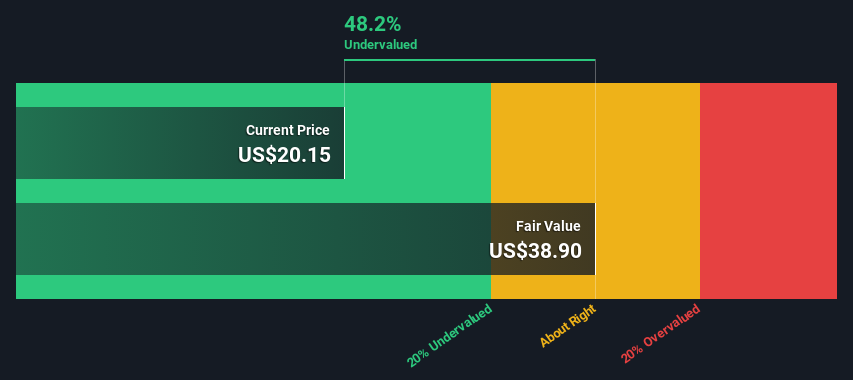

PCB Bancorp (PCB)

Simply Wall St Value Rating: ★★★★★☆

Overview: PCB Bancorp operates as a bank holding company, primarily providing commercial banking services to small and medium-sized businesses, professionals, and residents with a market capitalization of approximately $0.19 billion.

Operations: PCB Bancorp generates revenue primarily from its operations in the banking industry, with recent quarterly revenues reaching $111.69 million. The company's operating expenses have been a significant component of its cost structure, with general and administrative expenses accounting for a substantial portion, such as $50.83 million in the latest period. Notably, PCB Bancorp has consistently achieved a gross profit margin of 100% over multiple periods.

PE: 8.7x

PCB Bancorp, a small player in the financial sector, recently reported a strong performance with fourth-quarter net income rising to US$9.24 million from US$7.03 million the previous year. Insider confidence is evident as an insider purchased 18,200 shares for approximately US$390K. Additionally, the company completed a share repurchase of 500,474 shares for US$9.31 million by December 2025. With earnings projected to grow at nearly 8% annually and increased dividends, PCB offers potential growth opportunities in its niche market segment.

- Dive into the specifics of PCB Bancorp here with our thorough valuation report.

Assess PCB Bancorp's past performance with our detailed historical performance reports.

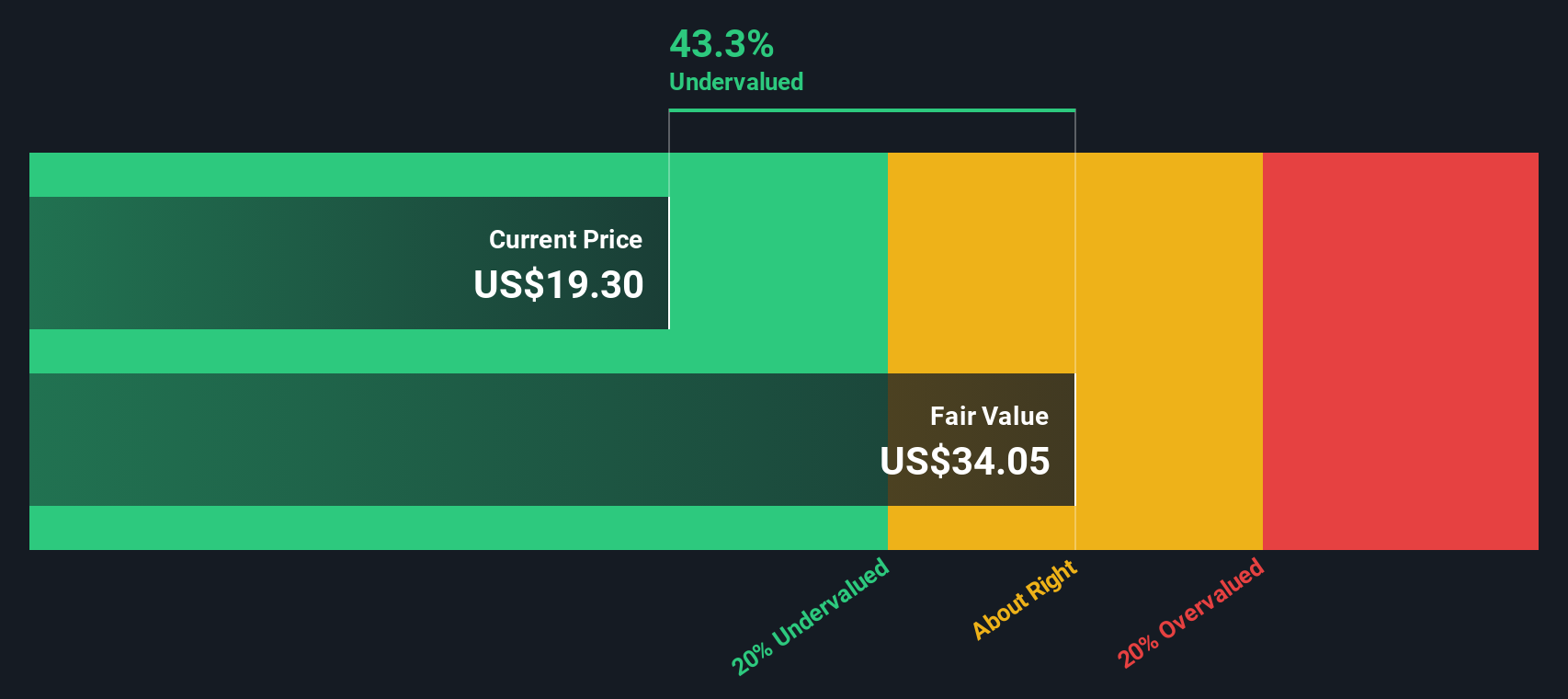

Amerant Bancorp (AMTB)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Amerant Bancorp operates as a bank holding company providing a range of banking products and services, with a market capitalization of approximately $0.92 billion.

Operations: The company's primary revenue stream is derived from its banking operations, generating $396.69 million in the most recent period. Operating expenses have shown fluctuations over time, with general and administrative expenses being a significant component, reaching $246.80 million in the latest quarter. The net income margin has experienced variability, reflecting changes in profitability over different periods.

PE: 16.6x

Amerant Bancorp, a smaller financial player in the U.S., showcases potential value with net income swinging to US$52.42 million from a prior loss, indicating improved profitability. Earnings per share rose to US$1.26 from a loss of US$0.44, reflecting operational efficiency gains. Despite grappling with high bad loans at 2.6% and low coverage at 46%, insider confidence is evident through share repurchases totaling US$45.49 million since late 2025, hinting at management's belief in the company's prospects amidst plans for further buybacks up to US$40 million by end-2026.

- Take a closer look at Amerant Bancorp's potential here in our valuation report.

Evaluate Amerant Bancorp's historical performance by accessing our past performance report.

GeoPark (GPRK)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: GeoPark is an oil and gas exploration and production company with a market cap of $0.55 billion.

Operations: GeoPark's revenue primarily stems from its Oil & Gas - Exploration & Production segment, generating $492.50 million. The company experienced fluctuations in its gross profit margin, peaking at 76.00% in Q3 2024 and dropping to a low of 60.31% in Q4 2015. Operating expenses have varied significantly over time, impacting overall profitability and net income margins, which reached a high of 22.35% in Q1 2023 and a low of -116.61% in Q2 2016.

PE: 10.1x

GeoPark, a smaller energy player in the U.S., recently saw insider confidence through share purchases, signaling potential value. Despite a dip in revenue to US$492.5 million for 2025 from US$660.8 million the previous year, net income rose to US$49.7 million from US$15.3 million due to strategic initiatives like a private placement raising over US$107 million and an extended offtake agreement with Vitol enhancing cash flow visibility. Looking ahead, earnings are expected to grow by nearly 20% annually, although challenges remain with funding risks and declining profit margins from 14.6% last year to 10.1%.

- Click to explore a detailed breakdown of our findings in GeoPark's valuation report.

Explore historical data to track GeoPark's performance over time in our Past section.

Seize The Opportunity

- Navigate through the entire inventory of 59 Undervalued US Small Caps With Insider Buying here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com