- LIVE QUOTES

- LEARN

- HELP

EN

Undiscovered Gems in the US Market to Explore This March 2026

Over the last 7 days, the United States market has experienced a 1.9% drop, yet it remains up by 15% over the past year with earnings projected to grow annually by the same percentage. In this dynamic environment, identifying stocks that are not only resilient but also positioned for growth can be crucial for investors seeking opportunities beyond well-trodden paths.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| First Bancorp | 68.18% | 1.28% | -2.88% | ★★★★★★ |

| Tri-County Financial Group | 70.32% | -2.03% | -13.70% | ★★★★★★ |

| Security Federal | 17.59% | 5.51% | 0.13% | ★★★★★★ |

| ASA Gold and Precious Metals | NA | 12.65% | 41.20% | ★★★★★★ |

| Oakworth Capital | 26.12% | 15.98% | 13.01% | ★★★★★★ |

| Affinity Bancshares | 42.51% | 1.82% | 1.11% | ★★★★★★ |

| Winchester Bancorp | 121.44% | 49.13% | 3283.33% | ★★★★★★ |

| Seneca Foods | 38.64% | 2.39% | -18.65% | ★★★★★☆ |

| NameSilo Technologies | 12.63% | 14.48% | 3.12% | ★★★★★☆ |

| Pure Cycle | 5.42% | 9.36% | -2.03% | ★★★★★☆ |

We're going to check out a few of the best picks from our screener tool.

Calavo Growers (CVGW)

Simply Wall St Value Rating: ★★★★★★

Overview: Calavo Growers, Inc. focuses on sourcing, packing, and distributing fresh produce like avocados and tomatoes, as well as processing guacamole for various retail and wholesale channels globally, with a market cap of $471.88 million.

Operations: Calavo Growers generates revenue primarily through its Fresh segment, contributing $541.44 million, and its Prepared segment, which adds $74.82 million. The company focuses on efficiently managing costs associated with sourcing and processing to optimize profitability across these segments.

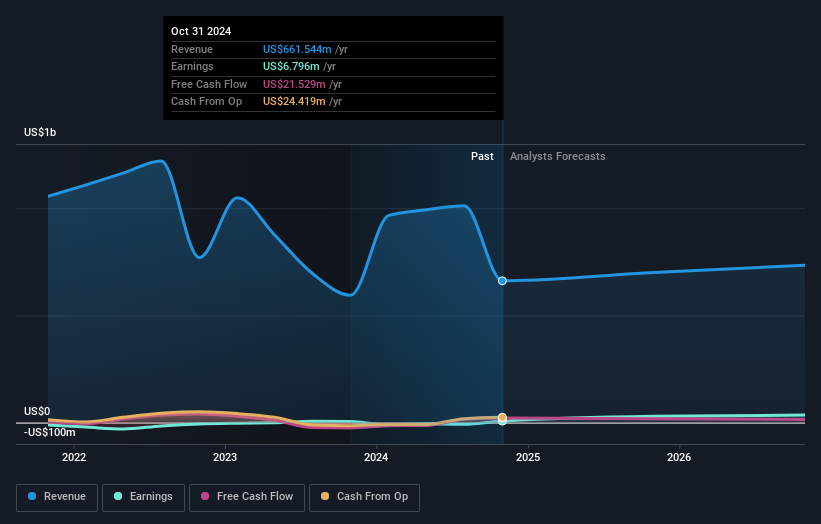

Calavo Growers, a notable player in the food industry, has been making waves with its earnings growth of 16.8% over the past year, outpacing the industry's -1.1%. Despite a significant one-off loss of US$6 million impacting recent financials, Calavo remains debt-free and is trading at 62.7% below estimated fair value. With earnings projected to grow by 29.46% annually and a solid free cash flow position, this company seems poised for potential upside despite recent challenges in sales and net income declines compared to last year’s figures.

- Click here and access our complete health analysis report to understand the dynamics of Calavo Growers.

Gain insights into Calavo Growers' past trends and performance with our Past report.

Natural Grocers by Vitamin Cottage (NGVC)

Simply Wall St Value Rating: ★★★★★☆

Overview: Natural Grocers by Vitamin Cottage, Inc. operates as a retailer of natural and organic groceries and dietary supplements in the United States, with a market capitalization of approximately $598.17 million.

Operations: NGVC generates revenue primarily through its natural and organic retail stores, amounting to $1.34 billion. The company's market capitalization stands at approximately $598.17 million.

Natural Grocers, a nimble player in the organic retail space, is making waves with its debt-free status and impressive 32.5% earnings growth over the past year, outpacing the industry average of 10.3%. Trading at 43.7% below its estimated fair value, it seems like a bargain for investors eyeing potential value plays. The company recently announced an exciting store relocation in Abilene and plans to expand further with new openings in Walla Walla and Lake Geneva this spring. These moves align with their commitment to community engagement and sustainable practices, potentially enhancing customer experience and market presence significantly.

Oil-Dri Corporation of America (ODC)

Simply Wall St Value Rating: ★★★★★☆

Overview: Oil-Dri Corporation of America, along with its subsidiaries, specializes in the development, manufacturing, and marketing of sorbent products both domestically and internationally, with a market cap of approximately $916.29 million.

Operations: Oil-Dri generates revenue primarily from two segments: Retail and Wholesale Products, contributing $301.91 million, and Business to Business Products, contributing $177.03 million. The company's market cap stands at approximately $916.29 million.

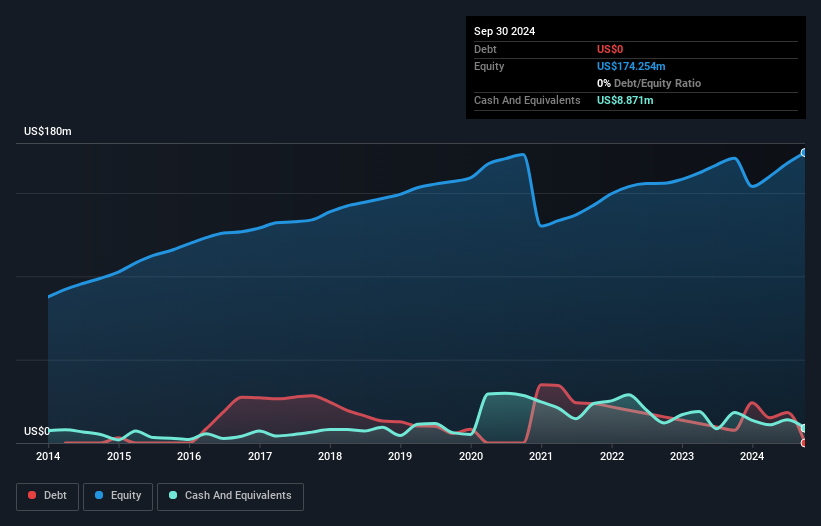

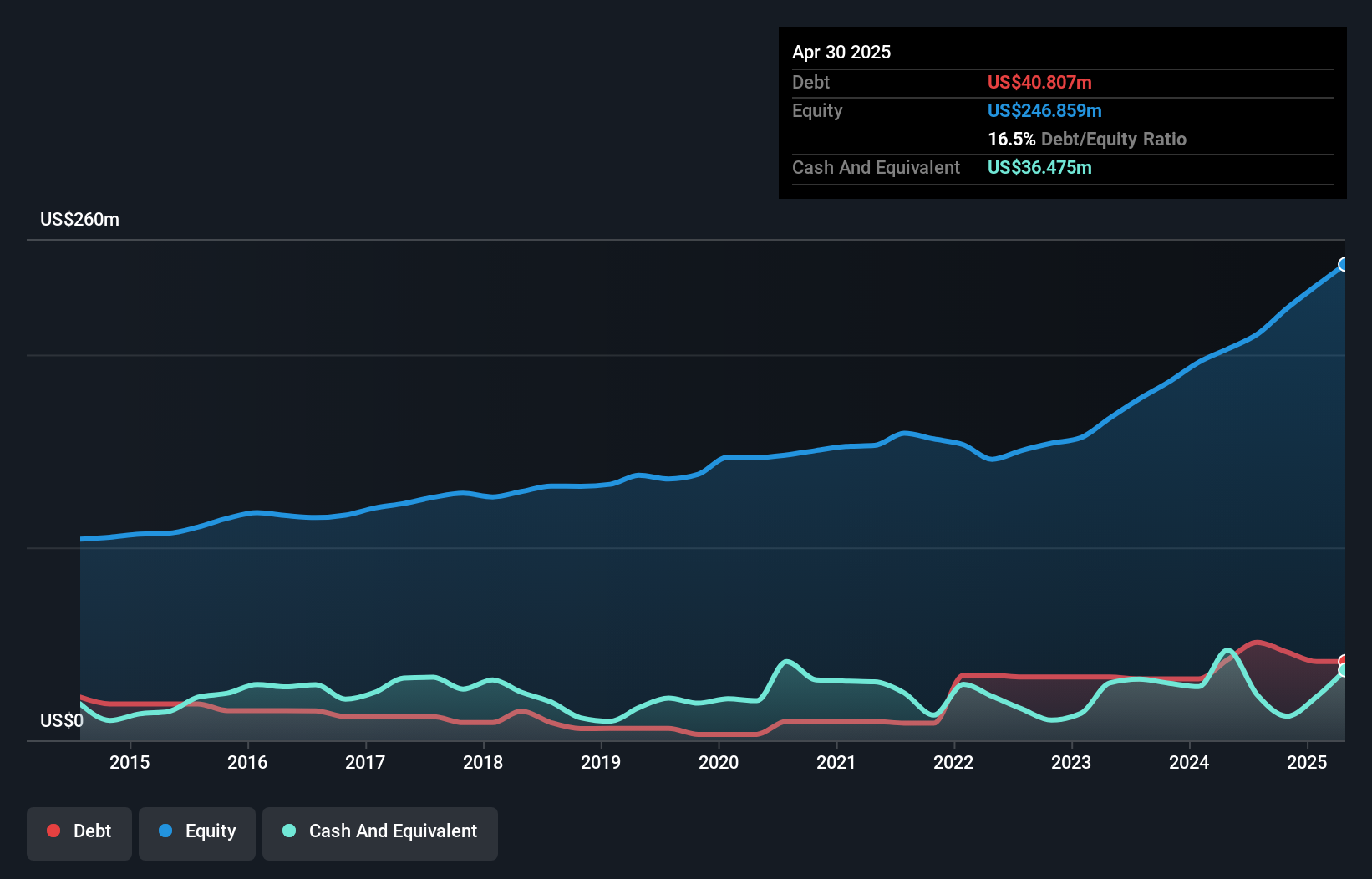

Oil-Dri Corporation of America, a nimble player in the household products sector, has demonstrated robust earnings growth of 16.1% over the past year, outpacing its industry peers. Trading at 26.1% below its estimated fair value, it offers an intriguing proposition for investors seeking undervalued opportunities. The company reported second-quarter sales of US$117.74 million with net income slightly down to US$12.57 million compared to last year's figures. Impressively, Oil-Dri's interest payments are well-covered by EBIT at a ratio of 59.7x, reflecting strong financial health despite an increased debt-to-equity ratio from 6.5% to 14.6%.

- Navigate through the intricacies of Oil-Dri Corporation of America with our comprehensive health report here.

Learn about Oil-Dri Corporation of America's historical performance.

Where To Now?

- Take a closer look at our US Undiscovered Gems With Strong Fundamentals list of 333 companies by clicking here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com