- LIVE QUOTES

- LEARN

- HELP

EN

Assessing Weyerhaeuser (WY) Valuation As Analyst Fair Value Signals A 25% Undervaluation

What stands out about Weyerhaeuser right now

Weyerhaeuser (WY) continues to trade with recent returns that differ meaningfully across time frames, with a positive move over the past week but negative performance over the past month and past 3 months.

See our latest analysis for Weyerhaeuser.

At a share price of $23.86, Weyerhaeuser sits roughly flat year to date, with a modest 7 day share price return of 3.02%. However, its 1 year total shareholder return decline of 15.67% points to fading longer term momentum and an ongoing reassessment of risk and income prospects.

If you want to see where else investors are finding opportunity in income and real assets, it can be useful to compare Weyerhaeuser with other companies via a discovery focused screener such as 20 top founder-led companies

With Weyerhaeuser trading at $23.86 and sitting at an estimated 19% discount to its US$31.82 analyst price target, plus an indicated intrinsic discount, you have to ask: is this a genuine value opportunity, or is the market already pricing in future growth?

Most Popular Narrative: 25% Undervalued

Weyerhaeuser’s most followed narrative pegs fair value at $31.82, comfortably above the last close at $23.86, and builds that gap on detailed operating and earnings assumptions.

The carbon capture and sequestration (CCS) agreement with Occidental Petroleum represents a growth opportunity in Weyerhaeuser's Natural Climate Solutions business, likely boosting future earnings.

Ongoing construction of the EWP facility in Arkansas and return to normal operations at the Montana facility will drive increased production, positively impacting revenue and net margins.

Want to see what is powering that valuation gap? The narrative leans heavily on faster earnings growth, higher margins and a richer P/E in a few years. The exact mix of those inputs might surprise you.

Result: Fair Value of $31.82 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on housing demand and lumber pricing holding up, because weaker construction activity or trade headwinds on logs could quickly challenge that upside story.

Find out about the key risks to this Weyerhaeuser narrative.

Another Angle On Valuation

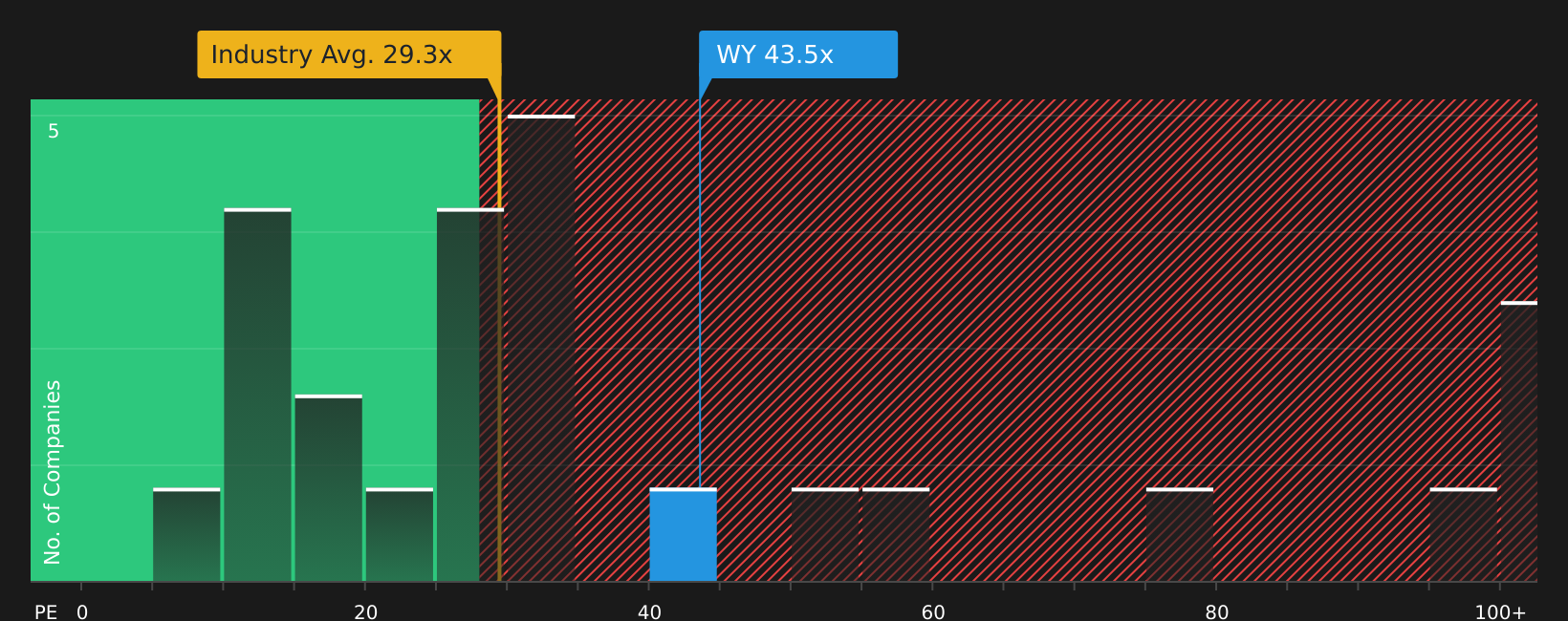

The main narrative leans on analyst targets and earnings projections, but the current P/E of 53.1x is well above both peers at 25.3x and the sector at 26.2x, and even sits above a fair ratio of 45.4x. That premium could signal quality, or just add valuation risk, so which do you think it is.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With mixed signals on value, risk and income throughout this article, it makes sense to review the underlying data yourself and move quickly to form your own take. To help frame that view, weigh up the 3 key rewards and 3 important warning signs

Looking for more investment ideas?

Now that you have a clearer view on Weyerhaeuser, you can broaden your watchlist with focused ideas that match your investing style.

- Target potential mispricing by reviewing companies flagged as 62 high quality undervalued stocks and see which ones deserve a closer look.

- Strengthen your income stream by scanning for reliable payers in the 12 dividend fortresses and see how they stack up on yield and stability.

- Prioritise resilience by focusing on financially robust names in the solid balance sheet and fundamentals stocks screener (39 results) and avoid businesses that look fragile on the numbers.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com