- LIVE QUOTES

- LEARN

- HELP

EN

Will Credit Acceptance’s New CBO Hire Reframe Its Analytics‑Driven Strategy Story for Investors (CACC)?

- Credit Acceptance Corporation recently appointed former Deutsche Telekom and T-Mobile executive Steffen Schumann as its Chief Business Officer, reporting to CEO Vinayak Hegde, with responsibilities spanning enterprise business planning, pricing strategy, advanced analytics, and dealer scorecarding.

- The hire underscores Credit Acceptance’s effort to tighten execution and translate analytics-driven insights into actions, at a time when management is seeing early signs of operational stability and steady forecasted collection rates.

- Next, we’ll examine how Schumann’s focus on pricing strategy and advanced analytics could influence Credit Acceptance’s existing investment narrative.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 25 best rare earth metal stocks of the very few that mine this essential strategic resource.

Credit Acceptance Investment Narrative Recap

To own Credit Acceptance, you need to be comfortable with a subprime auto lender that depends on accurate credit forecasting and disciplined pricing to protect margins. Schumann’s appointment looks supportive of the near term catalyst around stabilizing collections and loan performance, but it does not, by itself, remove the key risk that recent loan vintages could still underperform and pressure earnings.

The most relevant recent announcement here is management’s comment that forecasted collection rates were stable over the two months ended 28 February 2026, which helps frame Schumann’s mandate. If his work on pricing, unit economics, and dealer scorecards helps the company maintain or refine these forecasts, it could become an important input into how investors think about Credit Acceptance’s ability to manage through competitive and credit pressures.

But while collection forecasts look steadier for now, investors still need to be aware that...

Read the full narrative on Credit Acceptance (it's free!)

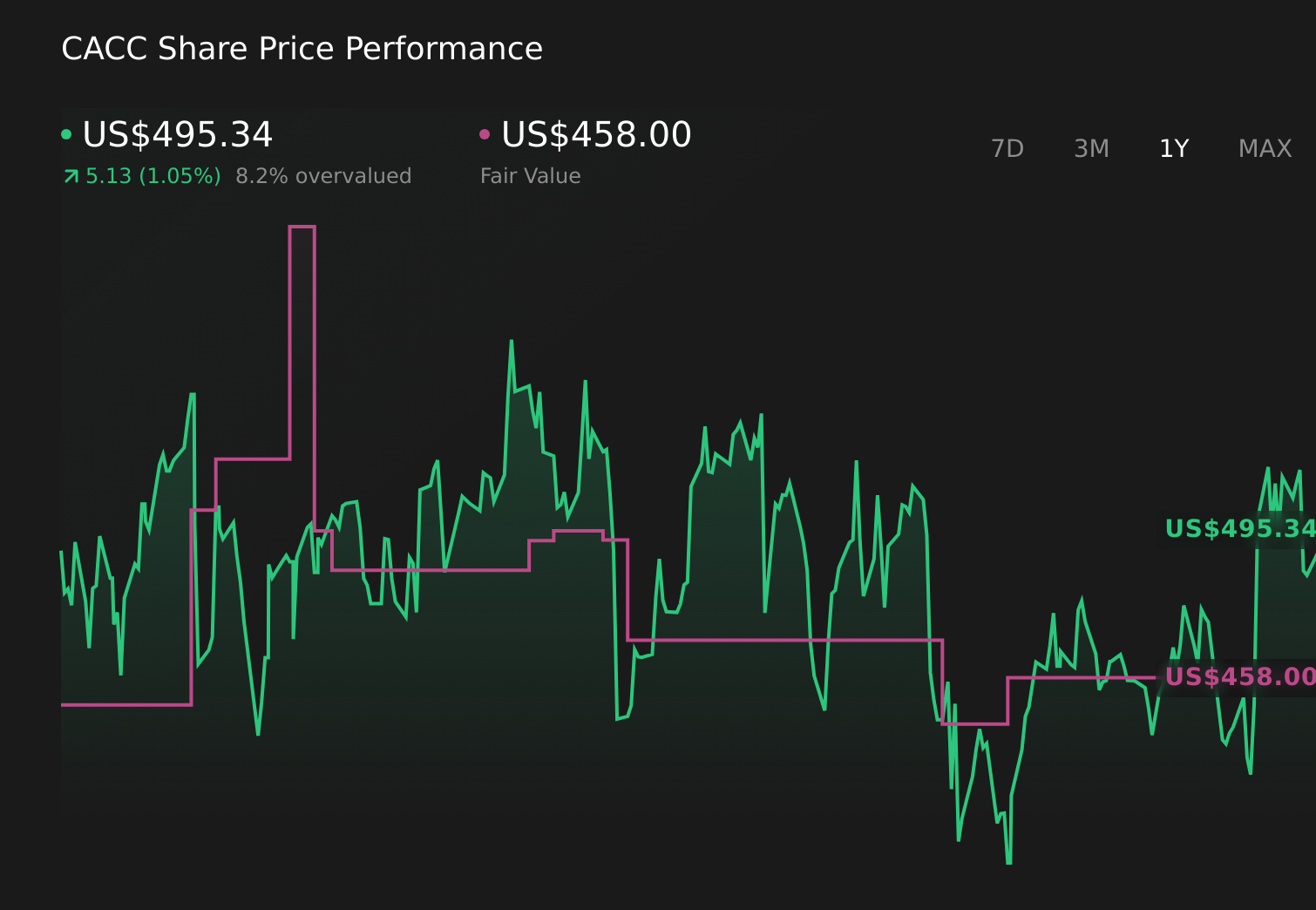

Credit Acceptance's narrative projects $4.5 billion revenue and $504.0 million earnings by 2028. This requires 56.2% yearly revenue growth and about an $80 million earnings increase from $424.4 million today.

Uncover how Credit Acceptance's forecasts yield a $458.00 fair value, a 9% upside to its current price.

Exploring Other Perspectives

Two Simply Wall St Community fair value estimates for Credit Acceptance range from US$300.34 to US$458, underscoring how far apart individual views can be. When you set those against the risk that 2022 to 2024 loan vintages could still see weaker net cash flows, it becomes clear why many investors seek out multiple perspectives before forming a view on the company’s resilience.

Explore 2 other fair value estimates on Credit Acceptance - why the stock might be worth 28% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Credit Acceptance research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Credit Acceptance research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Credit Acceptance's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- Explore 22 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com