- LIVE QUOTES

- LEARN

- HELP

EN

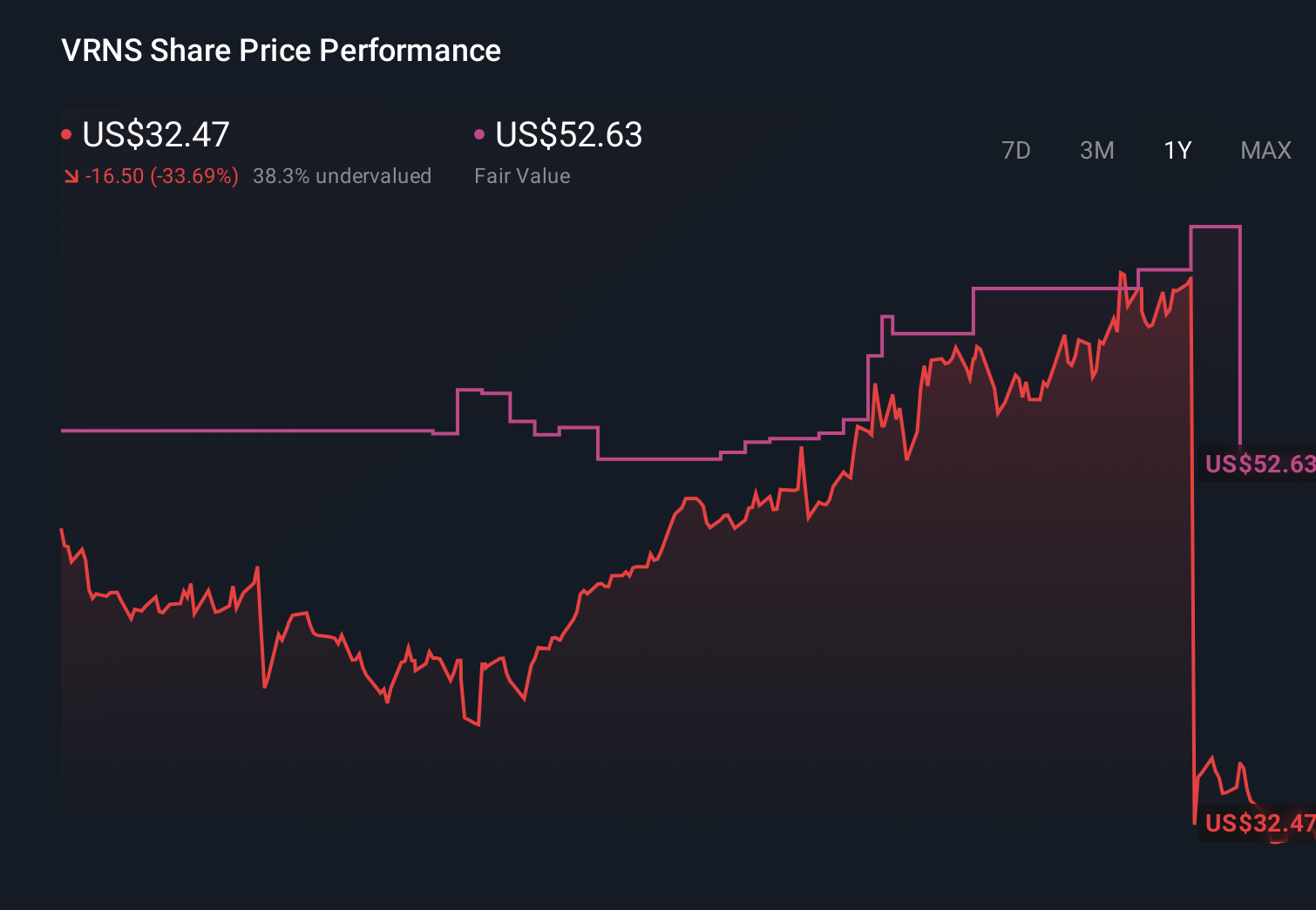

Varonis Systems (VRNS) Is Down 10.6% After Exiting On-Premise Business To Focus On AI SaaS

- Earlier this month, Varonis Systems unexpectedly announced it will discontinue its on-premises solution, which contributed about 15% of revenue, after missing quarterly projections and shifting its focus more fully to its SaaS platform.

- At the same time, the company launched its new Varonis Atlas AI security platform and prepared high-profile presentations at RSA Conference 2026, underscoring a quicker pivot toward AI-driven, cloud-based data security.

- We’ll now examine how the accelerated exit from on-premises products may reshape Varonis Systems’ existing SaaS-focused investment narrative.

AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Varonis Systems Investment Narrative Recap

To own Varonis today, you need to believe its SaaS and AI platforms can offset a challenging exit from on‑premises products while the company remains unprofitable and coping with margin pressure and dilution. The surprise decision to discontinue on‑prem offerings removes roughly 15% of revenue and could intensify short term earnings volatility, but it also simplifies the story around SaaS ARR as the main near term catalyst and heightens the risk that churn or slower migrations weigh on growth.

Among the recent announcements, Varonis Atlas stands out as most relevant here. As the firm accelerates away from self‑hosted products, Atlas positions Varonis more squarely in AI centric, cloud based data and AI security, which ties directly into its SaaS ARR growth goals. How effectively Atlas converts free trials into paid, recurring contracts will be an important data point for investors watching whether this sharper SaaS focus can offset the on‑premises revenue loss.

Yet beneath the AI and SaaS story, investors should also be aware that ongoing weakness in legacy on‑premises renewals could...

Read the full narrative on Varonis Systems (it's free!)

Varonis Systems’ narrative projects $992.3 million revenue and $113.1 million earnings by 2029. This requires 16.8% yearly revenue growth and a $242.4 million earnings increase from -$129.3 million today.

Uncover how Varonis Systems' forecasts yield a $33.90 fair value, a 60% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming about US$1.0 billion of revenue and US$125.8 million of earnings by 2028, but the surprise end of self hosted solutions and risk of permanent churn show how different your view might be if you focus on those upside targets versus the possibility that both bullish and baseline narratives will need to be revisited after this news.

Explore 3 other fair value estimates on Varonis Systems - why the stock might be worth over 3x more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Varonis Systems research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Varonis Systems research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Varonis Systems' overall financial health at a glance.

Searching For A Fresh Perspective?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Uncover the next big thing with 30 elite penny stocks that balance risk and reward.

- Explore 22 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Find 61 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com