- LIVE QUOTES

- LEARN

- HELP

EN

Discovering US Undiscovered Gems In March 2026

Over the last 7 days, the United States market has experienced a slight dip of 1.6%, yet it remains robust with a 15% increase over the past year and anticipated earnings growth of 16% per annum in the coming years. In this dynamic environment, identifying stocks that are undervalued or overlooked can provide unique opportunities for investors seeking to capitalize on emerging potential within a thriving market.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Tri-County Financial Group | 70.32% | -2.03% | -13.70% | ★★★★★★ |

| Cashmere Valley Bank | 31.17% | 5.25% | 1.74% | ★★★★★★ |

| ASA Gold and Precious Metals | NA | 12.65% | 41.20% | ★★★★★★ |

| Sound Financial Bancorp | 16.27% | 0.75% | -13.28% | ★★★★★★ |

| First Northern Community Bancorp | NA | 7.53% | 11.34% | ★★★★★★ |

| Winchester Bancorp | 121.44% | 49.13% | 3283.33% | ★★★★★★ |

| Union Bankshares | 374.44% | 1.11% | -7.71% | ★★★★★☆ |

| NameSilo Technologies | 12.63% | 14.48% | 3.12% | ★★★★★☆ |

| Pure Cycle | 5.42% | 9.36% | -2.03% | ★★★★★☆ |

| Oxford Bank | 12.42% | 14.34% | 4.14% | ★★★★☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

TSS (TSSI)

Simply Wall St Value Rating: ★★★★★★

Overview: TSS, Inc. focuses on the planning, design, deployment, maintenance, and refresh of end-user and enterprise systems in the United States with a market capitalization of $370.50 million.

Operations: TSS, Inc.'s revenue streams primarily comprise Procurement ($197.48 million), System Integration ($40.34 million), and Facilities Management ($7.91 million).

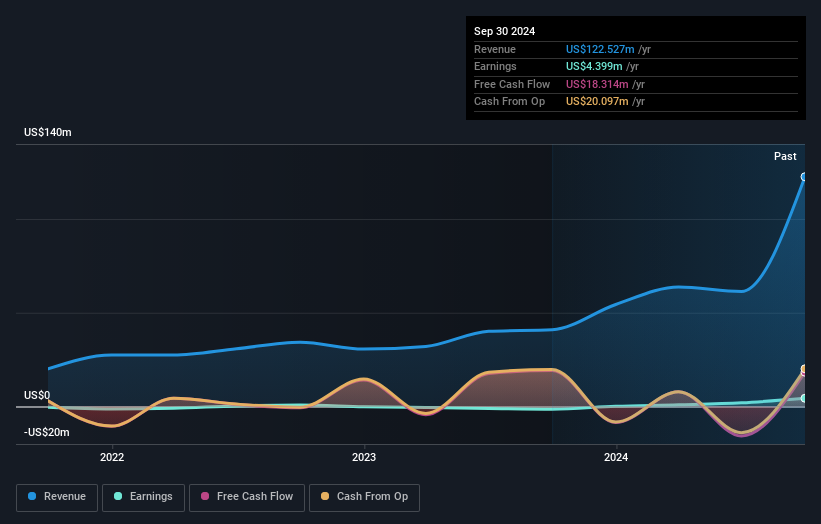

TSS, Inc. has shown impressive growth with earnings increasing by 153% over the past year, outpacing the IT industry's 32%. The company's debt to equity ratio improved significantly from 70.2% to 23.5% over five years, indicating stronger financial health. Despite a volatile share price recently, TSS remains profitable and free cash flow positive with US$19.18 million in levered free cash flow as of September 2023. However, recent significant insider selling could be a concern for some investors. Future earnings are expected to decline by an average of 25% annually over the next three years, suggesting potential challenges ahead.

- Click here and access our complete health analysis report to understand the dynamics of TSS.

Gain insights into TSS' past trends and performance with our Past report.

Ingles Markets (IMKT.A)

Simply Wall St Value Rating: ★★★★★★

Overview: Ingles Markets, Incorporated operates a chain of supermarkets in the United States and has a market capitalization of approximately $1.64 billion.

Operations: The company's primary revenue stream is its retail segment, generating approximately $5.20 billion.

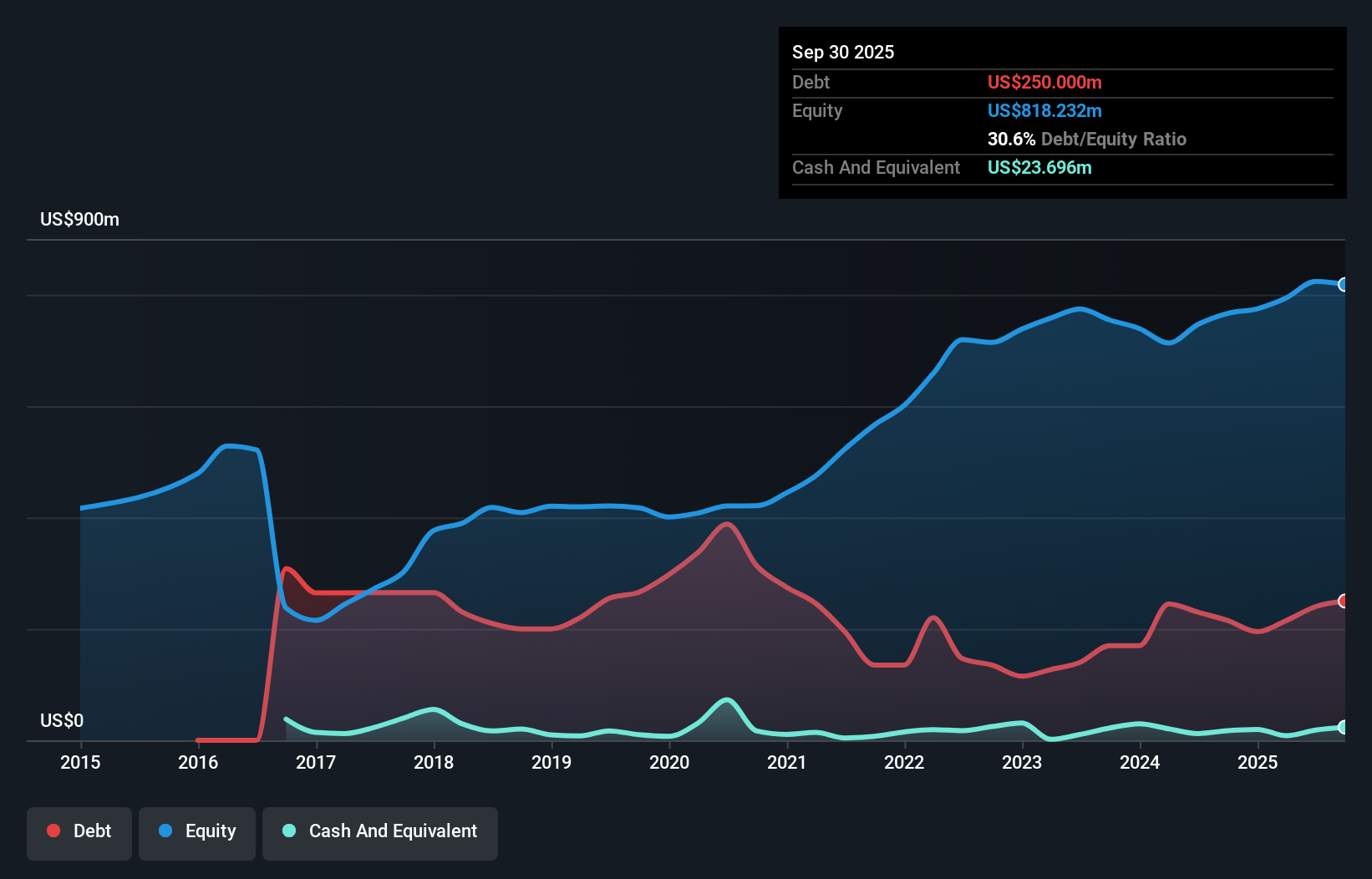

Ingles Markets, with its robust earnings growth of 20.4% over the past year, has outpaced the Consumer Retailing industry average of 10.3%. The company appears undervalued, trading at 40.7% below its estimated fair value, and has improved its financial health by reducing its debt to equity ratio from 67.5% to 31.2% over five years. Despite a historical annual decline in earnings of 22.4%, Ingles remains profitable with high-quality earnings and well-covered interest payments at a coverage ratio of 7.4x EBIT, indicating solid operational efficiency and financial management in this niche market space.

- Unlock comprehensive insights into our analysis of Ingles Markets stock in this health report.

Review our historical performance report to gain insights into Ingles Markets''s past performance.

AdvanSix (ASIX)

Simply Wall St Value Rating: ★★★★★☆

Overview: AdvanSix Inc. is an integrated chemistry company that manufactures and sells polymer resins both in the United States and internationally, with a market capitalization of approximately $629.90 million.

Operations: AdvanSix generates revenue primarily from its chemical manufacturing segment, which brought in $1.52 billion. The company's financial performance is significantly influenced by this core segment's operations and market dynamics.

AdvanSix, a small yet promising player in the chemicals sector, has shown resilience with earnings growth of 11.6% over the past year, outpacing the industry's -2.5%. Its debt to equity ratio improved significantly from 61.9% to 26.4% over five years, indicating prudent financial management. The company recently reported a net income of US$49.29 million for 2025, up from US$44.15 million in 2024, alongside basic earnings per share rising to US$1.83 from US$1.65 previously. Despite these gains and trading at an attractive value relative to peers, challenges like rising costs and market competition remain pertinent concerns for investors considering this stock's potential trajectory amidst evolving market conditions.

Seize The Opportunity

- Access the full spectrum of 327 US Undiscovered Gems With Strong Fundamentals by clicking on this link.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com