- LIVE QUOTES

- LEARN

- HELP

EN

Micron Stock: Did the AI Memory Leader Just Peak?

Key Points

Micron has fallen more than 20% since it reported a strong second-quarter earnings report last week.

Google said a new algorithm could significantly reduce the need for AI storage.

In past memory cycles, Micron stock has peaked shortly before its profits topped out.

Micron (NASDAQ: MU) investors were dealt a cold reality check last week. After the memory chipmaker delivered a smashing earnings report, the stock fell, and it's been sliding ever since.

A combination of doubts about the sustainability of the memory boom, malaise around the war in Iran, and a new threat to memory chips from Alphabet has led to a 23% sell-off, and the stock has fallen every day since the earnings report.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

On Thursday, Micron and its memory peers slipped in response to new research from Google on an algorithm that could make AI storage more efficient, thereby requiring less memory. TurboQuant, as the company calls the technology, could enable "massive compression for large language models and vector search engines."

While the implications of TurboQuant aren't fully clear, it underscores another risk to Micron and the memory sector, as new technology could alleviate the memory bottleneck.

However, most of Micron's pullback seems to be because of its sudden rise in the last year, and because the memory sector is notorious for being cyclical, prone to large booms and busts.

Ordinarily, a company that just tripled its revenue and grew net income by nearly 10x would be soaring, but Micron stock has already grown to become one of the most valuable companies in the world with a market cap that topped $500 billion before the post-earnings slide, so investors may think it's already run high enough.

So has Micron already peaked? Let's take a look back at what past memory cycles say.

Image source: Getty Images.

What Micron's history tells us

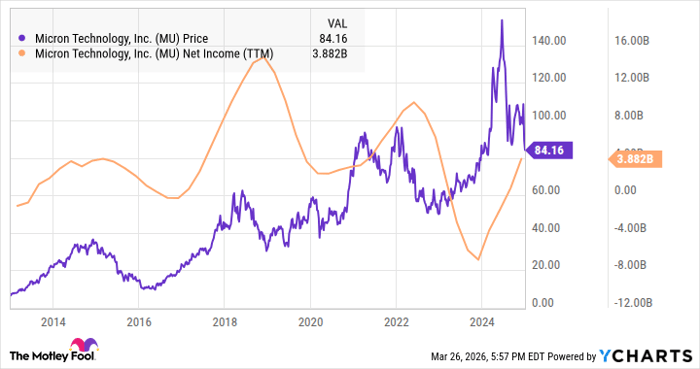

Micron's stock has historically moved in cycles as the memory sector experiences price swings due to inventory fluctuating between shortages and gluts. As recently as 2022, the company was losing more than $1 billion a year, and it just made nearly $14 billion in profit in a single quarter.

Stocks are forward-looking, so it makes sense that Micron stock would fall before the earnings cycle peaks. We don't know when that will be, of course, and management has suggested that supply would be tight through 2028. Micron's third-quarter guidance also called for even stronger results than the second quarter, seeing revenue reaching $33.5 billion, up from $23.9 billion in the second quarter, and adjusted earnings per share of around $19.15, which compares to $12.20 in the second quarter. That's a sign there's plenty of runway left for growth.

Prior to the AI boom, Micron has essentially had three stock peaks since 2014. As you can see from the chart below, each time the stock peaked, a peak in net income followed shortly after.

Historically, the stock has peaked because investors saw that profits were about to plateau. That was the case in 2014-15, 2018, and 2022 when the stock made a double peak.

Is this time different?

The AI supercycle is big enough that it has some important differences from previous cycles. Investors still don't know when AI semiconductor demand will top out, and it could still be years away. Nvidia just said it would generate $1 trillion in total revenue over the next two years, and the AI chip leader has recently seen its revenue growth accelerate.

What is clear is that Micron's profits look set to grow over the next several quarters, based on the company's own guidance, commentary from management about supply constraints, and Wall Street expectations as analysts see profits soaring through fiscal 2027. In fact, based on the analyst consensus of $58 in earnings per share this year, Micron now trades at a forward price-to-earnings ratio of just 6.

Using the chart above as a guide, it looks like Micron's peak is still to come. The company likely has several more quarters of profit growth in front of it before the cycle peaks.

While the nearly 25% sell-off since the earnings report may be scary, volatility is part of the memory sector. If profits continue to grow, Micron stock should rebound.

Jeremy Bowman has positions in Micron Technology and Nvidia. The Motley Fool has positions in and recommends Alphabet, Micron Technology, and Nvidia. The Motley Fool has a disclosure policy.