- LIVE QUOTES

- LEARN

- HELP

EN

Alphabet and Amazon Are Quietly Winning the Artificial Intelligence (AI) Race While Microsoft Stumbles. Should You Buy Either Stock Right Now?

Key Points

Microsoft has fallen so far, it's in bear market territory this year.

Amazon and Alphabet are doing better at keeping up with the market.

The three are collectively spending hundreds of billions of dollars on AI infrastructure this year.

This hasn't been a great year for artificial intelligence (AI) stocks. While I'm still confident that AI is a solid long-term play, it appears many AI stocks will finish the first quarter in the red for 2026. The tech-heavy Nasdaq Composite is down nearly 7% so far this year.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

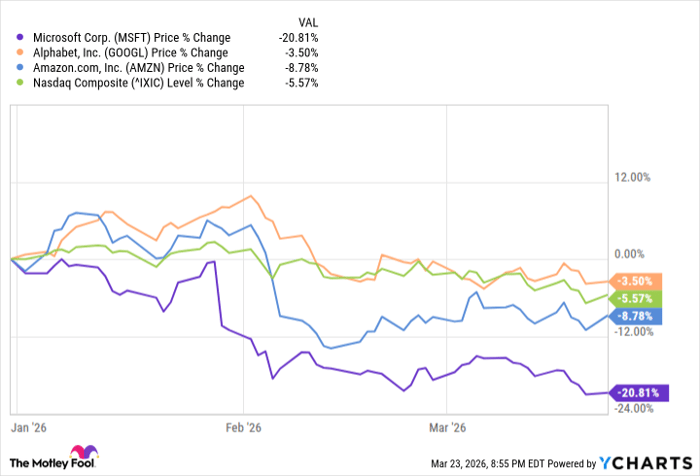

When you consider the top cloud computing companies, Microsoft (NASDAQ: MSFT) is notably in bear market territory with a loss of more than 21% this year, while Amazon (NASDAQ: AMZN) and Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL) are doing a better job of keeping up with the overall market.

What's the reason behind Microsoft's bigger-than-expected decline? And does this weakness mean that either Alphabet or Amazon is a better choice right now?

The challenges with Microsoft

The biggest reason Microsoft stock is sinking is the fear that overall spending on artificial intelligence (AI) will not yield a return on the its ambitious plans to build out its AI infrastructure. The company spent $37.5 billion in capital expenditures in the second quarter of fiscal 2026, up 65% from a year ago.

While the company saw a 10x increase in daily active users of Microsoft 365 Copilot, its AI digital assistant, total paid seats were only 15 million, versus 450 million in paid 365 commercial seats. It raises the question of whether Microsoft will be able to successfully recoup its investment in AI.

Microsoft also operates Azure, its leading cloud computing environment, which has 21% of the market, behind only Amazon Web Services, with 28%. (Google Cloud trails with 14%, giving the three top companies more than 60% of the cloud computing market.)

Microsoft reported that its Azure revenue was up 39% in the second quarter from a year ago, and overall cloud revenue was up 26% to $51.5 billion. Microsoft reported that its cloud remaining performance obligations increased 110% in the last year to $625 billion -- signaling that the company has a steep runway for future growth.

Image source: Getty Images.

Are Alphabet or Amazon better buys?

To be clear, Microsoft is far from alone in its AI spending ambitions. Alphabet, Amazon, Microsoft, and Meta Platforms are projected to spend as much as $650 billion on AI infrastructure this year alone. Amazon is expected to be the biggest spender, pumping $200 billion into its capital-expenditure budget -- a rate of spending that analysts say will result in negative free cash flow of $17 billion to $28 billion.

Alphabet is expected to spend $185 billion this year, which could see its free cash flow drop from $73.3 billion in 2025 to $8.2 billion this year. Microsoft is spending an estimated $145 billion.

If you agree with the narrative that the major AI companies are at risk of not seeing a return on their AI investments, then it's also important to look at the companies themselves -- because all three of them do more than just AI. Microsoft's suite of applications, through its Microsoft 365 product, includes Word, Excel, PowerPoint, and Outlook, all of which are critical for business operations. It also owns the LinkedIn social media platform, giving it an even greater position in offices nearly everywhere.

Then there's Amazon, which also runs the largest e-commerce site in the U.S. Amazon.com generated $588.19 billion in revenue in 2025, up 10.9% from 2024.

But the knock against Amazon is that e-commerce has low profit margins. The unit had operating income of $34.36 billion, meaning that its profit margin was a low 5.8%. AWS has a much better profit margin, with operating income of $45.6 billion on sales of $128.72 in 2025. That's a much more appealing margin of 35%.

Alphabet has a core business, too, as it's arguably the most dominant internet company in the world. Its Chrome browser and Google search engine have the biggest market shares in their respective businesses, by far. Alphabet received $82.28 billion in revenue from what it calls Google Services, which includes Google Search, YouTube ads, Google advertising and subscriptions. Plus, its operating income of $40.13 billion from Google Services results in a powerful profit margin of 48.7%.

What's the call here?

I like all three companies as long-term plays, and all are compelling buys on the dip. But if I had to choose one name in this grouping, Alphabet stock would be the clear pick. The company's advertising business is a powerful engine with a high profit margin. This, in my view, makes Alphabet less vulnerable to analysts' concerns over AI overspending.

Patrick Sanders has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, and Microsoft. The Motley Fool has a disclosure policy.