- LIVE QUOTES

- LEARN

- HELP

EN

A Look At Ultra Clean Holdings (UCTT) Valuation As AI Demand Outpaces Supply Constraints

AI driven demand in focus after analyst meeting

A recent analyst meeting with Ultra Clean Holdings (UCTT) executives highlighted that AI related wafer fabrication demand is holding up, with company leaders pointing to supply and execution bottlenecks rather than weak end demand as key constraints.

See our latest analysis for Ultra Clean Holdings.

Ultra Clean Holdings' share price has moved sharply higher alongside AI related demand, with a 1 day share price return of 6.79% at US$65.27, a 90 day share price return of 149.31%, and a 1 year total shareholder return of 166.30%. This suggests strong momentum rather than fading interest.

If AI equipment suppliers like Ultra Clean are on your radar, it can be helpful to see what else is moving in the space by checking out 35 AI infrastructure stocks

With Ultra Clean’s share price already up sharply and analyst targets sitting above the current level, the real question for you is whether recent AI optimism still leaves room for upside or if markets are already pricing in future growth.

Most Popular Narrative: 19.7% Undervalued

The most followed narrative puts Ultra Clean Holdings' fair value at $81.25 versus the last close of $65.27. This frames a gap that hinges on execution of its long term plan.

Ongoing organizational flattening, cost reduction initiatives, and factory or site consolidation are producing tangible decreases in OpEx, with further improvements expected by Q4, providing sustainable margin enhancement as industry volumes recover. Progress in vertical integration, particularly the Fluid Solutions business unit, along with deployment of company wide SAP systems, is set to improve operational efficiency and streamline customer engagement, driving higher margin mix and improved earnings beginning in early 2026.

Want to understand what has to go right for that valuation gap to close? The narrative leans on faster revenue growth, margin repair, and a richer profit multiple that is far from conservative. Curious which assumptions have the biggest impact on that $81.25 figure and how sensitive the outcome is to small changes in earnings power? The full breakdown lays those moving parts bare.

Result: Fair Value of $81.25 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on AI and memory spending staying supportive and on Ultra Clean avoiding extended demand weakness or customer concentration shocks that disrupt the UCT 3.0 plan.

Find out about the key risks to this Ultra Clean Holdings narrative.

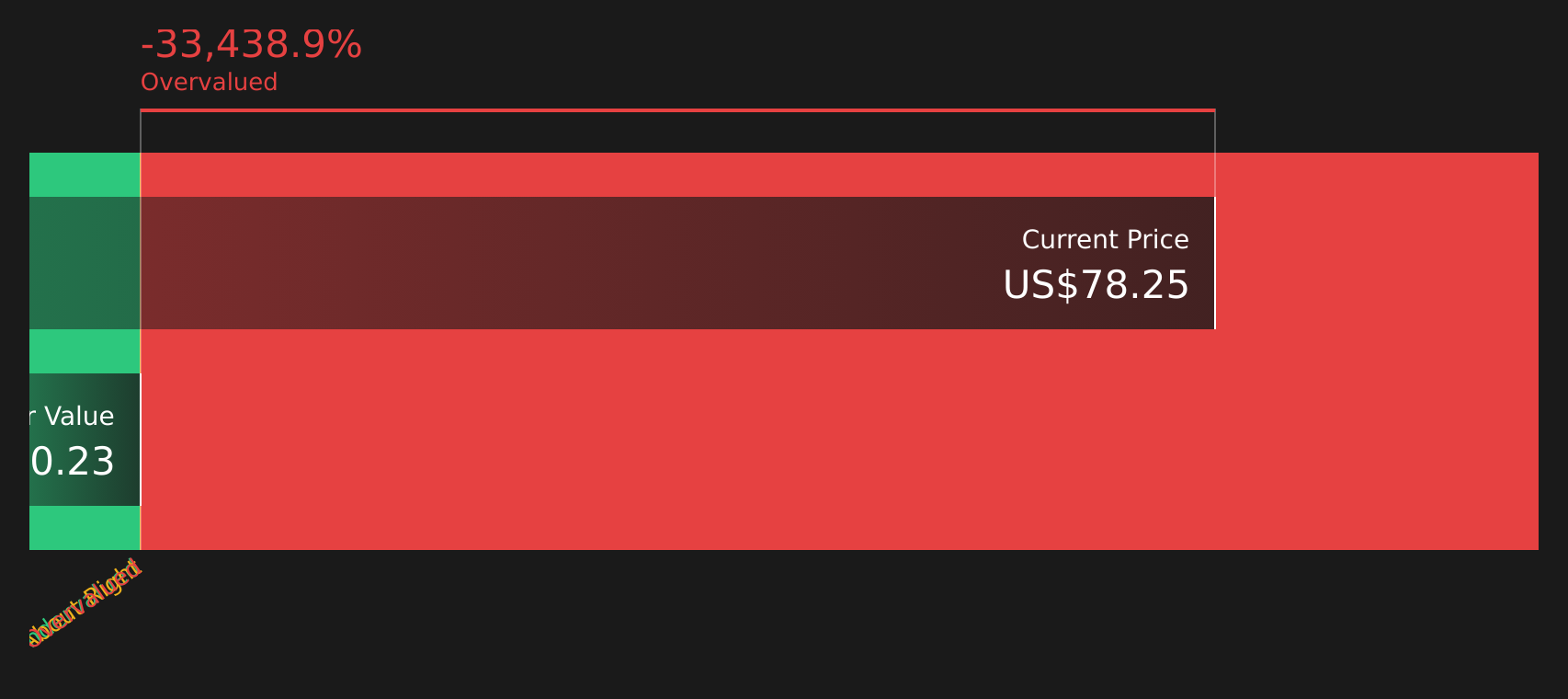

Another View: Cash Flows Paint A Harsher Picture

While the narrative and analyst targets point to a fair value of $81.25 and an undervalued share price, the Simply Wall St DCF model tells a very different story. On that framework, Ultra Clean trades well above an estimated future cash flow value of just $0.23, which implies very limited support from current cash flow assumptions.

If you want to see how this big gap between price and cash flow value is built up line by line, it is worth looking at how the SWS DCF model treats Ultra Clean’s forecasts and discount rate in more detail, starting with Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Ultra Clean Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 58 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With such a mixed picture on value and cash flows, it helps to move quickly, review the underlying data yourself and decide what feels reasonable. To weigh the potential upside against the concerns that other investors are focused on, check out the 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If you stop at just one company, you could miss opportunities that suit your goals better, so use the screener to compare and pressure test fresh ideas.

- Target resilient cash generators and stress test your watchlist against 58 high quality undervalued stocks that pair quality with pricing that may interest value focused investors.

- Prioritize staying power by scanning solid balance sheet and fundamentals stocks screener (39 results) to see which companies line up with your comfort level on debt and financial strength.

- Hunt for under followed stories before the crowd notices by checking the screener containing 25 high quality undiscovered gems that match your preferred fundamentals and risk profile.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com