- LIVE QUOTES

- LEARN

- HELP

EN

Nautilus Biotechnology And 2 Other Compelling Penny Stocks For Your Watchlist

Over the last 7 days, the U.S. market has dropped by 2.3%, though it has shown a robust increase of 13% over the past year, with earnings projected to grow by 16% annually in the coming years. In such fluctuating conditions, identifying stocks with strong fundamentals and solid balance sheets can be crucial for investors seeking growth opportunities at lower price points. Penny stocks, often representing smaller or newer companies, continue to present underappreciated potential for growth and remain a relevant investment area worth exploring.

Top 10 Penny Stocks In The United States

| Name | Share Price | Market Cap | Rewards & Risks |

| Waterdrop (WDH) | $1.67 | $593.13M | ✅ 4 ⚠️ 0 View Analysis > |

| LexinFintech Holdings (LX) | $2.33 | $403.83M | ✅ 3 ⚠️ 2 View Analysis > |

| FinVolution Group (FINV) | $4.86 | $1.29B | ✅ 4 ⚠️ 1 View Analysis > |

| Tuniu (TOUR) | $0.716 | $79.71M | ✅ 2 ⚠️ 2 View Analysis > |

| Information Services Group (III) | $3.11 | $188.79M | ✅ 3 ⚠️ 1 View Analysis > |

| Golden Growers Cooperative (GGRO.U) | $5.00 | $77.45M | ✅ 2 ⚠️ 5 View Analysis > |

| Niagen Bioscience (NAGE) | $4.54 | $377.97M | ✅ 3 ⚠️ 1 View Analysis > |

| Cricut (CRCT) | $4.13 | $876.77M | ✅ 2 ⚠️ 2 View Analysis > |

| LifeVantage (LFVN) | $4.33 | $58.13M | ✅ 4 ⚠️ 3 View Analysis > |

| SIGA Technologies (SIGA) | $7.80 | $357.51M | ✅ 3 ⚠️ 1 View Analysis > |

Click here to see the full list of 371 stocks from our US Penny Stocks screener.

We're going to check out a few of the best picks from our screener tool.

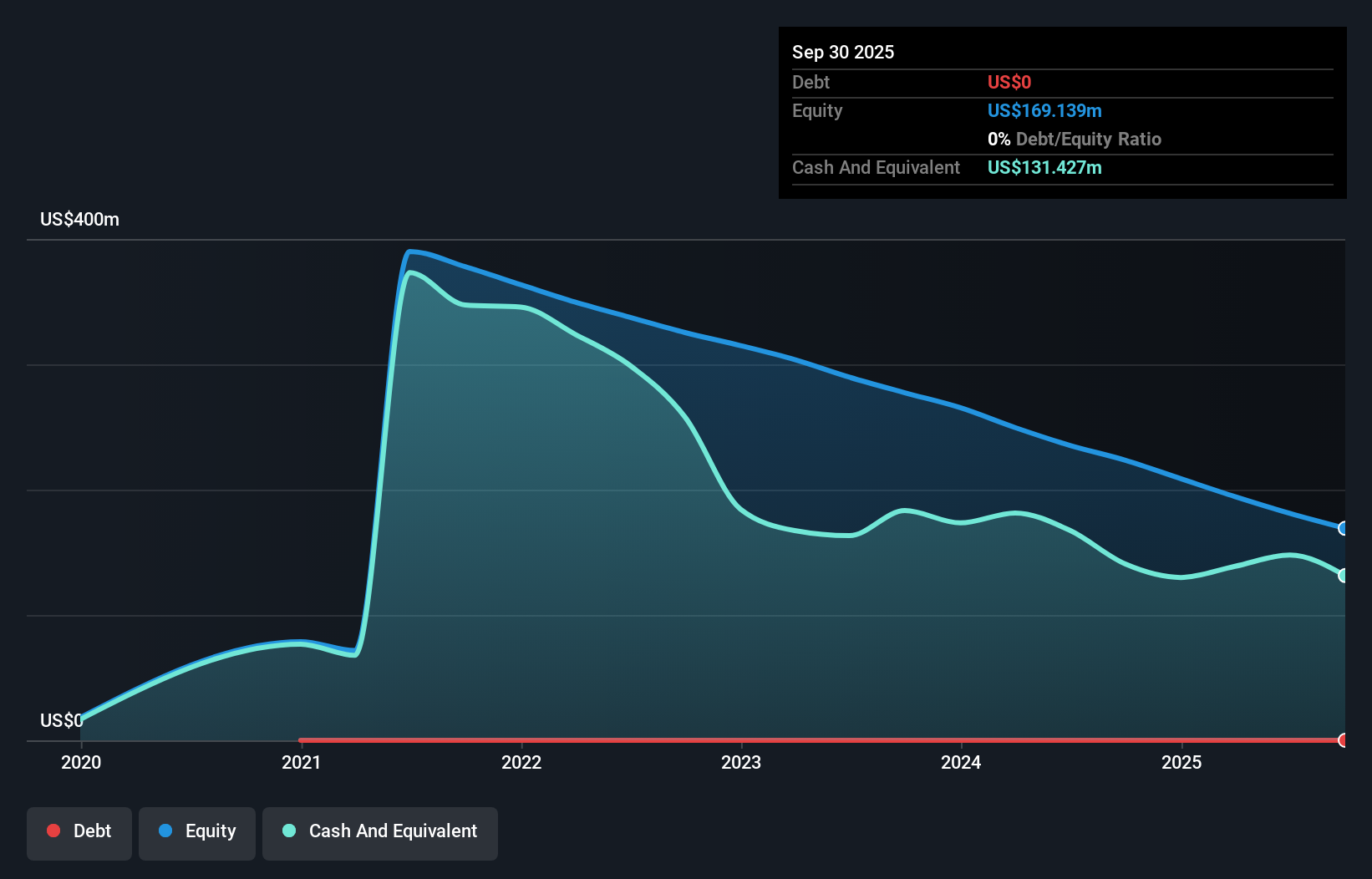

Nautilus Biotechnology (NAUT)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Nautilus Biotechnology, Inc. is a development stage life sciences company focused on creating a platform technology to quantify and unlock the complexity of the proteome in the United States, with a market cap of approximately $458.16 million.

Operations: Currently, Nautilus Biotechnology does not have any reported revenue segments.

Market Cap: $458.16M

Nautilus Biotechnology, a pre-revenue company with a market cap of US$458.16 million, is making strides in the life sciences sector despite its unprofitability and recent losses. The company recently announced Baylor College of Medicine as its first customer for the Iterative Mapping Early Access Program, which aims to advance cancer research through proteomics. Nautilus' debt-free status and sufficient cash runway provide financial stability while it develops its innovative Voyager Platform. This platform promises to revolutionize protein analysis by enabling detailed mapping of proteoforms, potentially positioning Nautilus for future growth in the biotech industry.

- Unlock comprehensive insights into our analysis of Nautilus Biotechnology stock in this financial health report.

- Understand Nautilus Biotechnology's earnings outlook by examining our growth report.

Cytek Biosciences (CTKB)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Cytek Biosciences, Inc. is a cell analysis solutions company that offers tools for biomedical research and clinical applications, with a market cap of approximately $605.47 million.

Operations: The company's revenue of $201.49 million is derived from its Scientific & Technical Instruments segment.

Market Cap: $605.47M

Cytek Biosciences, with a market cap of US$605.47 million, continues to face challenges as it remains unprofitable and its losses have grown over the past five years. Despite this, the company maintains a strong financial position with short-term assets of US$392 million exceeding both short and long-term liabilities. Recent earnings reports show revenue growth to US$201.49 million for 2025, though net losses increased significantly to US$66.54 million from the previous year. Cytek's cash runway extends beyond three years, providing some stability as it navigates its current financial hurdles and aims for future revenue growth in 2026.

- Click here to discover the nuances of Cytek Biosciences with our detailed analytical financial health report.

- Assess Cytek Biosciences' future earnings estimates with our detailed growth reports.

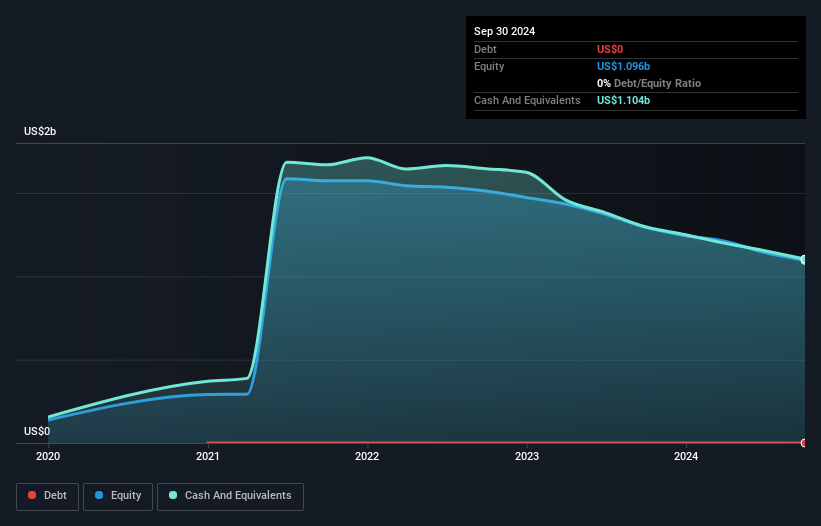

Marqeta (MQ)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Marqeta, Inc. operates a cloud-based open API platform for card issuing and transaction processing services in the United States, with a market cap of approximately $1.81 billion.

Operations: The company generates revenue primarily from its data processing segment, which amounts to $624.88 million.

Market Cap: $1.81B

Marqeta, Inc., with a market cap of US$1.81 billion, has shown revenue growth, reporting US$624.88 million for 2025 but remains unprofitable with a net loss of US$13.93 million. Despite its financial challenges, Marqeta benefits from being debt-free and having substantial short-term assets of US$1.2 billion that cover both short and long-term liabilities comfortably. The company has reduced losses over the past five years by 21.6% annually and maintains a positive cash flow runway exceeding three years, supporting its strategy for growth amidst market volatility and recent executive changes in leadership roles.

- Jump into the full analysis health report here for a deeper understanding of Marqeta.

- Evaluate Marqeta's prospects by accessing our earnings growth report.

Turning Ideas Into Actions

- Dive into all 371 of the US Penny Stocks we have identified here.

- Searching for a Fresh Perspective? Trump's oil boom is here — pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com