- LIVE QUOTES

- LEARN

- HELP

EN

US Market's 3 Undiscovered Gems With Promising Potential

Over the last 7 days, the United States market has experienced a 2.3% drop, yet it remains up by 13% over the past year with earnings projected to grow by 16% annually. In this context, identifying stocks with strong fundamentals and growth potential can be key to uncovering promising opportunities in an evolving market landscape.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Tri-County Financial Group | 70.32% | -2.03% | -13.70% | ★★★★★★ |

| Southern Michigan Bancorp | 110.37% | 7.93% | 2.26% | ★★★★★★ |

| Cashmere Valley Bank | 31.17% | 5.25% | 1.74% | ★★★★★★ |

| ASA Gold and Precious Metals | NA | 12.65% | 41.20% | ★★★★★★ |

| Sound Financial Bancorp | 16.27% | 0.75% | -13.28% | ★★★★★★ |

| Epsilon Energy | NA | 2.43% | -4.36% | ★★★★★★ |

| Affinity Bancshares | 42.51% | 1.82% | 1.11% | ★★★★★★ |

| Winchester Bancorp | 121.44% | 49.13% | 3283.33% | ★★★★★★ |

| Union Bankshares | 374.44% | 1.11% | -7.71% | ★★★★★☆ |

| Seneca Foods | 38.64% | 2.39% | -18.65% | ★★★★★☆ |

We'll examine a selection from our screener results.

One and one Green Technologies (YDDL)

Simply Wall St Value Rating: ★★★★★★

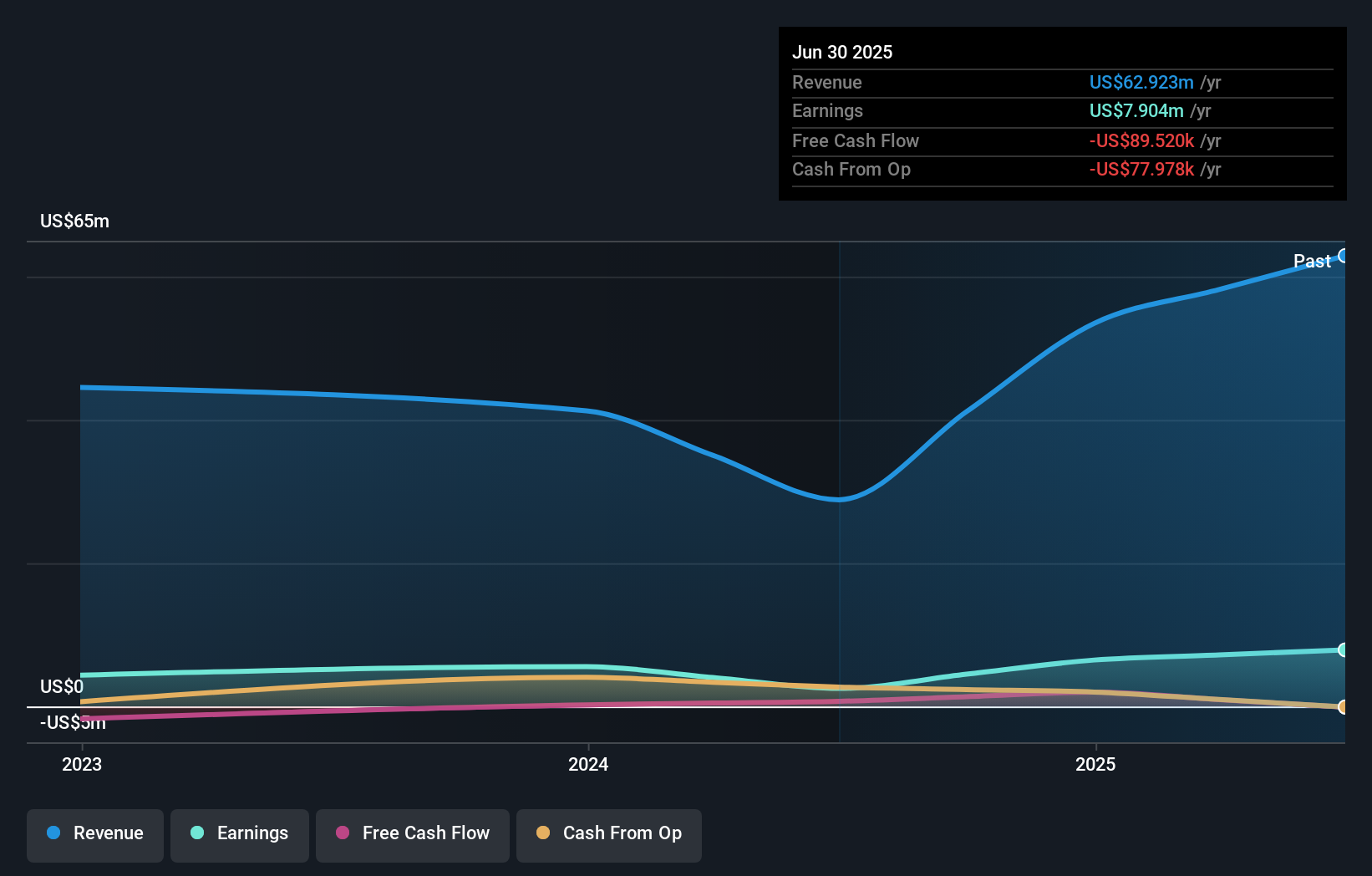

Overview: One and one Green Technologies, Inc is a waste materials and scrap metal recycling company involved in the recycling, production, and trading of recycled scrap metals in the Philippines with a market cap of $563.63 million.

Operations: YDDL generates revenue primarily from its Metal Processors and Fabrication segment, which reported $62.92 million. The company's financial performance is influenced by its ability to manage costs associated with recycling and production processes.

One and One Green Technologies, a nimble player in the e-waste sector, is making strategic moves to capture market share in the Philippines. With a 1 million-ton-per-year hazardous waste permit, it plans to process high-value materials like copper and nickel mud. Recent upgrades at its San Rafael facility have increased PCB processing capacity by over 30% and improved metal extraction efficiency by up to 20%. Notably, earnings surged by 214% last year, outpacing industry growth of 96%. Despite a volatile share price recently, the company remains debt-free with strong non-cash earnings.

Envela (ELA)

Simply Wall St Value Rating: ★★★★★★

Overview: Envela Corporation, with a market cap of $433.59 million, operates in the United States offering recommerce and recycling services through its subsidiaries.

Operations: The company generates revenue primarily from its Consumer and Commercial segments, with the Consumer segment contributing $192.72 million and the Commercial segment $48.30 million.

Envela, a nimble player in the specialty retail sector, recently reported impressive financials. Sales surged to US$241.02 million from US$180.38 million year-on-year, while net income jumped to US$14.6 million from US$6.76 million. The company's earnings per share doubled to $0.56, reflecting robust growth and efficiency improvements over the past year with earnings expanding by 116%, outpacing the industry average of -1.1%. Envela's debt-to-equity ratio has significantly decreased from 87.7% to 14.8% in five years, showcasing prudent financial management and a solid footing for future endeavors in this dynamic market space.

- Take a closer look at Envela's potential here in our health report.

Gain insights into Envela's past trends and performance with our Past report.

CTS (CTS)

Simply Wall St Value Rating: ★★★★★★

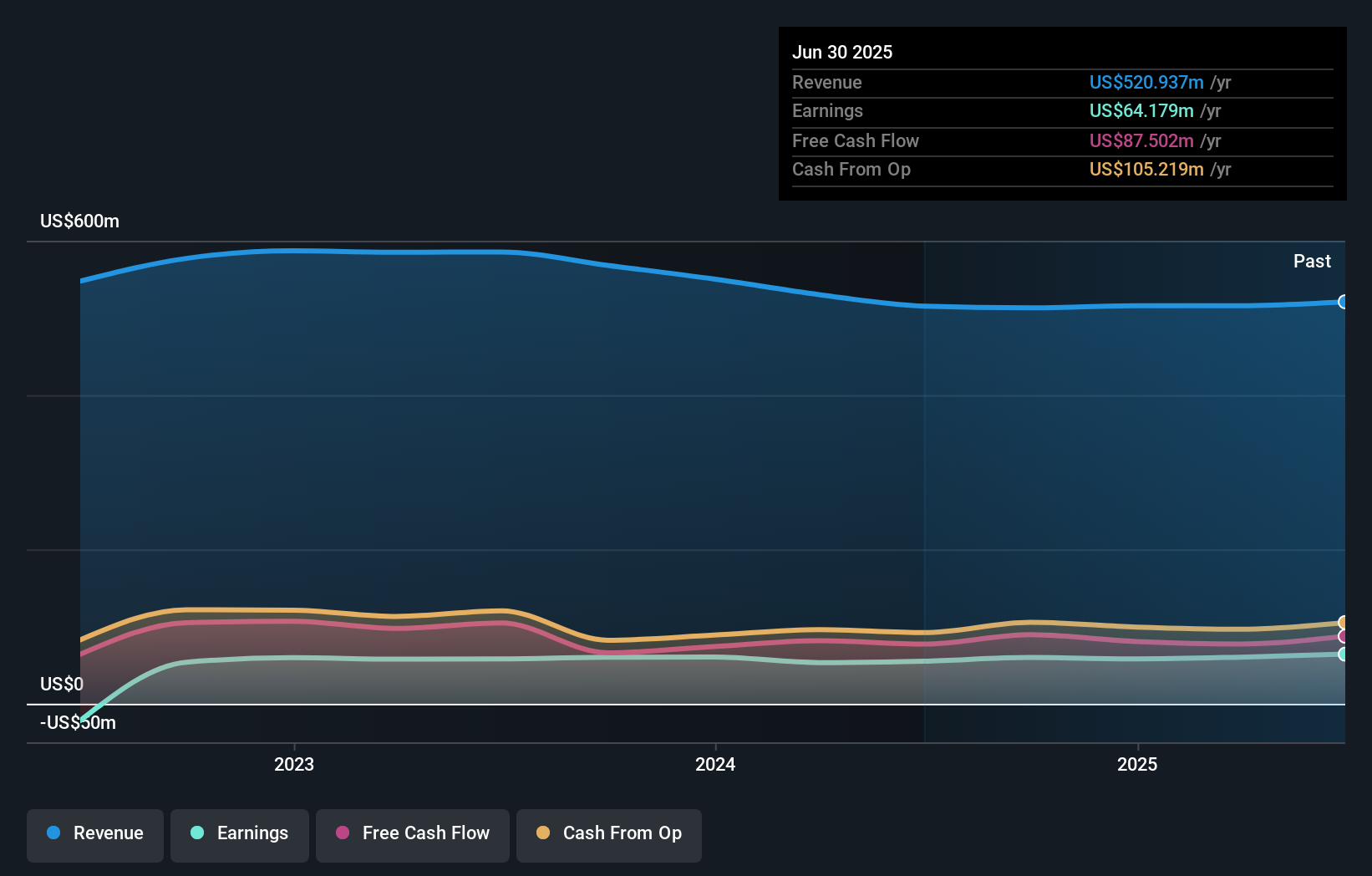

Overview: CTS Corporation designs, manufactures, and sells sensors, connectivity components, and actuators across North America, Europe, and Asia with a market capitalization of approximately $1.40 billion.

Operations: CTS generates revenue primarily through its Electronic Components & Parts segment, which reported $541.32 million. The company's financial performance is reflected in its gross profit margin trend, which provides insight into its cost management and pricing strategies over time.

CTS, an electronics company with a market focus on high-growth sectors like medical and industrial, has demonstrated robust financial health. Over the past year, earnings grew by 17.7%, outpacing the electronic industry average of 17.4%. The company's debt to equity ratio improved from 13.4% to 10.4% over five years, indicating prudent financial management. With EBIT covering interest payments by a factor of 38.5 times, CTS's interest obligations are well managed. Recent activities include repurchasing approximately $57 million worth of shares in 2025 and maintaining strong cash generation capabilities with $102 million in operating cash flow for that year.

Seize The Opportunity

- Delve into our full catalog of 321 US Undiscovered Gems With Strong Fundamentals here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com