- LIVE QUOTES

- LEARN

- HELP

EN

How Trane’s NVIDIA-Aligned AI Data Center Thermal Upgrades Could Reshape Trane Technologies (TT) Investors’ Thesis

- In March 2026, Trane Technologies announced major upgrades to its gigawatt-scale AI factory thermal management reference design and introduced two new Trane Continuum Rubin DSX designs, engineered to integrate with NVIDIA’s Omniverse DSX Blueprint and deliver nearly 10% better overall thermal management performance than its original 1-gigawatt model.

- This deepening collaboration with NVIDIA and expansion of high-efficiency solutions for large-scale AI deployments highlights Trane’s push into AI data center infrastructure as a specialized growth avenue within its HVAC portfolio.

- Next, we’ll explore how Trane’s enhanced NVIDIA-aligned AI data center thermal designs might influence its investment narrative and growth assumptions.

Capitalize on the AI infrastructure supercycle with our selection of the 34 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Trane Technologies Investment Narrative Recap

To own Trane Technologies, you generally need to believe in sustained demand for energy efficient commercial HVAC and growing services, with data centers as a key vertical. The NVIDIA-aligned AI factory thermal designs support that data center story, but do not materially change the near term catalysts of commercial HVAC bookings strength or the biggest current risks around a potential slowdown in data center and transport markets.

Among recent announcements, Trane’s 12% dividend increase to US$1.05 per share in February 2026 stands out. It reinforces management’s confidence in cash generation just as the company leans further into AI data center thermal solutions, which could complement its established HVAC and services engine that underpins those rising capital returns.

Yet beneath the AI data center opportunity, investors should also be aware of the risk that a future slowdown in data center construction or spending could...

Read the full narrative on Trane Technologies (it's free!)

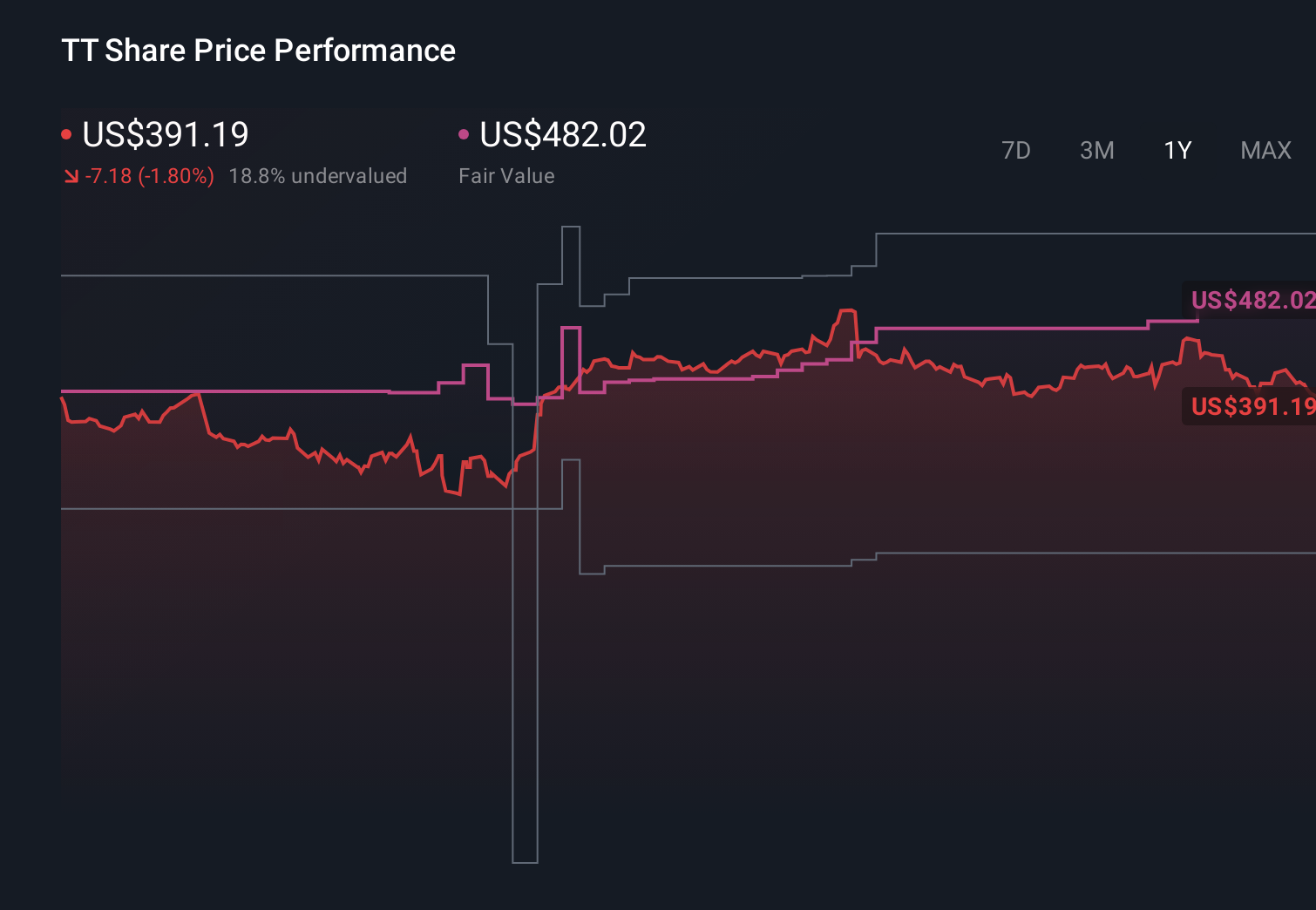

Trane Technologies' narrative projects $25.4 billion revenue and $3.7 billion earnings by 2028.

Uncover how Trane Technologies' forecasts yield a $479.73 fair value, a 13% upside to its current price.

Exploring Other Perspectives

While consensus sees balanced growth, the most pessimistic analysts expect only about US$26.0 billion of revenue and US$3.9 billion of earnings by 2029, highlighting how concerns about over reliance on North American commercial HVAC and possible future data center slowdowns can diverge sharply from more optimistic takes on Trane’s AI factory momentum.

Explore 4 other fair value estimates on Trane Technologies - why the stock might be worth as much as 13% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Trane Technologies research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Trane Technologies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Trane Technologies' overall financial health at a glance.

No Opportunity In Trane Technologies?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 21 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- AI is about to change healthcare. These 36 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com