- LIVE QUOTES

- LEARN

- HELP

EN

Is Alliant Energy (LNT) Fairly Priced After Recent Share Price Pullback?

- Wondering if Alliant Energy’s current share price reflects its real worth, or if you might be paying too much for a regulated utility stock right now?

- The stock last closed at US$68.71, with a 7 day return of a 5.6% decline, a 30 day return of a 1.2% decline, a 1 year return of 12.5%, a 3 year return of 46.9%, and a 5 year return of 49.7%.

- These moves have come as investors continue to reassess regulated utilities as an income and stability option. Alliant Energy has attracted attention as part of that broader interest. Recent coverage has focused on how the stock fits into portfolios that balance income needs with potential for capital returns, which helps frame how you might think about its current price.

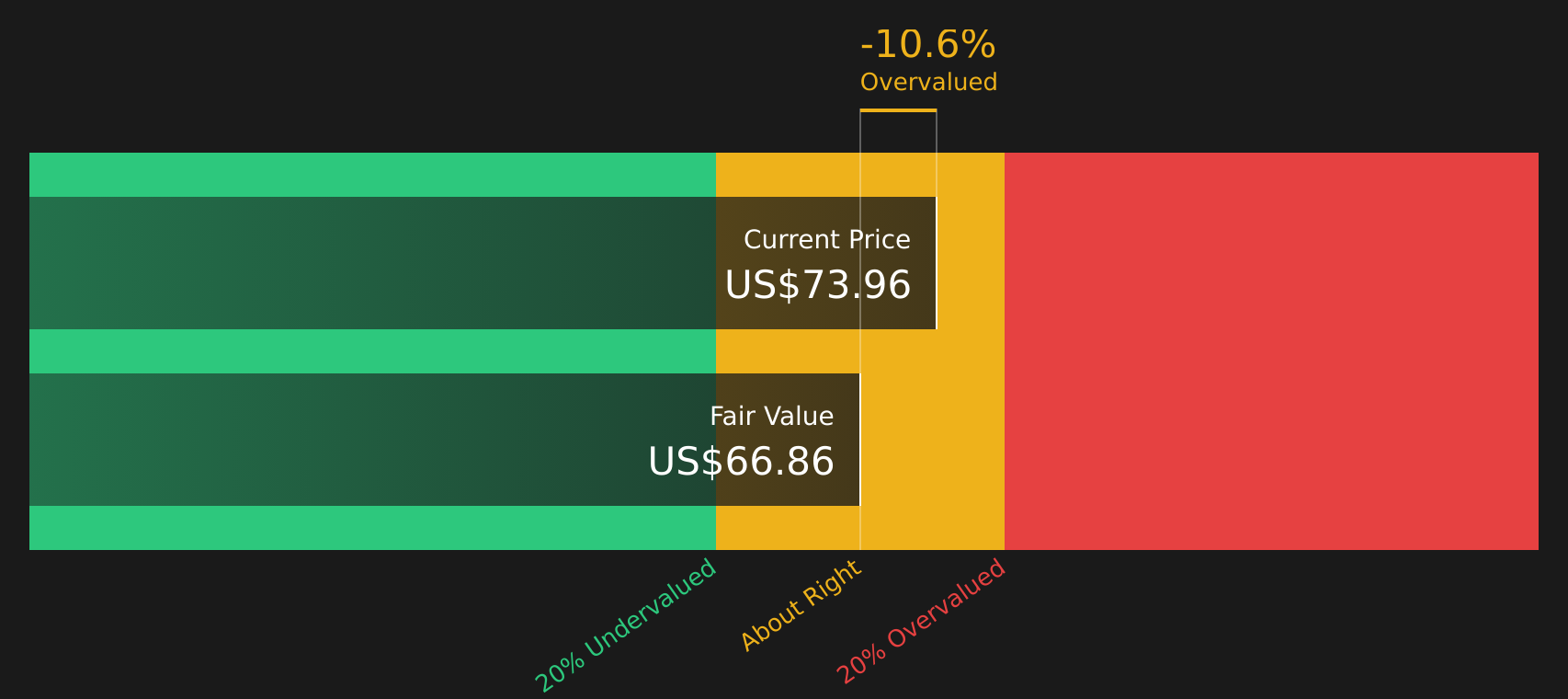

- Even with that interest, Alliant Energy currently has a valuation score of 1 out of 6. The next step is to look at how different valuation methods judge the stock today, and then finish with a way to assess value that goes beyond any single model.

Alliant Energy scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Alliant Energy Dividend Discount Model (DDM) Analysis

The Dividend Discount Model estimates what a stock might be worth by projecting future dividends and discounting them back to today, then comparing that value with the current share price.

For Alliant Energy, the model uses a dividend per share of US$2.40, a return on equity of 10.62%, and a payout ratio of about 66%. Dividend growth in the model is capped at 3.41%, with an expected growth input of 3.60%. This keeps the forecast grounded in moderate, sustainable dividend growth rather than assuming aggressive expansion.

Using these inputs, the DDM arrives at an estimated intrinsic value of about US$67.16 per share. Compared with the recent share price of US$68.71, the model implies the stock is roughly 2.3% overvalued. That is a very small gap and within the sort of range where normal market fluctuations can easily close the difference.

On this DDM view, Alliant Energy appears close to fairly priced, with only a slight premium to the model’s estimate.

Result: ABOUT RIGHT

Alliant Energy is fairly valued according to our Dividend Discount Model (DDM), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: Alliant Energy Price vs Earnings

For profitable companies, the P/E ratio is a useful way to relate what you are paying for each share to the earnings that support that price. It gives a quick sense of how much of a premium or discount the market is putting on those earnings.

What counts as a “normal” P/E partly reflects expectations for future growth and the risk investors see in those earnings. Higher expected growth or lower perceived risk can justify a higher P/E, while lower growth or higher risk usually points to a lower multiple.

Alliant Energy currently trades on a P/E of 21.81x. That sits above the Electric Utilities industry average of 20.70x and the peer average of 16.32x. Simply Wall St’s Fair Ratio for Alliant Energy is 24.28x. This is its view of a more tailored P/E based on factors such as earnings growth, profit margin, industry, market cap and key risks.

This Fair Ratio can be more informative than a simple peer or industry comparison because it adjusts for those company specific characteristics, rather than assuming all utilities deserve the same multiple. With the current P/E below the 24.28x Fair Ratio, this approach points to the shares being undervalued on earnings.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Alliant Energy Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are introduced as a simple way for you to spell out your story about Alliant Energy, connect that story to a forecast for revenue, earnings and margins, and then see a Fair Value that you can compare with the current price on Simply Wall St’s Community page. There, different investors can, for example, set a bullish Narrative closer to US$74.50 or a more cautious one around US$60.00, and have those Fair Values update automatically when new news or earnings arrive, so you can judge for yourself whether the price looks high, low, or about right for your view.

Do you think there's more to the story for Alliant Energy? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com