- LIVE QUOTES

- LEARN

- HELP

EN

A Look At Align Technology (ALGN) Valuation As Elliott Investment Management Takes A Major Stake

Elliott Investment Management has quietly become one of the largest shareholders in Align Technology (ALGN), preparing to engage management on options to improve stock performance, a development that has quickly drawn investor attention.

See our latest analysis for Align Technology.

At a share price of US$173.18, Align has seen a 5.45% 7 day share price return and a 9.82% 90 day share price return. The 3 year total shareholder return of a 43.53% decline indicates that longer term momentum has been weaker, even as recent news around activist involvement, conference commentary and the SprintRay collaboration has brought fresh attention to the stock.

If this kind of catalyst driven story interests you, it can be worth widening the search to other dental and medical names using our healthcare AI stock ideas via the 35 healthcare AI stocks.

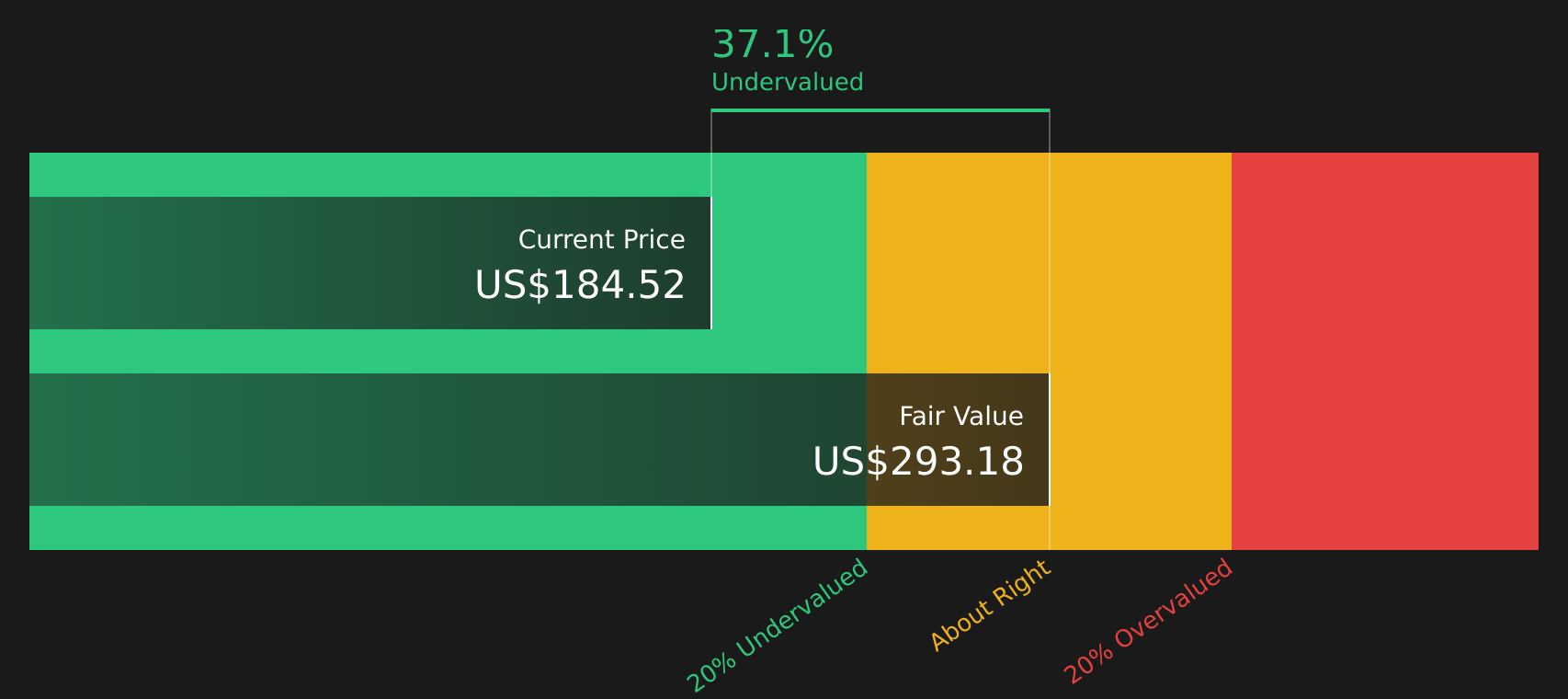

With Align trading at US$173.18 and sitting at a 19% discount to one intrinsic estimate and a similar gap to analyst targets, you have to ask: is this a genuine opportunity, or is the market already baking in future growth?

Most Popular Narrative: 12% Overvalued

According to the most followed narrative, Align's fair value of $154.62 sits below the current $173.18 share price, which frames the activist interest in a different light.

Align Technology is no longer proving that clear aligners work. It is proving that premium orthodontics can endure in a cost-sensitive world. For investors, ALGN represents a business built on medical credibility as much as consumer appeal. If Align continues to align innovation with clinical rigor, it may retain its leadership not through price competition, but through outcomes that justify the premium.

Curious what sits behind that premium argument? The narrative leans heavily on long term margin resilience, measured revenue expansion, and a profit multiple that assumes those strengths hold. The full breakdown shows exactly how those moving parts support a fair value below today's price.

Result: Fair Value of $154.62 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this premium story can break if clear aligner competitors close the quality gap, or if pressure on discretionary dental spending undercuts Align’s pricing power.

Find out about the key risks to this Align Technology narrative.

Another View: Cash Flows Point the Other Way

While the popular narrative pins fair value at $154.62 and characterizes Align as overvalued, the SWS DCF model points in the opposite direction. On that approach, the stock price of $173.18 sits about 19% below an estimated cash flow value of $214.68, raising a simple question: which story do you find more convincing?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Align Technology for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 52 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment this mixed, it helps to look past the headlines and weigh the numbers yourself. Then move quickly while the picture is clear and see how the balance of 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If Align is on your radar, now is a good moment to broaden your watchlist and line up a few other candidates that could complement your portfolio.

- Target quality at a discount by scanning companies that combine earnings strength with attractive pricing using the 52 high quality undervalued stocks.

- Focus on resilience first and hunt for businesses that prioritize balance sheet strength and stable fundamentals through the solid balance sheet and fundamentals stocks screener (39 results).

- Spot opportunities others might overlook by using the screener containing 26 high quality undiscovered gems before these names attract wider attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com