- LIVE QUOTES

- LEARN

- HELP

EN

How Varonis’ New Atlas AI Security Platform Launch Will Impact Varonis Systems (VRNS) Investors

- Earlier this month, Varonis Systems launched Varonis Atlas, an end-to-end AI security platform that discovers, secures, and monitors AI systems across the enterprise, integrating with its existing data security suite and offering a free trial for capabilities such as AI posture management, runtime guardrails, and compliance reporting.

- This move extends Varonis beyond data protection into full AI lifecycle security, potentially deepening its role in how enterprises safely operationalize AI agents, copilots, and custom LLMs.

- We’ll now explore how Atlas’s AI lifecycle coverage and tight integration with Varonis’s data security platform could influence the company’s investment narrative.

We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

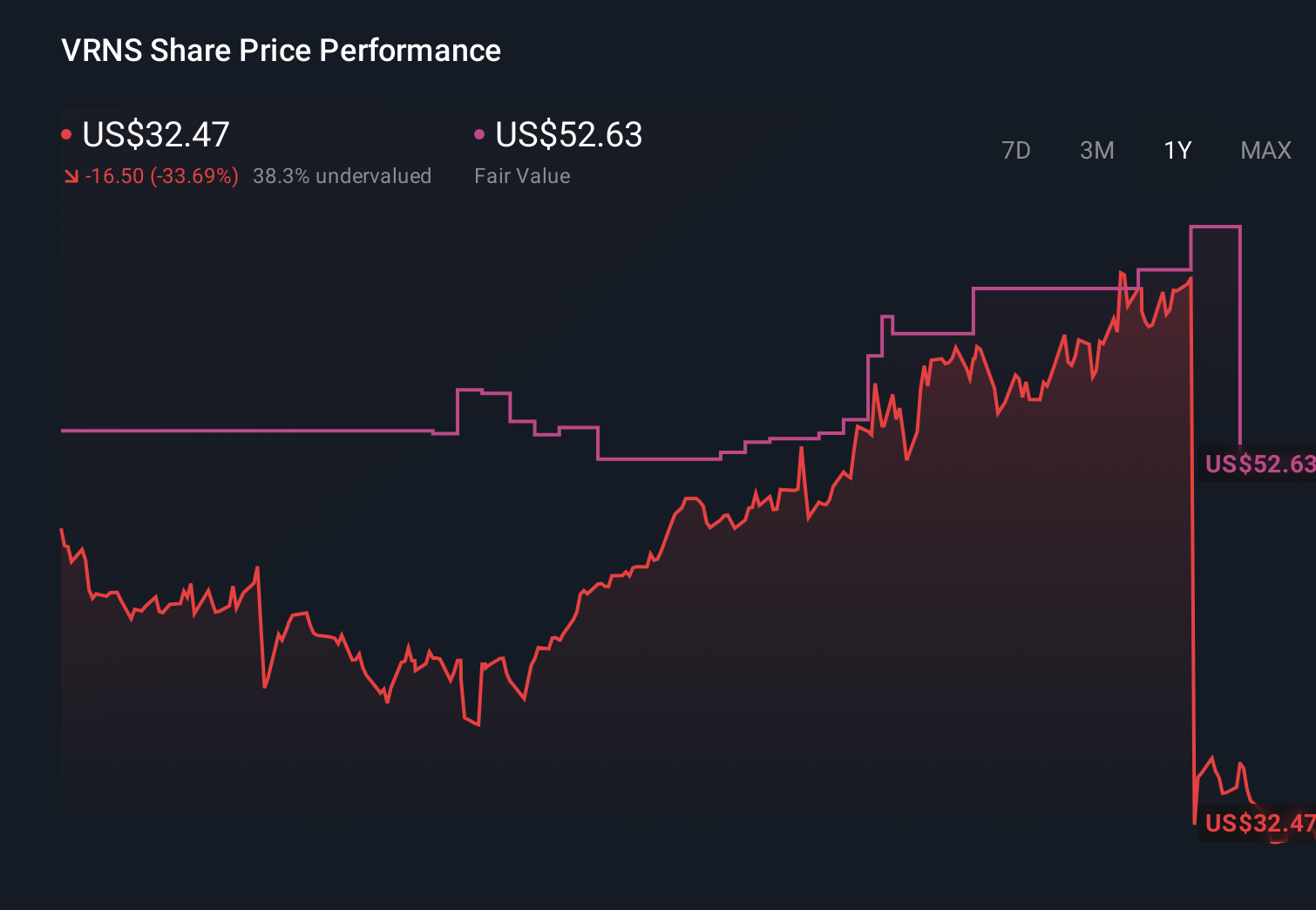

Varonis Systems Investment Narrative Recap

To own Varonis, you need to believe that securing unstructured data and AI workflows becomes mission critical, and that Varonis can turn that demand into durable, recurring SaaS revenue despite current losses. The launch of Atlas sharpens that story by extending protection from data to AI systems, but it does not remove near term concerns around revenue recognition during the SaaS transition, margin pressure, and whether ARR growth will ultimately flow through to earnings.

Among recent updates, the 2026 guidance stands out next to Atlas. Management guided to 2026 revenue of US$722.0 million to US$730.0 million and SaaS ARR growth of 26 to 32 percent, while the stock sold off after full year EPS guidance fell short of expectations. Atlas now sits against that backdrop as a new product that could support SaaS ARR expansion, but investors will be watching whether it meaningfully improves conversion, upsell, and profitability over time.

Yet investors should also weigh how rising share count and ongoing losses could still pressure returns if Atlas adoption or SaaS conversions fall short of expectations...

Read the full narrative on Varonis Systems (it's free!)

Varonis Systems' narrative projects $911.4 million revenue and $119.3 million earnings by 2028.

Uncover how Varonis Systems' forecasts yield a $33.90 fair value, a 43% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts were already assuming revenue of about US$979 million and only US$32 million of earnings by 2029, so compared with the baseline they are building in a much tougher path to profitability that news like the Atlas launch could either challenge or reinforce, and you should expect that views like this may shift as new information comes through.

Explore 3 other fair value estimates on Varonis Systems - why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Varonis Systems research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Varonis Systems research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Varonis Systems' overall financial health at a glance.

No Opportunity In Varonis Systems?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 28 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Outshine the giants: these 21 early-stage AI stocks could fund your retirement.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com