- LIVE QUOTES

- LEARN

- HELP

EN

Does V2X’s Elastic Partnership Reshape Its Data-Driven Mission Solutions Story For VVX Investors?

- On 16 March 2026, V2X, Inc. announced a collaboration with Elastic to integrate advanced search and analytics for government, defense, and intelligence customers, aiming to speed access to critical information while meeting strict security and compliance standards.

- This partnership highlights V2X’s push to deepen its role in data-enabled mission solutions by enhancing multi-source analysis, logistics support, and cyber resilience for public-sector and commercial clients.

- Now we will examine how this focus on enhanced data analytics for government and defense missions could influence V2X’s existing investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 34 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

V2X Investment Narrative Recap

To own V2X, you generally need to believe it can turn a large government and defense opportunity into durable earnings growth, despite contract timing and backlog risks. The Elastic collaboration fits the push into higher value, data-enabled mission work, but it does not directly change the near term dependence on winning and executing large, sometimes binary awards, or on stabilizing book to bill and backlog trends that remain central to the story.

The recent extension of V2X’s multi year, US$100 million plus training contract with General Motors through 2030 reinforces the company’s ability to secure long duration work outside core defense programs. While smaller than major Pentagon awards, this deal adds a measure of revenue stability and diversification that can help offset timing swings in government contracting, which is particularly relevant as V2X leans further into digital and analytics driven offerings with partners like Elastic.

Yet, behind the growing focus on advanced analytics and long term contracts, investors should still be aware of the risk that...

Read the full narrative on V2X (it's free!)

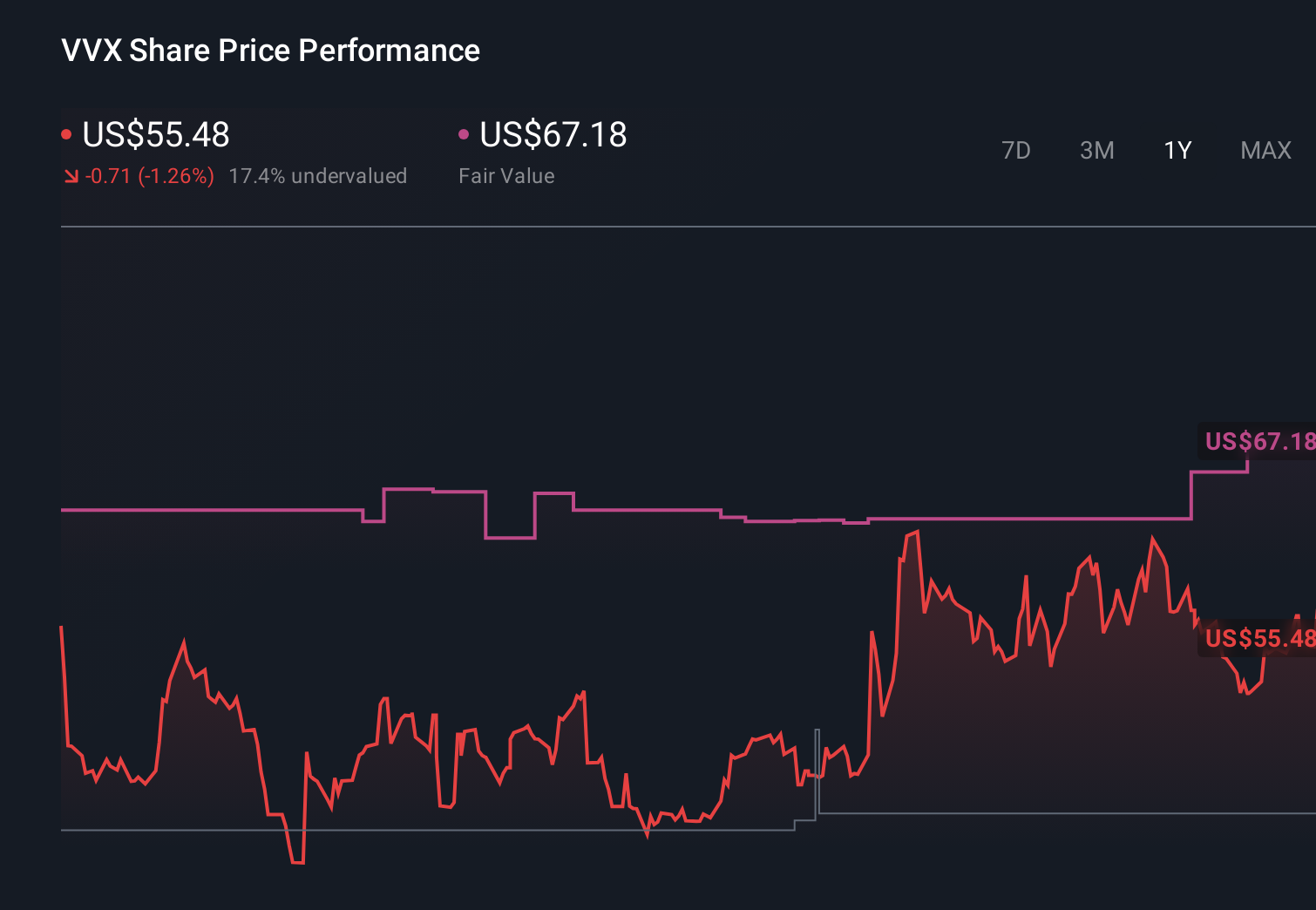

V2X's narrative projects $5.0 billion revenue and $148.8 million earnings by 2028. This requires 4.8% yearly revenue growth and a $78.2 million earnings increase from $70.6 million today.

Uncover how V2X's forecasts yield a $75.88 fair value, a 11% upside to its current price.

Exploring Other Perspectives

While the consensus view leans on a robust US$50 billion pipeline, the most pessimistic analysts expected only about 3.2% annual revenue growth and US$119.3 million of earnings by 2028, reminding you that reasonable people can read the same V2X news very differently and that both the bullish and bearish cases may shift as partnerships like Elastic reshape what the business looks like over time.

Explore 4 other fair value estimates on V2X - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your V2X research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free V2X research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate V2X's overall financial health at a glance.

Interested In Other Possibilities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 28 best rare earth metal stocks of the very few that mine this essential strategic resource.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com