- LIVE QUOTES

- LEARN

- HELP

EN

What PDF Solutions (PDFS)'s Margin Gains and Analytics Pivot Means For Shareholders

- Earlier in March 2026, PDF Solutions reported a strong fourth-quarter 2025 performance, with revenue growth and higher gross margins following management’s update on its evolving business model and expanding role in networking and scaled analytics across the semiconductor ecosystem.

- An interesting angle is how PDF Solutions is increasingly positioning its analytics and networking offerings as core infrastructure for semiconductor supply-chain collaboration and manufacturing optimization.

- Next, we will examine how PDF Solutions’ stronger margins and expanding role in scaled semiconductor analytics influence its existing investment narrative.

The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

PDF Solutions Investment Narrative Recap

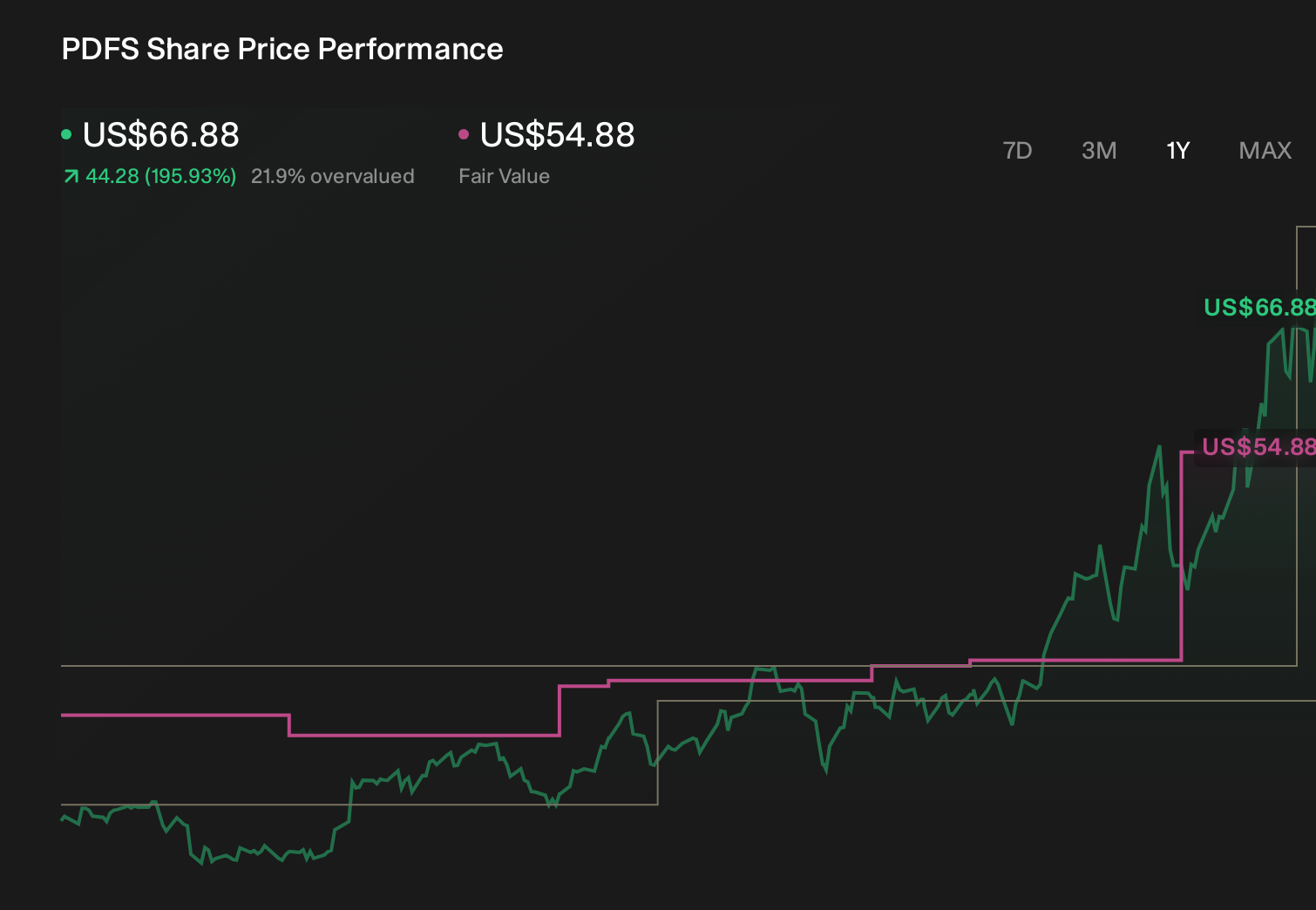

To own PDF Solutions, you need to believe its analytics and networking platforms can become embedded infrastructure across the semiconductor supply chain, turning data connectivity into a durable, higher-margin business. The latest Q4 2025 beat on revenue and gross margins supports that thesis, but near term the key catalyst remains execution on recurring, cloud-based analytics growth, while the biggest risk is that concentrated large customers or in-house tools blunt that momentum. This news does not materially change those priorities.

Among recent developments, the Q4 2025 update that FY2026 revenue is expected to grow in line with the company’s 20% long term target directly ties into the scaled analytics story. It reinforces the idea that PDF Solutions is leaning into its role in networking and manufacturing optimization, even as it remains just shy of sustained profitability after a modest 2025 net loss. For investors, that guidance sharpens the focus on whether higher-margin software and analytics can fully offset ongoing cost intensity.

Yet behind the improving margins and growth targets, investors should be aware of how quickly generative AI could compress pricing and erode differentiation if...

Read the full narrative on PDF Solutions (it's free!)

PDF Solutions' narrative projects $330.7 million revenue and $47.9 million earnings by 2028. This requires 19.0% yearly revenue growth and roughly a $47.0 million earnings increase from $859.0 thousand today.

Uncover how PDF Solutions' forecasts yield a $36.00 fair value, a 13% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenue could reach about US$340.3 million and earnings US$46.1 million by 2028, which is a far more ambitious path than the baseline view that emphasizes steady adoption and execution risk around AI driven commoditization. This latest analytics focused news could either support those higher expectations or force a rethink, so it is worth comparing how your own assumptions line up with both narratives.

Explore 5 other fair value estimates on PDF Solutions - why the stock might be worth as much as 37% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your PDF Solutions research is our analysis highlighting 1 key reward that could impact your investment decision.

- Our free PDF Solutions research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate PDF Solutions' overall financial health at a glance.

Contemplating Other Strategies?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 19 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com