- LIVE QUOTES

- LEARN

- HELP

EN

Assessing Credit Acceptance (CACC) Valuation After Recent Share Price Pullback

Why Credit Acceptance Is on Investors’ Radar

Without a single headline event driving attention, Credit Acceptance (CACC) is drawing interest as investors weigh its recent share performance against its current size, profitability profile, and niche in US auto financing.

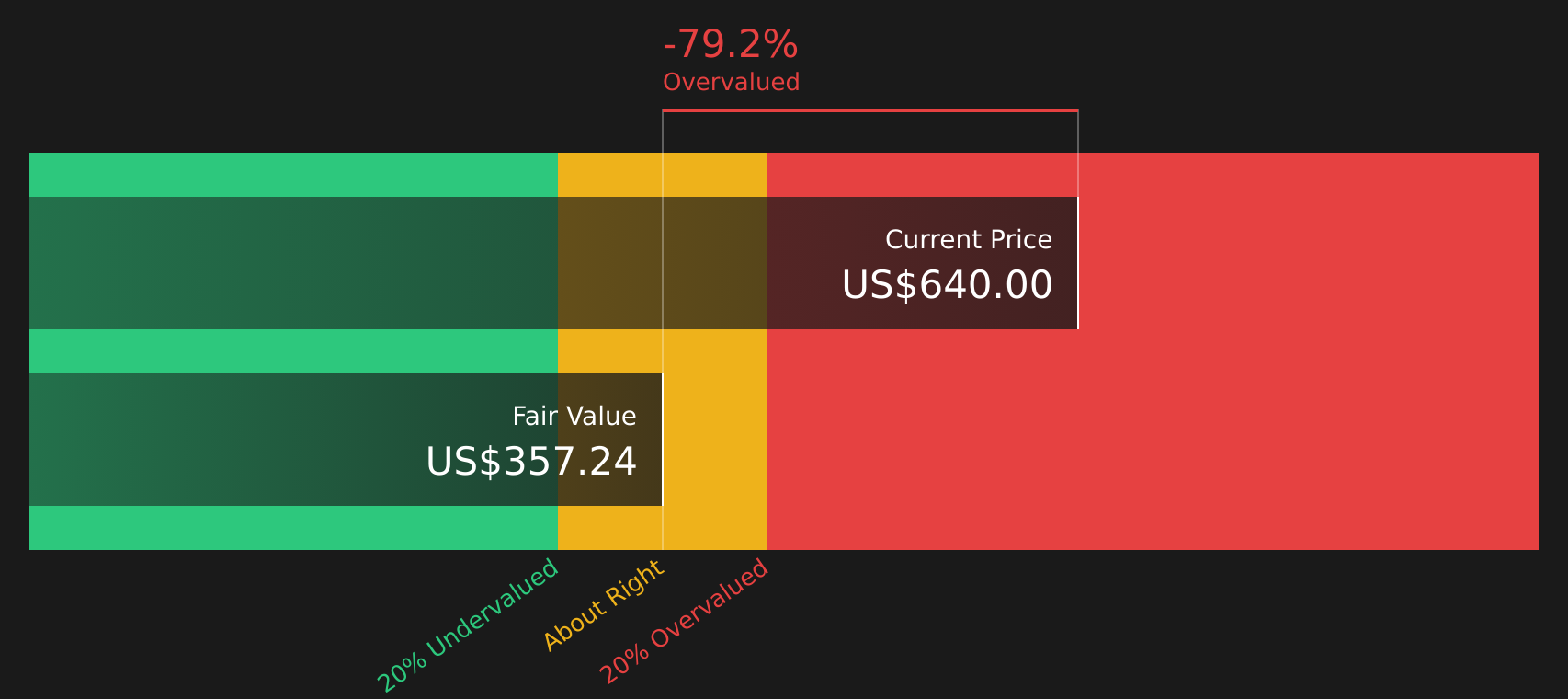

See our latest analysis for Credit Acceptance.

The share price has stepped back to $447.79 after a 9.35% 1 day decline and a 10.72% 7 day share price return. The 1 year total shareholder return of an 8.02% decline contrasts with positive 3 and 5 year total shareholder returns, suggesting weaker recent performance alongside a stronger longer term record.

If you are looking beyond auto finance for ideas, it could be a good time to scan 20 top founder-led companies

With shares pulling back and analyst targets sitting only slightly higher, the key question now is simple: does Credit Acceptance trade below its underlying value, or is the market already pricing in its future growth potential?

Most Popular Narrative: 2.2% Undervalued

The most followed valuation narrative places Credit Acceptance’s fair value at $458 per share, slightly above the last close of $447.79. This frames the current pullback as relatively modest against that estimate.

The recent investments in technology modernization, including a revamped loan origination system and accelerated feature development, should improve customer and dealer experiences, drive operating efficiency, and support net margin improvement through cost reductions. Adoption of more advanced data analytics and ongoing scorecard updates are expected to enhance risk assessment and loan performance over coming vintages, reducing future default rates and stabilizing or expanding net margins and earnings.

Want to see what sits behind that fair value gap? Revenue growth assumptions, margin compression, and future earnings multiples are combined in one detailed roadmap.

Result: Fair Value of $458 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you also need to factor in weaker recent loan performance and tougher competition in subprime auto, both of which could pressure margins and growth.

Find out about the key risks to this Credit Acceptance narrative.

Another View: Cash Flows Paint A Tougher Picture

While the prevailing narrative sees Credit Acceptance as 2.2% undervalued at a fair value of $458 per share, the SWS DCF model points the other way. On that approach, the shares at $447.79 sit above an estimated future cash flow value of $304.33. This frames the stock as overvalued on this metric and raises a simple question: which story do you trust more, earnings or cash flows?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Credit Acceptance for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 48 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed messages on value and risk can be confusing, so move quickly, review the assumptions for yourself, and weigh up the 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Credit Acceptance has your attention today, do not stop there; expanding your watchlist across sectors and styles can help you spot opportunities others overlook.

- Target potential mispricings by scanning 48 high quality undervalued stocks that combine quality fundamentals with prices that may not fully reflect their financial profiles.

- Build a steadier income stream by reviewing 14 dividend fortresses that pair higher yields with an emphasis on resilience.

- Protect your downside by focusing on 70 resilient stocks with low risk scores that score well on balance sheet strength and overall risk checks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com