- LIVE QUOTES

- LEARN

- HELP

EN

Emerson Electric (EMR) Valuation Check After Earnings Beat And US$10b Shareholder Return Plan

Emerson Electric (EMR) has drawn fresh attention after reporting quarterly earnings that exceeded analyst expectations, raising full year earnings guidance and outlining plans for a US$250 million buyback and US$10 billion in shareholder returns by 2028.

See our latest analysis for Emerson Electric.

Despite the earnings beat and higher guidance, recent share price returns have been soft, with a 30 day share price return of 10.73% and a year to date share price return of 2.64%. In contrast, the 1 year total shareholder return of 20.11% and 3 year total shareholder return of 73.20% point to stronger longer term momentum supported by dividends and past price gains.

If this has you thinking about where else capital goods style trends like electrification and energy infrastructure could play out, you might want to scan our 24 power grid technology and infrastructure stocks as a starting list of ideas.

So with earnings ahead of expectations, higher guidance, softer recent returns and a current price of US$132.24 against an average analyst target of US$166.66, is Emerson Electric offering an opportunity, or is the market already pricing in future growth?

Most Popular Narrative: 19.6% Undervalued

Emerson Electric's most followed narrative points to a fair value of about $164.51 per share, compared with the last close of $132.24. This frames the recent earnings beat against longer term expectations.

The accelerating adoption of digital automation and artificial intelligence solutions in global industrial markets is fueling strong demand for Emerson's advanced software platforms and AI-enabled products, such as Ovation 4.0 and Nigel AI adviser, which is resulting in robust order growth and positions the company for sustained revenue expansion.

Curious what that growth story actually looks like in numbers? The narrative leans on steadier revenue, expanding margins and a future earnings base that assumes AI driven orders keep flowing. The valuation hinges on how those earnings and the future P/E line up over the next few years, not just the latest quarter.

Result: Fair Value of $164.51 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still clear pressure points, including tariff and currency swings, as well as any setback in AspenTech or AI software execution, that could quickly challenge this upbeat view.

Find out about the key risks to this Emerson Electric narrative.

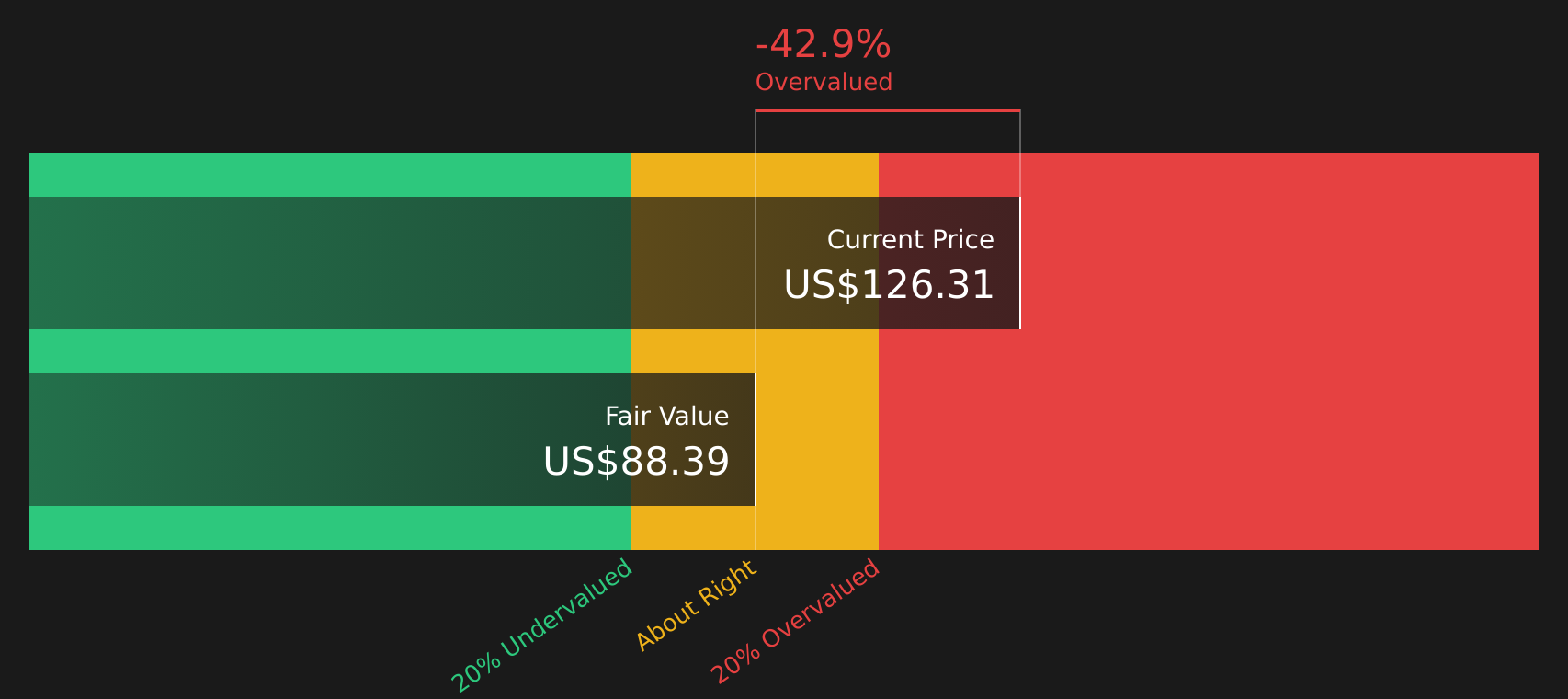

Another Angle on Valuation

There is a very different message coming from our DCF model, which points to a value of about $78.13 per share versus the current $132.24. In this view, the stock appears expensive rather than undervalued. The key question is which set of assumptions you consider more realistic.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Emerson Electric for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 48 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of signals feels mixed for you, now is a good time to look through the underlying data, pressure test the narratives, and weigh up the 4 key rewards and 2 important warning signs for yourself.

Looking for more investment ideas?

Before you move on, give yourself options by lining up a few fresh watchlist candidates that match the kind of risk and return profile you actually want.

- Target potential mispricings by scanning our 48 high quality undervalued stocks and see which companies currently look cheaper relative to their fundamentals.

- Prioritize resilience by checking out the 68 resilient stocks with low risk scores, focusing on businesses with lower risk scores that may suit a steadier approach.

- Hunt for future leaders early with the screener containing 26 high quality undiscovered gems, a list built to surface quality names that fewer investors are watching.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com