- LIVE QUOTES

- LEARN

- HELP

EN

Assessing SFL (NYSE:SFL) Valuation After Recent Share Price Momentum And Conflicting Fair Value Signals

Why SFL (NYSE:SFL) Is Catching Investor Attention Now

SFL (NYSE:SFL) has been drawing fresh interest after recent trading moves, with the stock showing mixed short term returns but a stronger picture over the past year and beyond.

See our latest analysis for SFL.

The recent 1 day share price return of 5.68% and 7 day share price return of 7.86% sit against a stronger backdrop, with a 30 day share price return of 9.09% and a 1 year total shareholder return of 35.64%. This suggests momentum has been building over time even with short term pullbacks.

If this kind of rebound in shipping interests you, it could be a moment to broaden your watchlist with 28 elite gold producer stocks as another potential hunting ground for ideas.

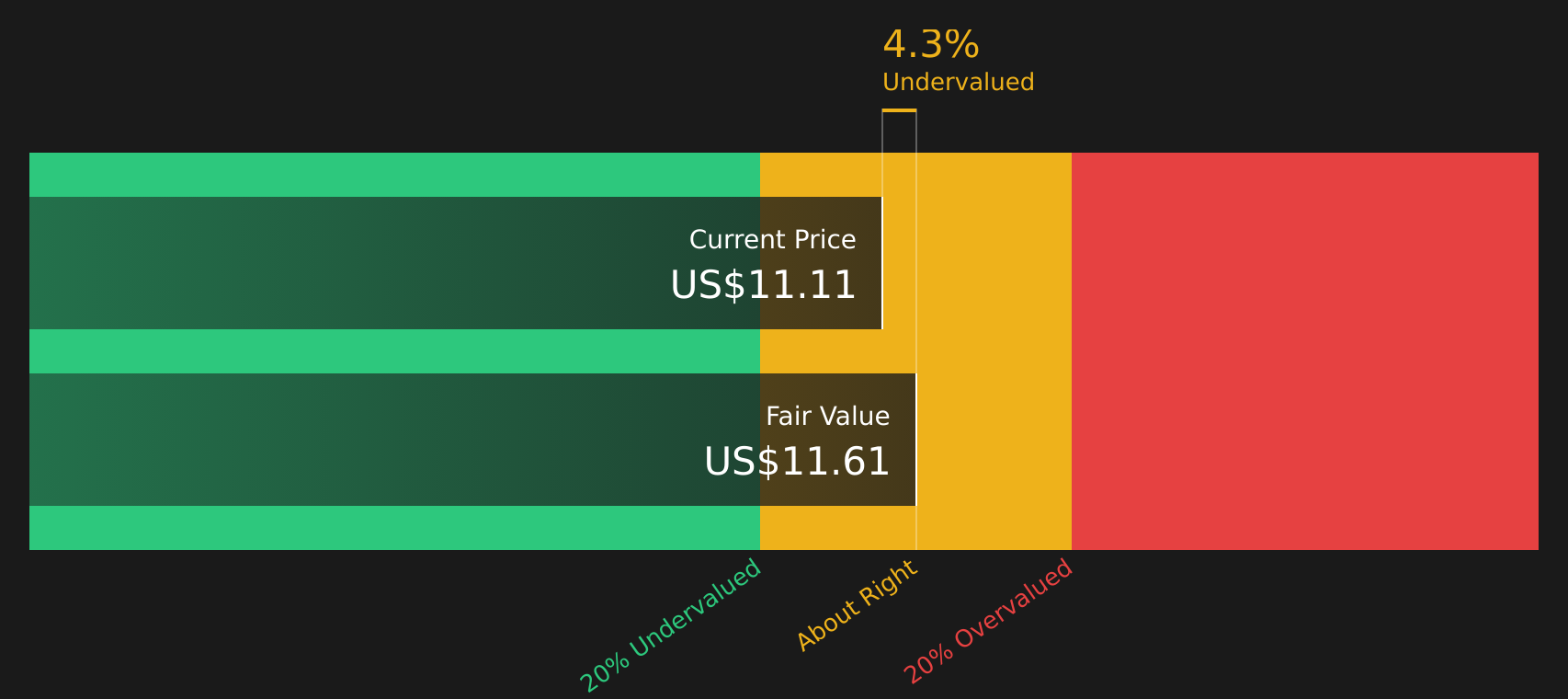

With SFL trading at $9.96 against an analyst price target of $10.55 and an estimated intrinsic discount of about 10%, the key question is whether the stock is still undervalued or whether the market is already pricing in future growth.

Most Popular Narrative: 6% Overvalued

Compared with the narrative fair value of $9.43, SFL’s last close at $9.96 sits slightly higher. The gap largely comes down to how future cash flows and capital returns are expected to play out.

With $4.2 billion in charter backlog (two-thirds with investment-grade customers) and available liquidity exceeding $300 million, SFL is positioned to capitalize on increased global trade and supply chain resilience initiatives, potentially enabling accretive asset growth and supporting future revenue expansion.

Curious how relatively flat revenue expectations, much higher margins, and a lower future earnings multiple still point to that fair value? The narrative leans heavily on recurring charters, cash flow resilience, and capital return assumptions. The full story connects these moving parts into one valuation view.

Result: Fair Value of $9.43 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there is still meaningful risk if container demand weakens or environmental compliance costs rise faster than expected. This could pressure utilization and margins.

Find out about the key risks to this SFL narrative.

Another Angle On Valuation

The narrative fair value model suggests SFL is about 6% overvalued at $9.96, but our DCF model points the other way, with a fair value of $11.07 and the shares trading at roughly a 10% discount. When two models disagree like this, which one do you lean on more?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

With sentiment in the article pointing both to opportunity and caution, it makes sense to move quickly, review the numbers yourself, and weigh up 2 key rewards and 2 important warning signs.

Ready to hunt for more ideas?

If SFL is on your radar, do not stop there. The screener can surface other opportunities that might suit your goals just as well.

- Target income first by checking out 15 dividend fortresses if you focus on steady cash distributions.

- Spot potential value plays early with 48 high quality undervalued stocks before the rest of the market pays closer attention.

- Prioritize capital protection by reviewing 68 resilient stocks with low risk scores that align with a more cautious approach.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com