- LIVE QUOTES

- LEARN

- HELP

EN

Vistance Networks (VISN) Valuation After Profitability Turnaround And High Profile Wi Fi 7 Stadium Deployment

Vistance Networks (VISN) is back in focus after reporting fourth quarter and full year 2025 results that shifted prior losses into net income and after showcasing a high profile Wi Fi 7 deployment at BMO Stadium.

See our latest analysis for Vistance Networks.

The recent move into profitability and the high profile Wi Fi 7 rollout have arrived during a softer period for the shares, with a 30 day share price return of a 7.11% decline and a 90 day share price return of a 12.36% decline. However, the 1 year total shareholder return of over 2.8x and 3 year total shareholder return of over 1.7x still point to strong longer term momentum.

If this kind of networking story has your attention, it could be a good moment to see what else is out there through our 35 AI infrastructure stocks.

With Vistance now profitable, trading at US$17.65 and carrying a value score of 4, the key question is whether the recent weakness leaves the stock mispriced or if the market is already factoring in more growth ahead.

Most Popular Narrative: 27% Undervalued

Vistance Networks' most followed narrative pegs fair value at about $24.17 a share, well above the recent $17.65 close, which sets up a clear valuation gap for investors to unpack.

The ongoing rollout of DOCSIS 4.0 amplifiers and next-gen networking products, driven by increased investments from major cable operators, positions CommScope's ANS segment to capitalize on long-term demand for higher-speed broadband and infrastructure upgrades, supporting sustained revenue growth.

Read the complete narrative. Read the complete narrative.

Curious what earnings power and margin profile sit behind that valuation gap. The narrative leans heavily on future broadband upgrades, richer software revenue and a higher earnings multiple than many investors might expect.

Result: Fair Value of $24.17 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this story can shift quickly if DOCSIS 4.0 uptake slows or key ANS customers trim spending, which could pressure revenue, margins, and that optimistic P/E profile.

Find out about the key risks to this Vistance Networks narrative.

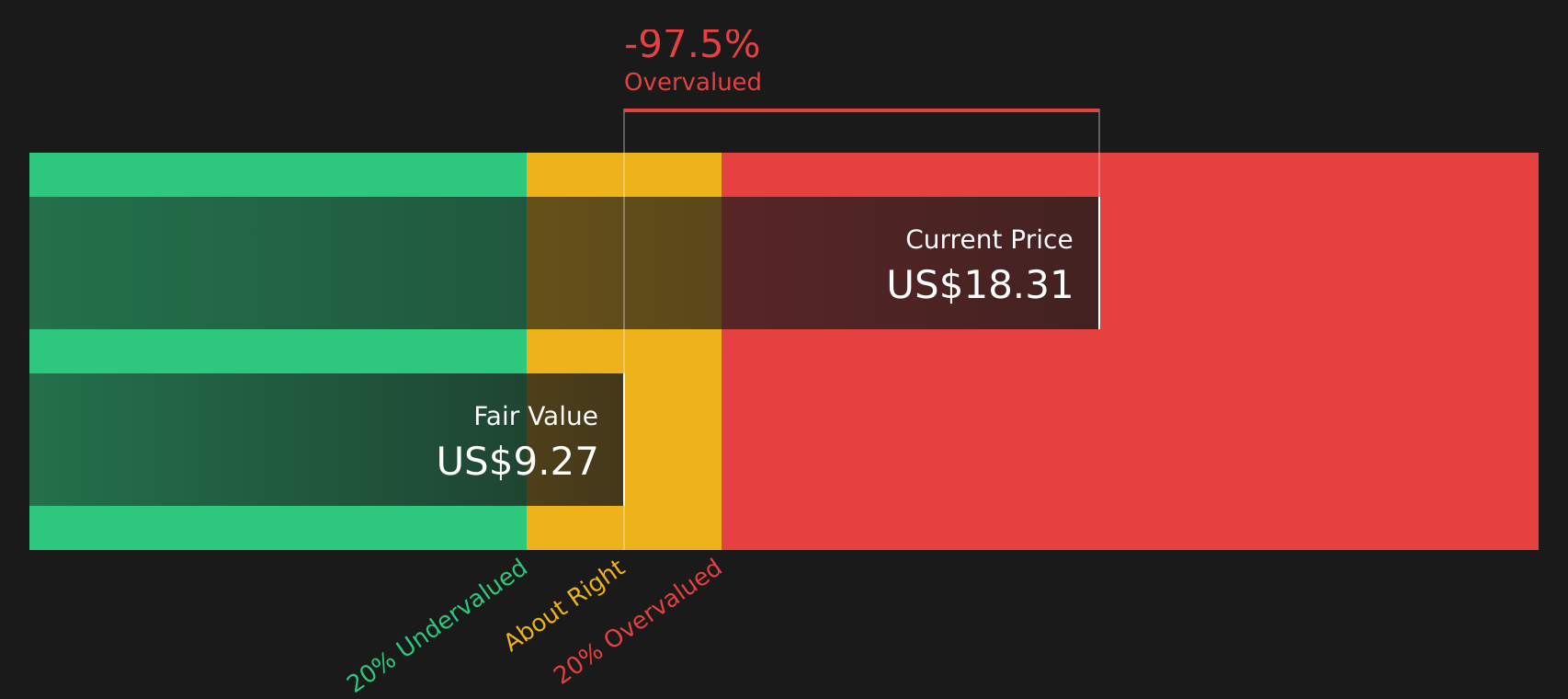

Another View: Cash Flows Point The Other Way

That $24.17 fair value comes from a narrative style model tied to earnings and multiples, but our DCF model lands in a very different place. On that approach, VISN at $17.65 is trading above an estimated future cash flow value of about $9.27, which flags potential downside if cash generation underwhelms.

So while earnings based narratives lean toward upside, the SWS DCF model highlights the risk that current expectations already lean too optimistic. Which of those two anchors do you trust more when the story around broadband upgrades or Wi Fi 7 adoption changes pace?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Vistance Networks for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 48 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals across earnings, cash flows and recent returns, do you feel that optimism or caution is stronger here, and are you ready to move quickly and weigh the trade off yourself using the 4 key rewards and 3 important warning signs?

Ready to uncover more investment ideas?

If you stop with just one stock, you risk missing other opportunities that might suit you even better, so keep your options open and keep comparing.

- Spot potential value candidates early by scanning our 48 high quality undervalued stocks that pair quality fundamentals with pricing that could appeal to disciplined investors.

- Prioritize resilience and sleep a little easier by reviewing the 68 resilient stocks with low risk scores focused on companies with lower overall risk scores.

- Hunt for under the radar opportunities by checking the screener containing 23 high quality undiscovered gems built around companies with strong fundamentals that are not widely followed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com