- LIVE QUOTES

- LEARN

- HELP

EN

Assessing Viasat (VSAT) Valuation After A Powerful One Year Share Price Surge

Viasat’s recent performance snapshot

Viasat (VSAT) has drawn fresh investor attention after recent trading, with the stock last closing at $46.31. The company operates in satellite broadband, in-flight connectivity, and government communications services.

Over the past month, Viasat has delivered an 11.06% return, while the past 3 months show a 24.19% gain, and the 1 year total return is 279.9%. Year to date, the stock is up 23.07%.

See our latest analysis for Viasat.

Viasat’s recent share price strength, including a 30 day share price return of 11.06% and a year to date share price return of 23.07%, sits alongside a very large 1 year total shareholder return. This indicates that momentum has been building rather than fading.

If Viasat’s move has you thinking about where satellite and connectivity demand might intersect with AI infrastructure, take a look at our screener of 35 AI infrastructure stocks for potential ideas beyond this single stock.

With Viasat trading near its analyst price target yet sitting on an estimated 34% intrinsic discount, the real question is whether the recent surge still leaves upside on the table or if markets are already pricing in future growth.

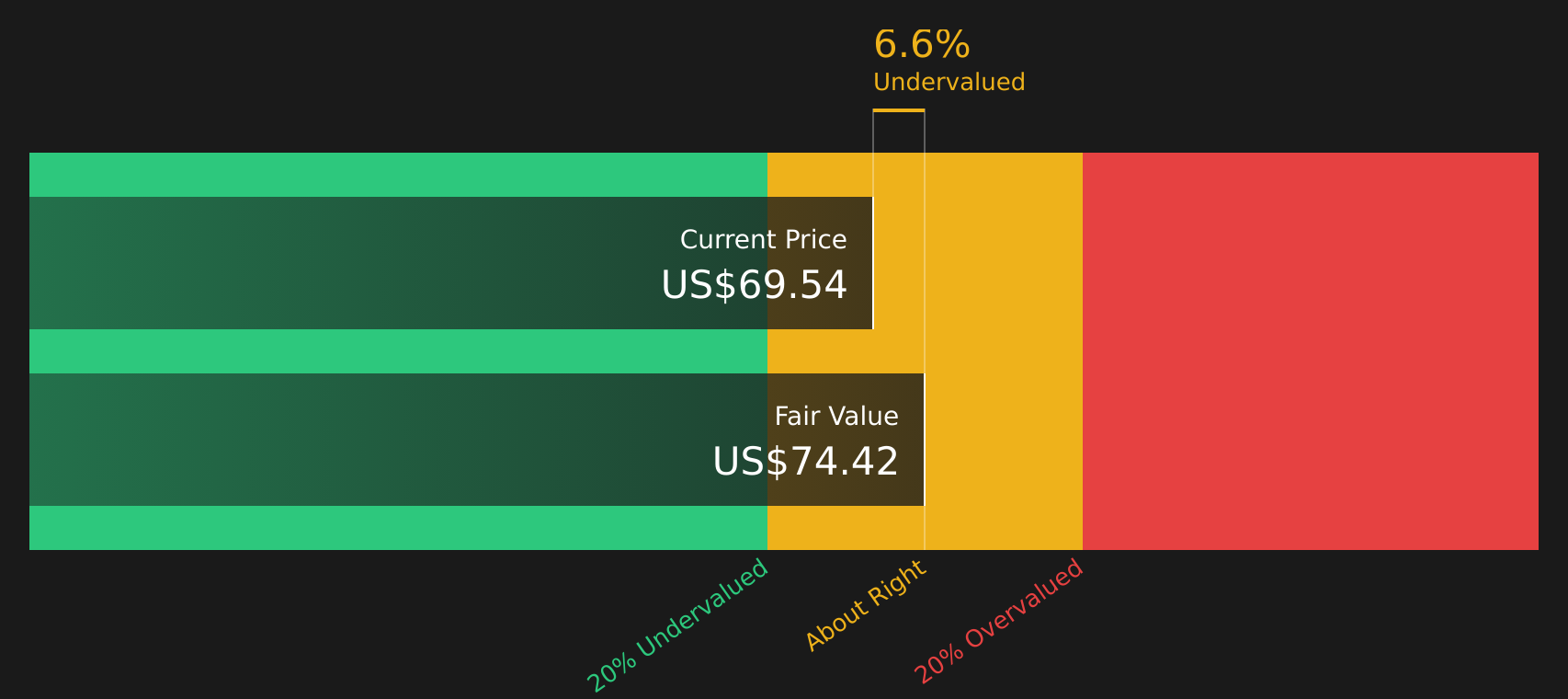

Most Popular Narrative: 12.6% Overvalued

The most followed fair value narrative for Viasat places fair value at $41.13, below the last close of $46.31, which suggests a cautious valuation gap.

The analysts have a consensus price target of $24.286 for Viasat based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $52.0, and the most bearish reporting a price target of just $10.0.

Want to see why this fair value sits above some targets yet below the market price, and how revenue, margins, and future multiples all interact to get there?

Result: Fair Value of $41.13 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you still have to weigh the heavy ViaSat 3 and Inmarsat capital spending, along with rising competition from rivals like Starlink and Project Kuiper, which could pressure returns.

Find out about the key risks to this Viasat narrative.

Another angle on Viasat’s valuation

While the fair value narrative suggests Viasat is 12.6% overvalued at $46.31 versus a $41.13 estimate, our DCF model points the other way, with a future cash flow value of $70.06. That is a 33.9% gap. Which lens do you trust more right now?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

If this mix of cautious and optimistic signals feels like a lot to weigh, review the underlying data yourself and move quickly to shape your own view with 2 key rewards and 3 important warning signs.

Looking for more investment ideas?

Do not stop at one stock. Broaden your watchlist with focused ideas that match how you like to invest and what risks you are comfortable with.

- Target potential mispricings by scanning companies our research flags as 48 high quality undervalued stocks and see which ones line up with your own view.

- Anchor your portfolio around income by checking out 14 dividend fortresses, featuring companies offering higher dividend yields with supporting fundamentals.

- Prioritise resilience by reviewing 68 resilient stocks with low risk scores, where the emphasis is on businesses with lower overall risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com