- LIVE QUOTES

- LEARN

- HELP

EN

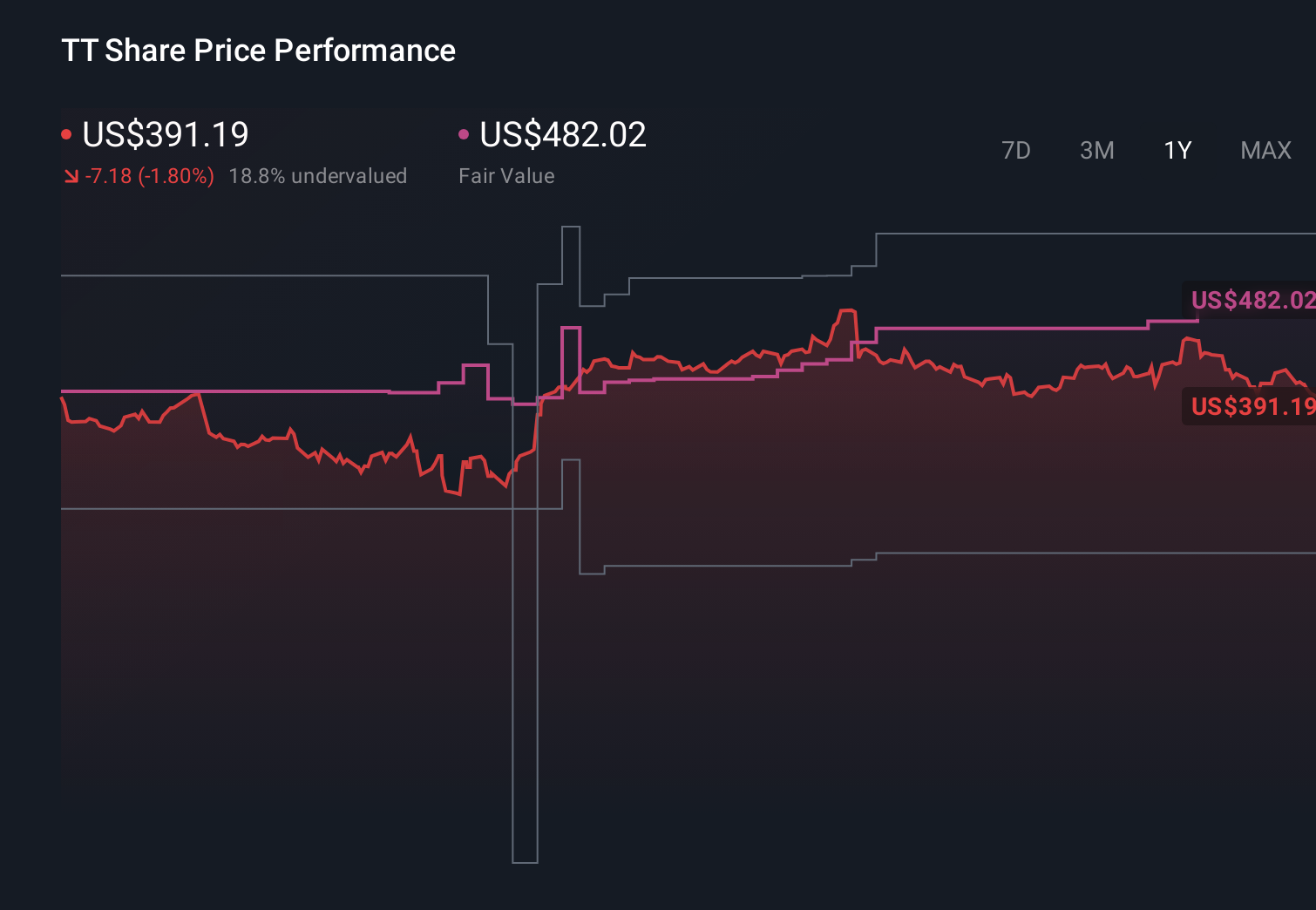

Trane Technologies (TT) Is Down 8.3% After Insider Sale And Premium Valuation Jitters Has The Bull Case Changed?

- In recent days, Trane Technologies faced pressure after going ex-dividend amid concerns that its shares are trading at a premium to industry peers, while an executive’s share sale added to questions about near-term confidence.

- At the same time, the company advanced its sustainability agenda with new climate-smart cooling programs in India and Africa and launched an energy-efficient chiller tailored for Asia Pacific data centers, underscoring its push into high-demand, lower-emission cooling solutions.

- We’ll now examine how insider selling, alongside Trane’s expanding sustainable cooling offerings, may reshape the existing investment narrative on the company.

AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Trane Technologies Investment Narrative Recap

To own Trane Technologies, you need to believe in its ability to convert demand for energy efficient, lower emission HVAC into durable earnings, despite premium valuation concerns. The latest pullback after going ex dividend and worries about insider selling chiefly highlight near term sentiment risk rather than a clear change to core fundamentals. For now, the bigger swing factor is whether key end markets like data centers and commercial projects keep supporting backlog and pricing, while Transport weakness remains a drag.

Among recent news, the launch of the HSAG air cooled magnetic bearing chiller for Asia Pacific data centers stands out. It reinforces Trane’s exposure to mission critical cooling, where efficiency and reliability are essential and regulation is tightening. For investors focused on catalysts, this type of product development ties directly to the current debate around valuation, because it shows how much of Trane’s growth story is tied to higher value, sustainability focused solutions rather than legacy HVAC volumes.

Yet beneath Trane’s growth story, investors should be aware of how premium pricing and insider selling could interact if data center or commercial demand were to soften...

Read the full narrative on Trane Technologies (it's free!)

Trane Technologies' narrative projects $25.4 billion revenue and $3.7 billion earnings by 2028. This requires 6.9% yearly revenue growth and a roughly $0.8 billion earnings increase from $2.9 billion today.

Uncover how Trane Technologies' forecasts yield a $479.73 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts take a far more cautious view than the consensus. They were assuming only about 6.5 percent annual revenue growth to roughly US$25.1 billion and earnings of about US$3.7 billion by 2028, which is much less enthusiastic than the base case. If you are weighing the recent valuation concerns and insider sale against data center and sustainability tailwinds, it is worth seeing how these more pessimistic expectations might shift after this news.

Explore 4 other fair value estimates on Trane Technologies - why the stock might be worth 11% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Trane Technologies research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Trane Technologies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Trane Technologies' overall financial health at a glance.

Interested In Other Possibilities?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Invest in the nuclear renaissance through our list of 85 elite nuclear energy infrastructure plays powering the global AI revolution.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 19 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Uncover the next big thing with 28 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com