- LIVE QUOTES

- LEARN

- HELP

EN

Pediatrix’s Profit Return And Heavy Buybacks Could Be A Game Changer For Pediatrix Medical Group (MD)

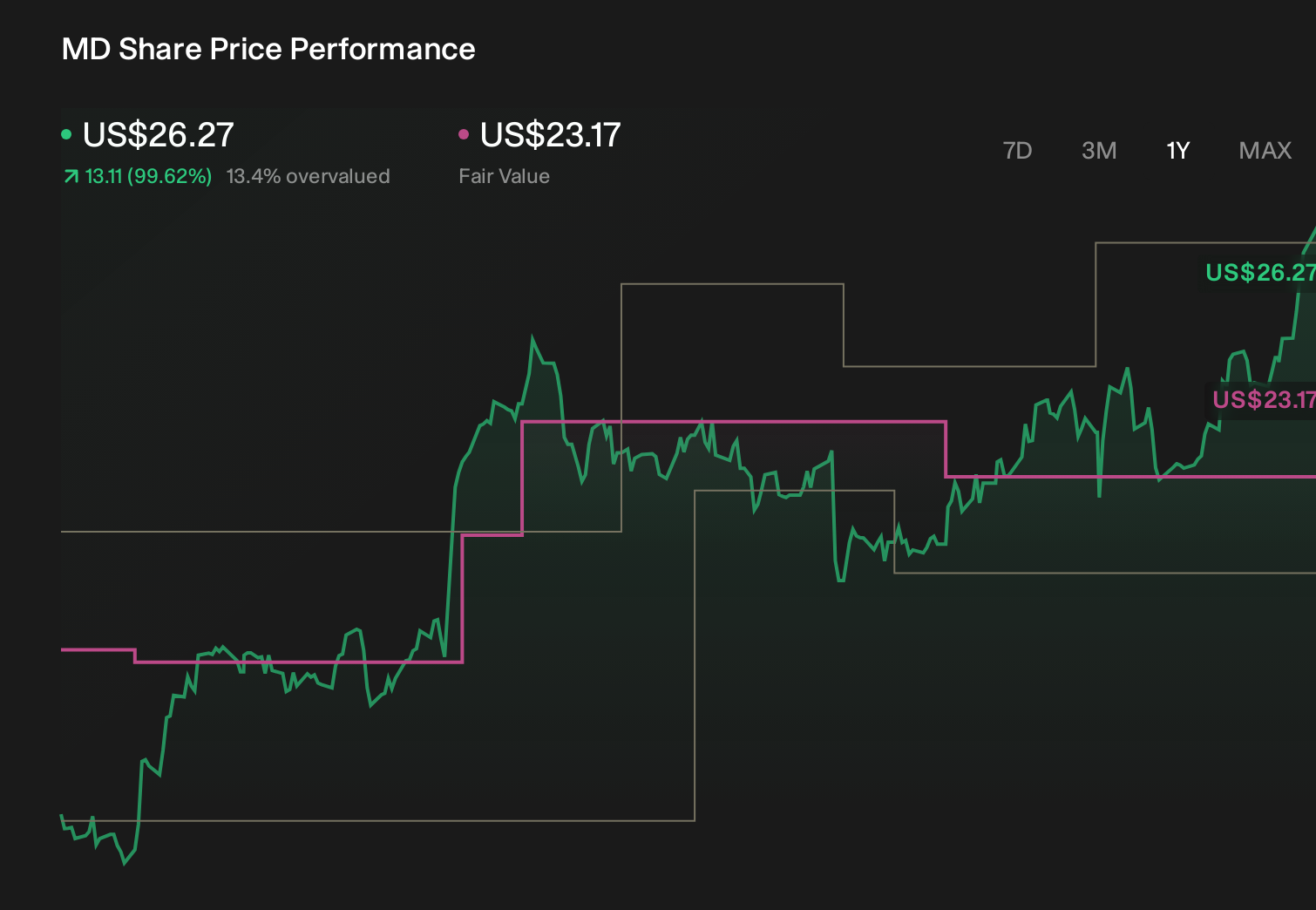

- Pediatrix Medical Group, Inc. recently reported its fourth-quarter and full-year 2025 results, with quarterly sales of US$493.77 million and net income of US$33.68 million, alongside full-year sales of US$1.91 billion and net income of US$165.39 million.

- Alongside this profit recovery, Pediatrix completed several long-running share repurchase programs totaling hundreds of millions of US dollars, while also continuing its clinical leadership with the 47th NEO: The Conference for Neonatology held in Las Vegas in February 2026.

- We’ll now examine how Pediatrix’s return to annual profitability and completion of sizeable buybacks may influence its existing investment narrative.

Find 47 companies with promising cash flow potential yet trading below their fair value.

Pediatrix Medical Group Investment Narrative Recap

To own Pediatrix, you need to believe in sustained demand for high-acuity neonatal and pediatric care and the company’s ability to protect margins despite payer and labor pressures. The latest results confirm a return to profitability, but also show year-on-year revenue softness, so they do not remove the key short term risk around potential revenue contraction from portfolio restructuring and reimbursement pressure, nor do they clearly introduce a new, near term catalyst beyond improved earnings visibility.

The completion of multiple share repurchase programs, including the August 18, 2025 plan that retired 4,003,832 shares for US$83.01 million, is the most directly relevant update. Combined with the shift from a US$99.07 million loss in 2024 to US$165.39 million in net income for 2025, these buybacks may matter for investors focused on per share earnings trends and how much financial flexibility Pediatrix retains if reimbursement, hospital fee growth, or staffing costs become more challenging.

Yet beneath the recovery in earnings, investors should be aware that rising salary and staffing pressures could still...

Read the full narrative on Pediatrix Medical Group (it's free!)

Pediatrix Medical Group's narrative projects $2.1 billion revenue and $145.1 million earnings by 2028. This requires 2.5% yearly revenue growth and a $35.2 million earnings increase from $109.9 million.

Uncover how Pediatrix Medical Group's forecasts yield a $22.67 fair value, a 14% upside to its current price.

Exploring Other Perspectives

The bullish analysts were expecting revenue to reach about US$2.2 billion and earnings of roughly US$159 million, which is a more optimistic view than the baseline. Their outlook leans heavily on stronger pricing power and higher NICU volumes, while the alternate risk you just saw highlights how shifts toward value based care could cut into that story. With Pediatrix’s new 2025 results now out, it will be important to see whether either narrative still fits or needs to be revised.

Explore 4 other fair value estimates on Pediatrix Medical Group - why the stock might be worth less than half the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Pediatrix Medical Group research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Pediatrix Medical Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Pediatrix Medical Group's overall financial health at a glance.

Interested In Other Possibilities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- We've uncovered the 14 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Invest in the nuclear renaissance through our list of 85 elite nuclear energy infrastructure plays powering the global AI revolution.

- Outshine the giants: these 22 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com