- LIVE QUOTES

- LEARN

- HELP

EN

Ultra Clean Holdings (UCTT) Valuation Check After Zero Coupon Notes Offering And Share Repurchase Plan

Ultra Clean Holdings (UCTT) is back in focus after completing a US$525 million zero coupon senior unsecured notes offering, paired with a Board-approved share repurchase plan of up to US$40 million.

See our latest analysis for Ultra Clean Holdings.

Despite the recent 5.73% 1 day share price decline and 17.18% 7 day share price pullback, Ultra Clean’s 36.45% 30 day and 118.16% year to date share price returns, alongside a 150.74% 1 year total shareholder return, point to strong momentum. The fresh zero coupon notes and buyback announcement may now be reframing this in terms of risk and capital allocation.

If you are reassessing semiconductor exposure after this move, it could be a good moment to scan other chip related names using our 34 AI infrastructure stocks as potential next ideas to research.

So, with a US$59.60 share price, a very large intrinsic value discount figure, and a 36% gap to the average analyst target still on the table, is UCTT now a mispriced opportunity, or are markets already baking in future growth?

Most Popular Narrative: 53.8% Overvalued

The most followed narrative places Ultra Clean Holdings’ fair value at $38.75, well below the recent $59.60 close. As a result, the zero coupon notes and buyback sit against a valuation framework that already assumes a lot of future execution.

Analysts have raised their price target on Ultra Clean Holdings by $15, based on updated assumptions regarding discount rates, long-term revenue growth, profit margins, and future P/E expectations that together support a higher valuation framework.

Bullish analysts see the higher price target as a reflection of updated modeling around revenue growth, profitability, and the P/E multiple that investors may be willing to pay for Ultra Clean Holdings over time.

Want to see what kind of revenue ramp, margin rebuild, and future earnings multiple are baked into that fair value math and target reset? The full narrative spells out a detailed earnings path, the assumed profitability pivot, and the valuation multiple that needs to hold up if today’s price is to be supported.

Result: Fair Value of $38.75 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the heavy reliance on a few large customers and ongoing tariff related cost pressure could quickly challenge that fair value story if orders or margins disappoint.

Find out about the key risks to this Ultra Clean Holdings narrative.

Another Angle on Valuation

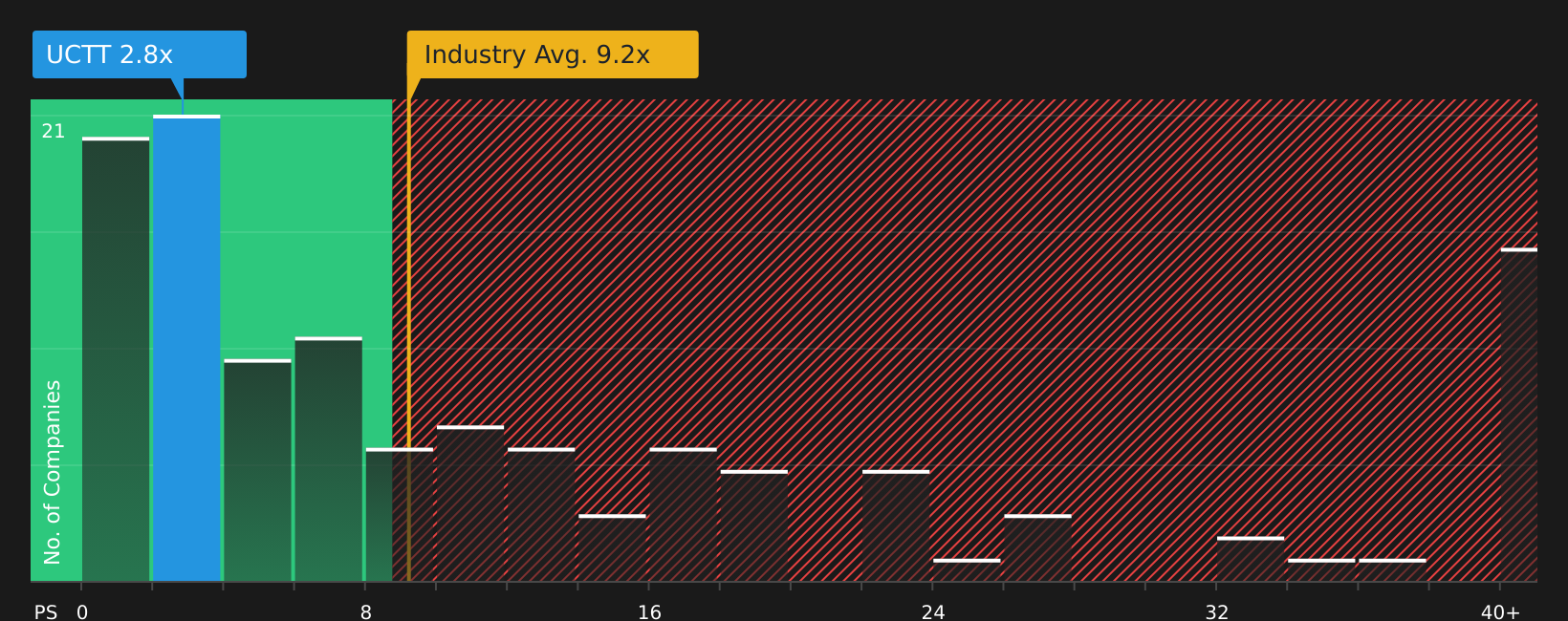

While the narrative fair value of $38.75 flags Ultra Clean as overvalued, the P/S picture tells a different story. At 1.3x sales, the stock is far below the US Semiconductor industry on 6.1x and peers on 8.4x, and even below a 2x fair ratio. Is the market being too harsh, or is it just pricing in the risks?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this mix of strong recent returns and valuation questions leaves you unsure, it may be worth taking time now to review the overall balance of risks and potential upsides, starting with 2 key rewards and 1 important warning sign.

Ready to hunt for your next idea?

If this update has sharpened your thinking on UCTT, do not stop here. Widen your watchlist now so you are not relying on a single story.

- Spot potential value opportunities early by scanning our 49 high quality undervalued stocks and see which names currently trade below their assessed worth.

- Prioritise resilience by checking companies in the 75 resilient stocks with low risk scores that score well on risk metrics and balance sheet strength.

- Get ahead of the crowd by researching our screener containing 24 high quality undiscovered gems, a set of under the radar ideas with solid fundamentals to investigate next.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com