- LIVE QUOTES

- LEARN

- HELP

EN

Is Helix’s 2025 Earnings Miss and Impairment Reshaping the Investment Case For Helix (HLX)?

- Helix Energy Solutions Group, Inc. recently reported fourth-quarter and full-year 2025 results showing lower sales and net income year-on-year, alongside a US$18,064,000 long-lived asset impairment and completion of a US$71.49 million share repurchase program that retired 9,094,398 shares since February 2023.

- As the company now evaluates acquisition opportunities and broader capital deployment, investors may weigh the tension between weaker recent performance and management’s appetite for inorganic growth.

- We’ll now examine how Helix’s softer 2025 earnings, including the long-lived asset impairment, may affect the previously outlined investment narrative.

Uncover the next big thing with 30 elite penny stocks that balance risk and reward.

Helix Energy Solutions Group Investment Narrative Recap

To own Helix Energy Solutions Group, you need to be comfortable with a project-driven offshore services business where contract backlog and utilization are key, but also volatile. The latest 2025 results, weaker year-on-year and hit by a US$18.06 million impairment, reinforce that earnings can swing when assets are underutilized. Near term, the main catalyst is converting existing contract wins into steadier margins, while the biggest risk remains further project deferrals that leave vessels idle. This news does not fundamentally change that risk profile, but it does highlight it.

The most relevant recent announcement here is Helix’s completion of its US$71.49 million share repurchase program, which retired about 5.99% of shares since February 2023. Combined with management’s current focus on potential acquisitions and broader capital deployment, this underlines a shift from purely defensive balance sheet moves toward more active use of capital at a time when earnings softness and impairments are reminding investors how dependent returns still are on project timing and pricing.

Yet beneath the capital deployment story, investors should be aware that prolonged project delays and underused assets could still...

Read the full narrative on Helix Energy Solutions Group (it's free!)

Helix Energy Solutions Group's narrative projects $1.4 billion revenue and $103.0 million earnings by 2028. This requires 2.9% yearly revenue growth and a $52.9 million earnings increase from $50.1 million today.

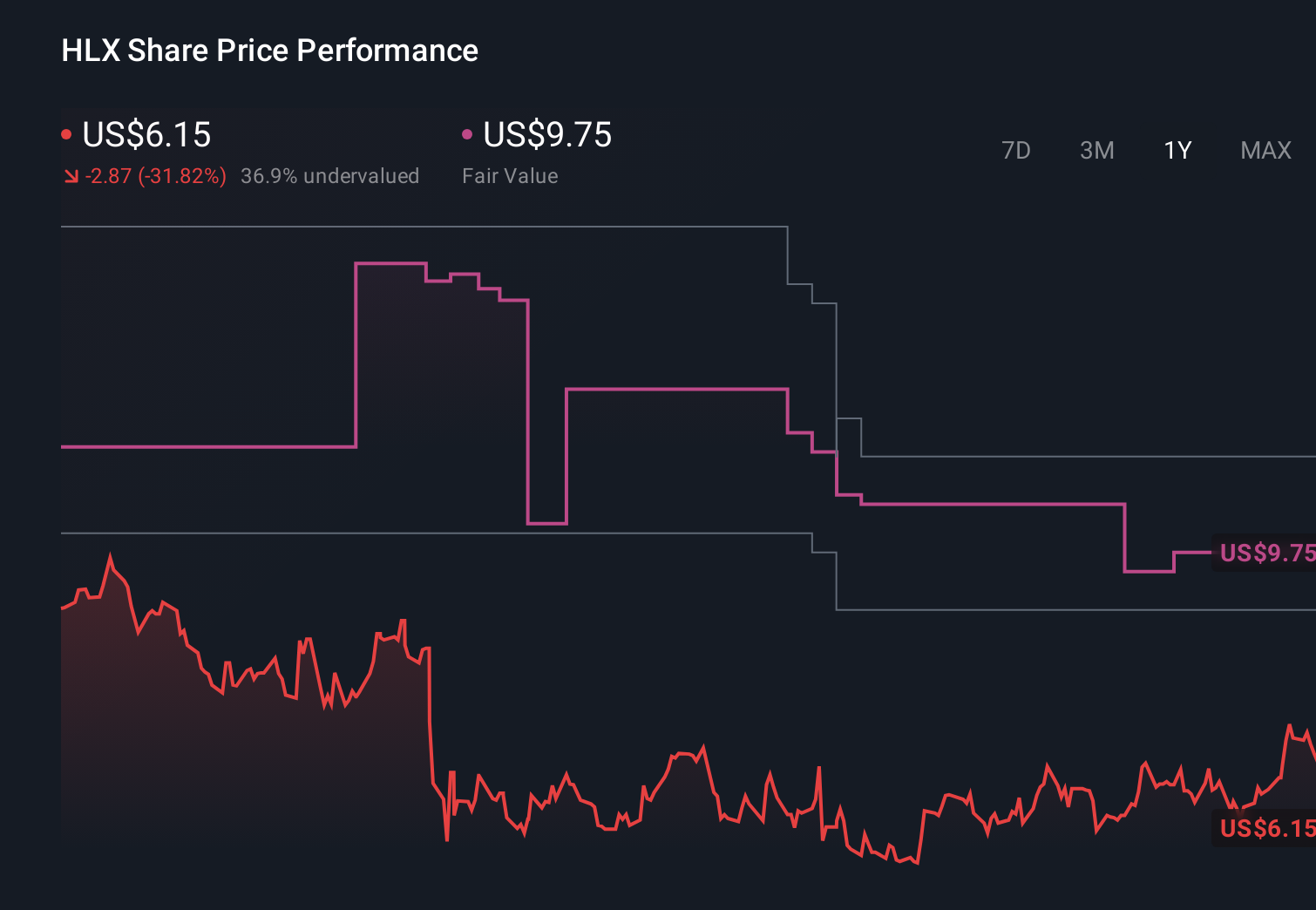

Uncover how Helix Energy Solutions Group's forecasts yield a $9.75 fair value, a 5% upside to its current price.

Exploring Other Perspectives

Some of the lowest-estimate analysts took a more cautious view, even before this news, assuming revenue of about US$1.4 billion and earnings near US$114 million by 2028, which is far less generous than consensus. When you set that against the recent impairment and margin pressure, you can see how their more pessimistic expectations around delayed projects and thinner margins might gain traction, and why it makes sense for you to compare several viewpoints before deciding what feels realistic.

Explore 4 other fair value estimates on Helix Energy Solutions Group - why the stock might be worth as much as 67% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Helix Energy Solutions Group research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Helix Energy Solutions Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Helix Energy Solutions Group's overall financial health at a glance.

Searching For A Fresh Perspective?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 22 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

- Capitalize on the AI infrastructure supercycle with our selection of the 34 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com