- LIVE QUOTES

- LEARN

- HELP

EN

Assessing Vistance Networks (VISN) Valuation After 2025 Results And Connectivity And Cable Solutions Sale

Vistance Networks (VISN) drew fresh attention after reporting 2025 results that included very large net income and a move from loss to profit, supported by the sale of its Connectivity and Cable Solutions segment.

See our latest analysis for Vistance Networks.

The share price reaction has been mixed, with a 1 day share price return of 1.59% after the results, a 90 day share price return showing an 8.51% decline, and a 1 year total shareholder return of very large magnitude that reflects how much sentiment shifted as the CCS sale, debt repayment and planned cash distribution came into focus.

If you are looking for ideas beyond Vistance, this could be a useful moment to see which AI infrastructure names are on investors' radars through our 34 AI infrastructure stocks.

With the stock at $17.85, a very large 1 year return behind it and a special cash distribution of at least $10 per share on the way, you have to ask: is there still an opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 26.1% Undervalued

Vistance Networks' most followed valuation narrative pegs fair value at about $24.17, which sits meaningfully above the recent $17.85 share price and reflects a very specific set of long term assumptions.

The completed sale of the CCS business is set to eliminate company debt and preferred equity, reduce interest expense, and free up significant excess cash for shareholder returns, directly improving net earnings and the company's capital structure resilience.

Want to see what justifies that higher fair value? The narrative leans heavily on future revenue trends, a step up in profit margins, and a richer earnings multiple that assumes investors will pay more for each dollar of profit down the road.

Result: Fair Value of $24.17 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you also have to weigh the risk that ANS and RUCKUS, which rely on project driven, cyclical spending and concentrated cable customers, may deliver more volatile revenue and margins than assumed.

Find out about the key risks to this Vistance Networks narrative.

Another View: Multiples Send A Mixed Signal

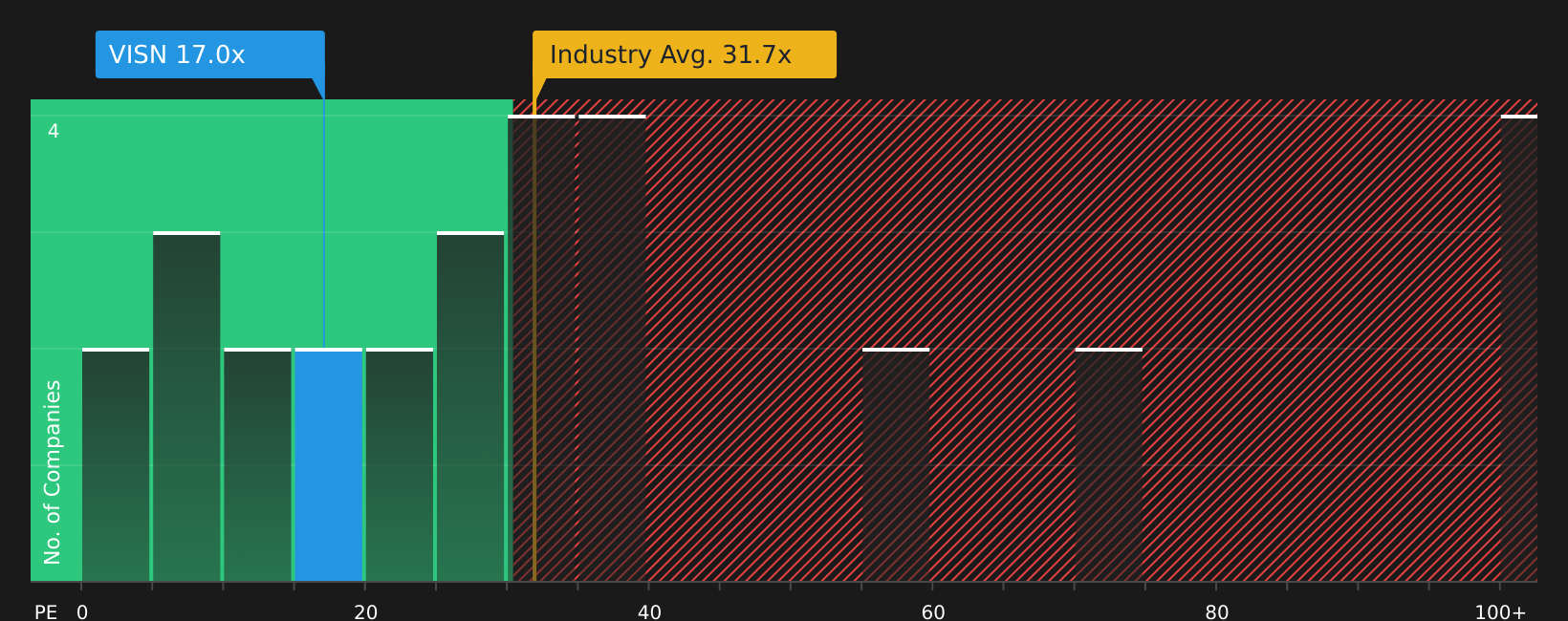

That 26.1% gap to a $24.17 fair value is one story, but the P/E numbers tell another. Vistance trades on a 15.8x P/E, lower than the US Communications industry at 43.3x and peers at 71x, yet only a touch above its 15.7x fair ratio, which suggests limited room for error.

Put simply, the market is pricing Vistance cheaper than many sector names but close to where our fair ratio says it could settle. The key question for you is whether the post CCS business mix justifies that small premium or calls for a wider discount.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Does this mix of optimism and concern match how you see Vistance right now, or does it feel off? Take a close look at the full risk and reward balance for yourself with 3 key rewards and 3 important warning signs.

Ready for more investment ideas?

If Vistance has sharpened your thinking, do not stop here. Use this momentum to size up other opportunities that might fit your style and risk tolerance.

- Target value first and hunt for quality companies trading below what our models suggest with the 45 high quality undervalued stocks that filters for strong fundamentals at appealing prices.

- Prioritise resilience and check out the solid balance sheet and fundamentals stocks screener (41 results) to focus on businesses with financial positions that may better handle shocks and funding needs.

- Spot potential early movers by scanning the screener containing 24 high quality undiscovered gems where smaller, less followed names with solid metrics sit before wider attention arrives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com