- LIVE QUOTES

- LEARN

- HELP

EN

A Look At Empire State Realty Trust’s Valuation After Earnings, New Leases And Buybacks

Why Empire State Realty Trust is back on investors’ radar

Empire State Realty Trust (ESRT) has moved back into focus after fourth quarter 2025 results showed higher quarterly revenue and net income year over year, alongside fresh leasing wins with major tenants.

For the fourth quarter, ESRT reported sales of US$159.72 million and revenue of US$199.22 million, compared with US$155.13 million and US$197.6 million a year earlier. Net income came in at US$20.73 million versus US$12.22 million, with basic and diluted earnings per share from continuing operations at US$0.12 compared with US$0.07.

Over the full year 2025, sales were US$626.21 million and revenue was US$768.27 million, compared with US$614.6 million and US$767.92 million in 2024. Net income for the year was US$47.6 million versus US$51.64 million, while basic EPS from continuing operations was US$0.26 compared with US$0.29, and diluted EPS was US$0.25 versus US$0.28.

Around the results, ESRT highlighted a series of long term lease commitments that help illustrate ongoing tenant demand across its New York portfolio. Burlington Stores expanded by a full floor of 35,629 square feet and renewed early on 170,763 square feet at 1400 Broadway, bringing its total footprint there to 206,392 square feet, its fourth expansion with the company since 2010. Nespresso renewed its 41,835 square foot space at 111 W. 33 Street, and separate announcements covered renewals with TJ Maxx for 46,437 square feet at 250 W. 57 Street and JP Morgan Chase Bank for 21,683 square feet at One Grand Central Place.

ESRT also reported progress on capital returns. From December 5 to December 31, 2025, the company repurchased 891,530 shares, representing 0.52% of shares, for US$6 million, completing the buyback tranche announced on December 5, 2025.

See our latest analysis for Empire State Realty Trust.

Even with the recent earnings update, long term leases and continued dividends, ESRT’s share price has been under pressure. The 30 day share price return is 11.31%, and the 1 year total shareholder return shows a 32.89% decline, pointing to fading momentum despite ongoing operational activity and capital returns such as buybacks.

If this has you rethinking where real estate fits in your portfolio, it could be a good moment to broaden your search and check out 19 top founder-led companies as potential alternatives.

With ESRT shares under pressure over 1, 3 and 5 years but trading below some analyst targets and intrinsic estimates, should you view today’s price as a discount, or assume the market already sees the company’s future growth?

Most Popular Narrative: 20.1% Undervalued

At $5.88, Empire State Realty Trust is trading below the most followed narrative fair value of $7.36, which reflects detailed assumptions about future cash flows and risk.

Ongoing portfolio modernization and leadership in sustainability and energy efficiency strengthens ESRT's competitive position, enabling premium rents, attracting high-quality tenants, and supporting net margin expansion as tenants increasingly seek sustainable space and as operating costs are optimized.

Curious what justifies that higher fair value? The narrative leans on modest revenue growth, thinner margins, and a future earnings multiple that might surprise office REIT watchers.

Result: Fair Value of $7.36 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the story could change if tourism driven Observatory income weakens again, or if rising operating costs continue to run ahead of ESRT’s revenue growth.

Find out about the key risks to this Empire State Realty Trust narrative.

Another way to look at ESRT’s valuation

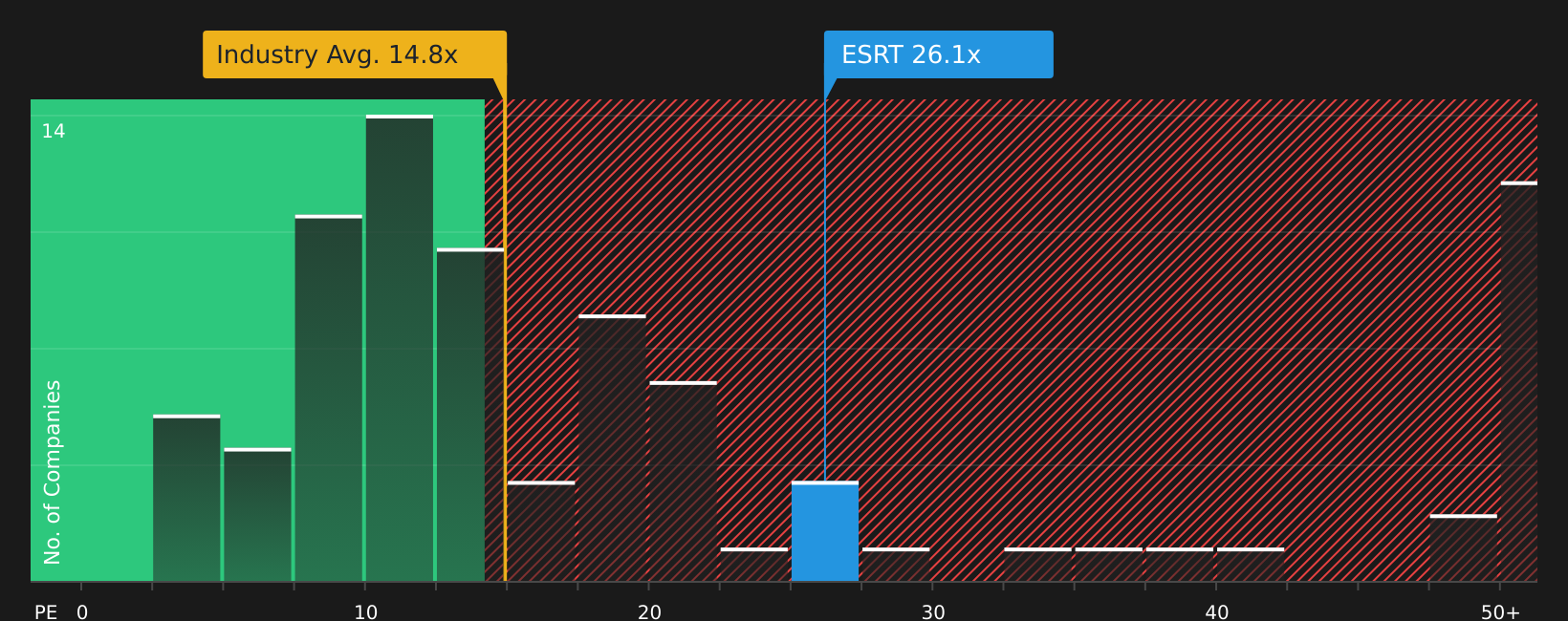

The narrative fair value of $7.36 paints ESRT as 20.1% undervalued, but the P/E picture is less forgiving. At 23.1x earnings, the shares sit above the estimated fair ratio of 14.4x and above the global Office REITs average of 17.3x, while still below a 59.7x peer average. Is that a cushion or a warning sign for you?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Mixed signals or clear opportunity, the data cuts both ways and time matters if you care about price. Take a closer look at the balance of 2 key rewards and 4 important warning signs before you decide where you stand.

Looking for more investment ideas?

If ESRT has you rethinking your next move, do not stall here, use the Simply Wall St screener to see what else the market is offering right now.

- Target resilience first by checking companies in the 76 resilient stocks with low risk scores that may better fit your comfort with volatility and drawdowns.

- Hunt for value by scanning the 49 high quality undervalued stocks to see where our model flags a gap between current prices and underlying fundamentals.

- Focus on reliability by reviewing income ideas in the 13 dividend fortresses if consistent cash payouts are high on your priority list.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com