- LIVE QUOTES

- LEARN

- HELP

EN

Butterfly Network (BFLY) Is Up 27.2% After First Positive Operating Cash Flow And AI Platform Push – Has The Bull Case Changed?

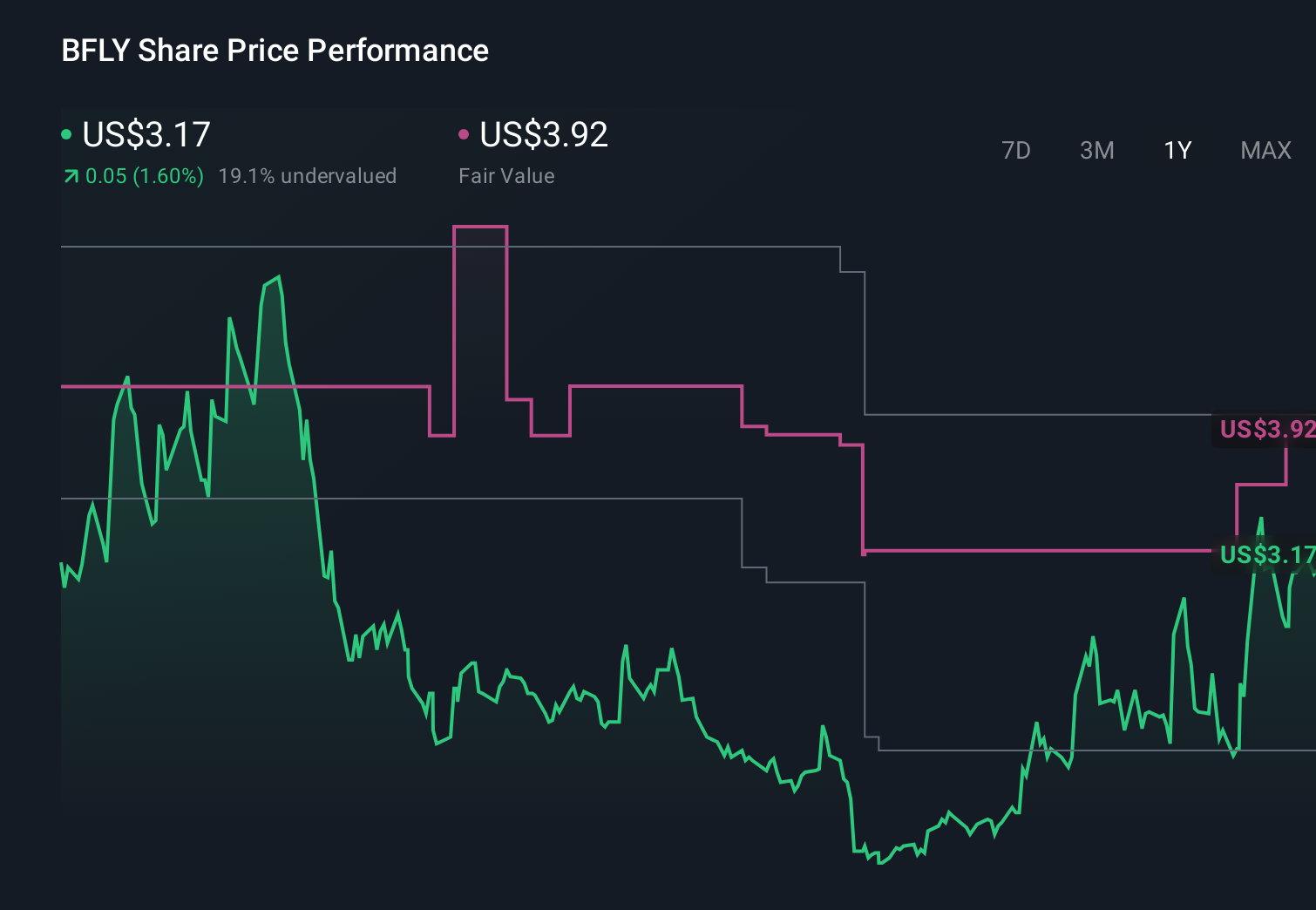

- In late February 2026, Butterfly Network, Inc. reported Q4 2025 results showing US$31.51 million in revenue versus US$22.35 million a year earlier, narrower quarterly losses, and issued 2026 revenue guidance of US$117 million to US$121 million alongside a new US$57.00 million shelf registration for ESOP-related Class A shares.

- The company’s first quarter of positive operating cash flow, boosted by its Midjourney partnership and Compass AI launch, highlights a shift toward higher-margin, platform-based ultrasound and AI offerings.

- We’ll now examine how Butterfly’s first positive operating cash flow and expanding AI platform reshape its existing investment narrative.

Find 46 companies with promising cash flow potential yet trading below their fair value.

Butterfly Network Investment Narrative Recap

To own Butterfly Network, you need to believe its shift from selling handheld ultrasound devices to monetizing an AI and semiconductor platform can eventually support a sustainable, higher-margin business. The key near term catalyst is continued traction from Compass AI and Butterfly Embedded deals, while the biggest risk is that recurring software and platform revenue does not build fast enough to offset ongoing operating losses. The latest results and guidance modestly strengthen, but do not eliminate, that risk.

The most relevant update here is Butterfly’s 2026 revenue guidance of US$117 million to US$121 million, following Q4 2025’s first quarter of positive operating cash flow. That outlook sits alongside ongoing adjusted EBITDA losses of US$21 million to US$25 million for 2026, underscoring that, despite higher Q4 revenue helped by the Midjourney partnership and expanding Compass AI pipeline, the path to consistent profitability and lower cash burn is still a central part of the story.

Yet behind the upbeat revenue guidance, investors should also be aware of the risk that recurring software margins lag and cash burn persists over time...

Read the full narrative on Butterfly Network (it's free!)

Butterfly Network’s narrative projects $135.9 million revenue and $17.0 million earnings by 2028. This requires 15.8% yearly revenue growth and a $79.8 million earnings increase from -$62.8 million today.

Uncover how Butterfly Network's forecasts yield a $5.06 fair value, a 34% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were assuming only about 14 percent annual revenue growth and no profits by 2028, so compared with consensus their view highlights how home care and AI platform traction could still disappoint, reminding you that reasonable people can look at the same Q4 cash flow upside and reach very different conclusions.

Explore 10 other fair value estimates on Butterfly Network - why the stock might be worth as much as 45% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Butterfly Network research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Butterfly Network research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Butterfly Network's overall financial health at a glance.

Searching For A Fresh Perspective?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- AI is about to change healthcare. These 27 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 31 companies in the world exploring or producing it. Find the list for free.

- The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com