- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Does Ternium’s 2025 Profit Rebound And Dividend Plan Reshape The Bull Case For TX?

- Ternium S.A. has reported its fourth-quarter and full-year 2025 results, with annual sales of US$15,609.09 million and net income of US$425.23 million, and its board intends to propose a total 2025 annual dividend of US$0.27 per share (US$2.70 per ADS), including the interim amount already paid.

- If shareholders approve the board’s plan at the May 12, 2026 meeting, investors would receive a further US$0.18 per share (US$1.80 per ADS) on May 15, 2026, highlighting how Ternium is balancing a return to profitability with sizable cash distributions of about US$530 million for the 2025 financial year.

- We’ll now consider how Ternium’s return to full-year profitability and planned US$0.27 per-share dividend proposal influence its investment narrative.

Uncover the next big thing with 30 elite penny stocks that balance risk and reward.

Ternium Investment Narrative Recap

To own Ternium, you need to believe in its role as a key steel supplier across Latin America and North America, while accepting exposure to regional demand swings and heavy investment needs. The return to profitability in 2025 and the proposed US$0.27 per share dividend are positive signals, but they do not materially change the near term focus on how higher capex and potential steel overcapacity could pressure margins and cash flows.

The most relevant announcement here is the full year 2025 earnings release, showing US$15,609.09 million in revenue and US$425.23 million in net income after a prior year loss. This recovery provides the backdrop for the proposed US$530 million dividend outlay and will likely frame how investors judge Ternium’s ability to keep funding its large capital program while maintaining shareholder distributions if pricing pressure or regional macro risks intensify.

Yet behind the dividend headlines, one key risk that investors should be aware of is how sustained global overcapacity and rising imports could...

Read the full narrative on Ternium (it's free!)

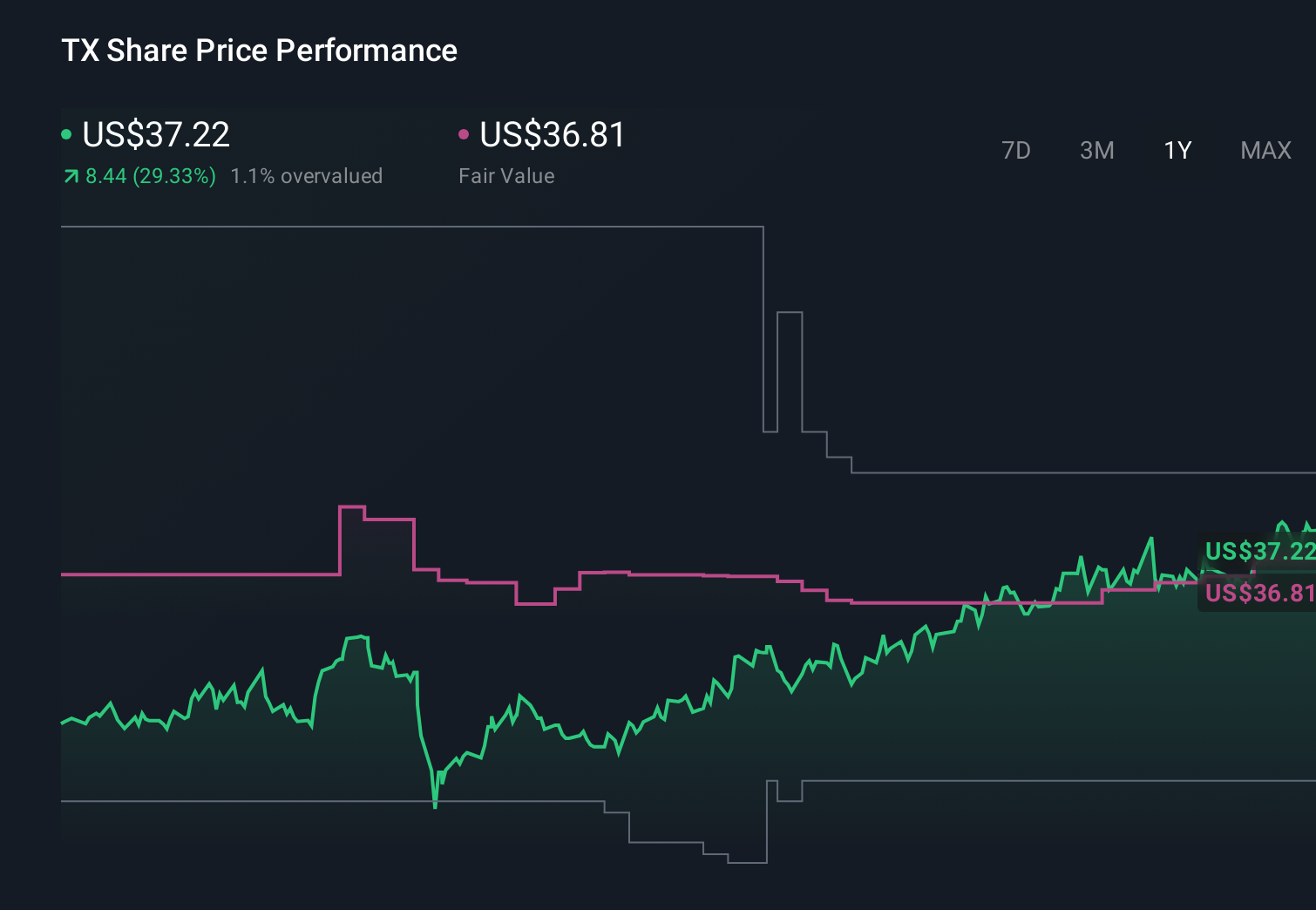

Ternium's narrative projects $18.4 billion revenue and $828.7 million earnings by 2028. This requires 4.2% yearly revenue growth and about a $233.8 million earnings increase from $594.9 million today.

Uncover how Ternium's forecasts yield a $39.88 fair value, a 8% downside to its current price.

Exploring Other Perspectives

While consensus sees improving earnings, the most pessimistic analysts were assuming revenue around US$17.2 billion and earnings near US$423.9 million by 2028, reminding you that views on Ternium’s margin pressures and regional exposure can diverge sharply and could shift again after this latest dividend and earnings news.

Explore 4 other fair value estimates on Ternium - why the stock might be worth as much as 81% more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Ternium research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Ternium research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ternium's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Capitalize on the AI infrastructure supercycle with our selection of the 33 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 30 companies in the world exploring or producing it. Find the list for free.

- We've uncovered the 15 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com