- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing W. P. Carey (WPC) Valuation After Its Latest Equity And Debt Capital Raises

Why W. P. Carey Just Raised Fresh Capital

W. P. Carey (WPC) has just completed a $432 million follow on equity offering of 6,000,000 common shares, alongside recent senior unsecured note issuances, to fund investments, repay debt, and support general corporate needs.

See our latest analysis for W. P. Carey.

Despite a small 1 day share price return of 0.52% to US$73.44, W. P. Carey’s 30 day share price return of 5.87% and year to date share price return of 13.23% suggest building momentum, while the 1 year total shareholder return of 20.80% highlights how income and price gains have combined over time.

If this kind of capital raising activity has you thinking about other income focused opportunities, it could be a good moment to broaden your search and check out 22 top founder-led companies.

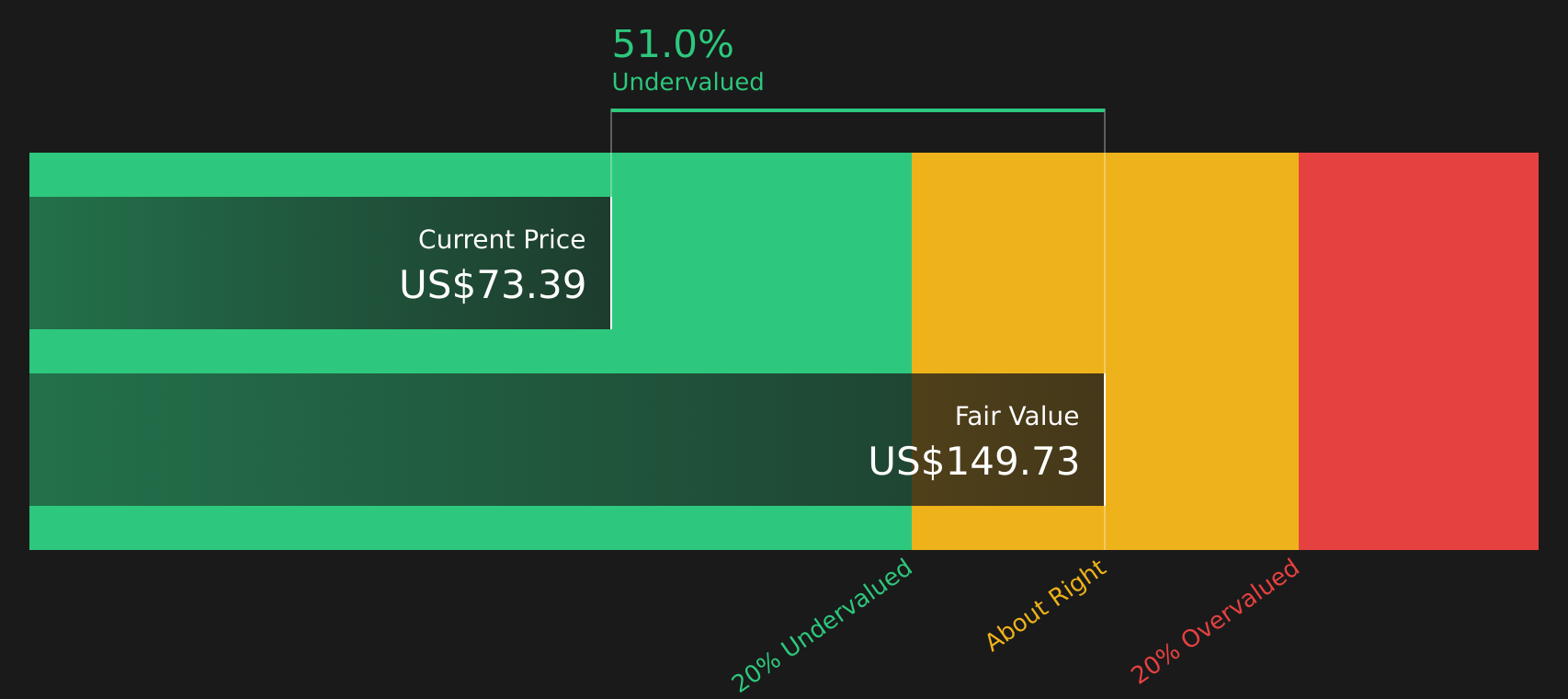

With W. P. Carey trading around US$73.44, near a recent equity offer at US$72 and showing a 51% intrinsic discount estimate, you have to ask: is this an underappreciated net lease REIT, or is the market already pricing in future growth?

Most Popular Narrative: 2.3% Overvalued

W. P. Carey closed at $73.44 compared with a widely followed fair value estimate of $71.82, a small gap that still prompts closer attention to the underlying story.

Active balance sheet management, including high spreads (100-150 bps) between disposition and investment cap rates, allows accretive reinvestment from non-core asset sales (for example, self-storage) into higher-yielding, long-term net lease assets, providing a catalyst for net margin expansion and AFFO growth.

Want to see what kind of revenue growth, margin lift and earnings profile justify that valuation gap? The most followed narrative lays out a detailed roadmap.

Result: Fair Value of $71.82 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you also have to weigh tenant concentration and reliance on property sales, because any hiccup in either area could quickly change how this story plays out.

Find out about the key risks to this W. P. Carey narrative.

Another Take On What W. P. Carey Is Worth

The earlier view framed W. P. Carey as only 2.3% above a fair value of $71.82, but our DCF model paints a different picture. On that approach, the shares at $73.44 sit about 51% below an estimated future cash flow value of $149.59, which is a wide gap for any income REIT.

With one method indicating the stock is slightly overvalued and the SWS DCF model indicating a deep discount, which lens seems more useful when real cash flows and long leases are at the center of the analysis?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out W. P. Carey for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of signals feels finely balanced, it is a good time to look through the underlying data yourself and decide what it all adds up to; you can weigh both the concerns and the upside potential by checking out 3 key rewards and 3 important warning signs.

Ready To Hunt For Your Next Idea?

If W. P. Carey has sharpened your focus, do not stop here; you could miss other ideas that fit your income, quality, or risk profile even better.

- Spot potential bargains early by scanning our screener containing 23 high quality undiscovered gems before they appear on everyone else’s radar.

- Build a sturdier core for your portfolio by focusing on companies from the solid balance sheet and fundamentals stocks screener (40 results) that pair resilient finances with fundamental strength.

- Prioritise sleep at night potential and concentrate on steadier names using the 78 resilient stocks with low risk scores to narrow your shortlist quickly.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com