- LIVE QUOTES

- LEARN

- HELP

EN

Assessing SFL Corporation (SFL) Valuation After Steady Dividend And Revenue Beat Despite Non Recurring Loss

SFL Corporation (SFL) kept its quarterly cash dividend at $0.20 per share for the 88th straight payout, even as it reported a quarterly net loss influenced by non recurring items and revenue above analyst expectations.

See our latest analysis for SFL.

SFL’s recent 1 month share price return of 29.67% and 90 day share price return of 32.84% indicate building momentum, while the 5 year total shareholder return of 120.24% shows longer term holders have already seen substantial value.

If this dividend update has you reviewing income ideas, it could be a good moment to widen your search with our screen of 27 elite gold producer stocks as another source of potential opportunities.

With SFL now near its 52-week high at US$10.84 and trading roughly in line with the latest analyst target and intrinsic value estimate, you have to ask yourself: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 15% Overvalued

SFL closed at $10.84 compared with a widely followed fair value narrative of $9.43, which frames the recent price strength in a different light.

SFL's diversified fleet structure with significant exposure to container vessels and strong, long-term charters to investment-grade counterparties provides stable recurring revenue streams, high fleet utilization (98%+), and resilience against market volatility, supporting more predictable earnings and dividend coverage.

Want to know what kind of earnings path and profit margin shift would need to sit behind that fair value call? The narrative leans heavily on changing profitability, a different revenue mix, and a future valuation multiple that does not match today's profile. Curious which assumptions really carry most of the weight in that model.

Result: Fair Value of $9.43 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are also pressure points to keep in mind, including SFL's large US$850 million capital spending commitments and its heavy reliance on the container shipping backlog.

Find out about the key risks to this SFL narrative.

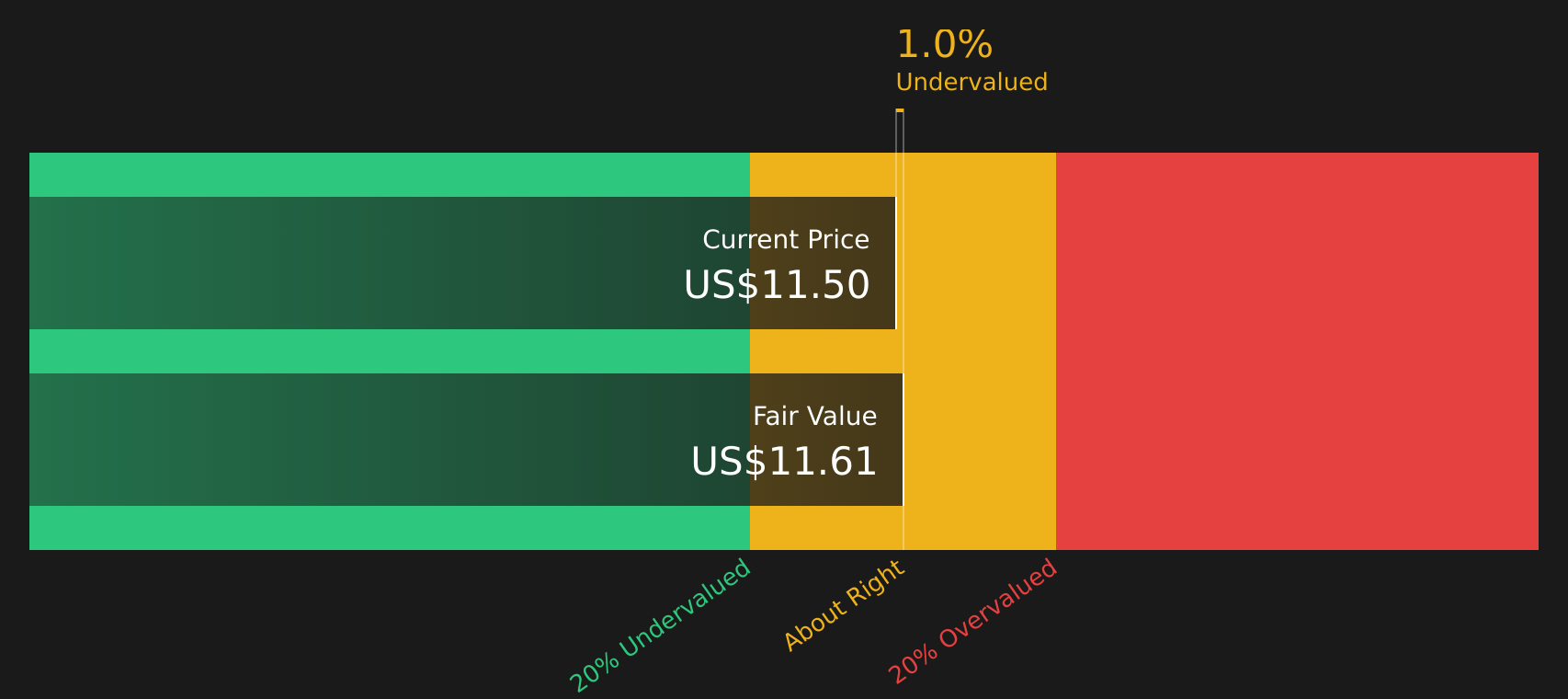

Another View: Cash Flows Point the Other Way

While the popular narrative places SFL at around 15% overvalued with a fair value of $9.43, our DCF model suggests a slightly different perspective. It indicates that SFL is trading about 2% below its fair value estimate of $11.07. Same company, two models; which one do you trust more?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out SFL for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of views has you torn, do not wait for consensus to form. Instead, check the balance of 2 key rewards and 2 important warning signs and decide where you stand.

Looking for more investment ideas?

If you stop with just one stock story, you risk missing other opportunities that better match your goals, risk comfort, and income needs.

- Target quality at a discount by scanning companies our model flags as 51 high quality undervalued stocks based on fundamentals and pricing.

- Prioritise resilience by checking out 78 resilient stocks with low risk scores, focusing on businesses our model scores with lower overall risk.

- Get ahead of the crowd by reviewing our screener containing 23 high quality undiscovered gems, where strong financial profiles have not yet attracted wide attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com